EchoStar (ECHO) Stock Looks Cheap On Cash Flow While Sales Look Rich

EchoStar Corporation Class A ECHO | 0.00 |

EchoStar stock has delivered an extremely strong 3 year return while the valuation checks are split, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to a discount and market multiples screening the shares as expensive.

- EchoStar has returned roughly 4.1x over the past 3 years, which puts recent share price volatility into the context of a very large longer term gain.

- Progress on monetising satellite, spectrum and wireless assets can support the intrinsic value case, while heavy debt levels and restructuring processes, including the prepackaged Chapter 11 filing at DISH DBS and legal work around Hughes Network Systems, remain key risks for how equity value is ultimately shared.

- The company scores 3 out of 6 on value checks, which points to a mixed picture rather than a straightforward bargain or clear overvaluation.

The stock's next move may depend on whether EchoStar's current price still offers enough margin between the market value and the intrinsic value suggested by the Discounted Cash Flow (DCF) work.

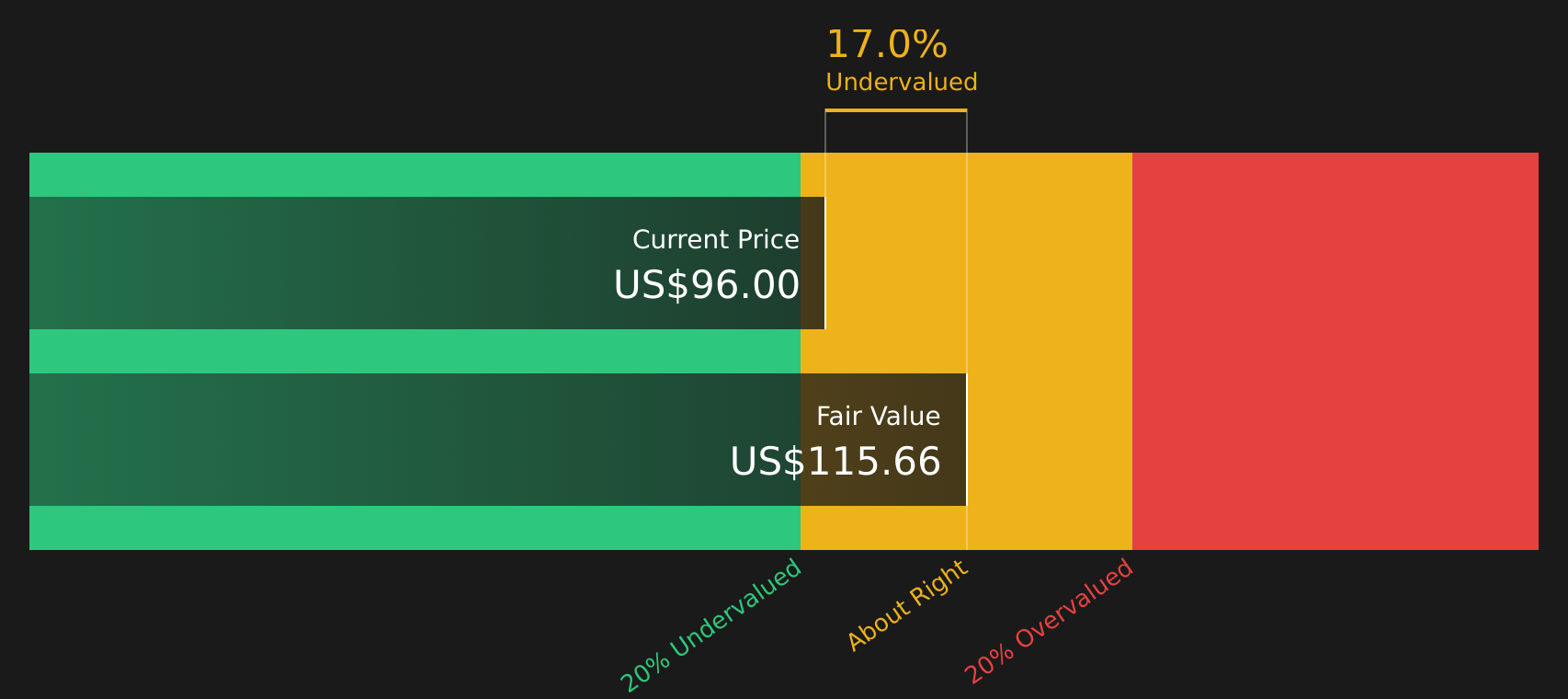

Is EchoStar a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model estimates EchoStar’s value by projecting future free cash flows and discounting them back to today. For EchoStar, the latest twelve month free cash flow shows an outflow of about $2.4b, while the model assumes that cash flows recover and grow into positive territory over time.

Based on these assumptions, the 2 Stage Free Cash Flow to Equity model points to an estimated intrinsic value of about $115 per share. This figure sits above the current share price and implies the stock is trading at roughly a 15.1% discount. The prepackaged Chapter 11 process at DISH DBS and the broader debt restructuring work help explain why the market is hesitant to fully reflect that intrinsic value estimate.

Overall, the Discounted Cash Flow (DCF) work indicates that EchoStar stock appears undervalued relative to the cash flows analysts expect it to generate.

Our Discounted Cash Flow (DCF) analysis suggests EchoStar is undervalued by 15.1%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Has EchoStar Run Too Far on Sales?

The P/S ratio is a useful cross check for EchoStar because revenue is still a core anchor even as profits and cash flows move around during restructuring.

EchoStar trades on a P/S of about 1.9x, compared with roughly 1.1x for the wider Media industry and a peer average near 2.8x. On Simply Wall St’s tailored fair multiple of about 1.2x, which factors in the company’s profile and risks, the current P/S sits higher than the level this framework would typically suggest.

This gap indicates EchoStar screens as overvalued on sales relative to what the fair P/S model implies, even after considering how its assets and business mix differ from the industry.

On the P/S yardstick, EchoStar stock currently appears overvalued relative to what its revenue base would usually support.

The EchoStar Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the EchoStar valuation puzzle a step further by spelling out which future paths for EchoStar’s growth, margins and earnings would line up with a share price that is meaningfully higher or lower than today. Rather than relying on a single multiple or DCF output, each Narrative lays out the key assumptions behind its view of fair value so you can compare them with EchoStar's actual results over time. They are available on Simply Wall St's Community page.

EchoStar investors on Simply Wall St are split between a spectrum and SpaceX driven upside story and a balance sheet and execution risk story that could cap the stock.

Bull case: 29% undervalued

"Success in monetizing EchoStar's substantial spectrum assets, either through launching lucrative new services, entering wholesale partnerships with global carriers, or potential spectrum sales/leases, could unlock significant one-time gains or ongoing income, materially strengthening the balance sheet and supporting medium-term earnings..."

Bear case: 123% overvalued

"Before the big spectrum shuffle, this company was struggling..."

Do you think there's more to the story for EchoStar? Head over to our Community to see what others are saying!

The Bottom Line

EchoStar sits in a genuine valuation tug of war, with the Discounted Cash Flow (DCF) work suggesting intrinsic value is meaningfully above the current price while the sales multiple flags the stock as overvalued. That split largely comes down to how you weigh funding needs, timing of future cash flows and capital intensity against today’s sentiment and where peers trade. With broader valuation checks sending a mixed signal, the real question is whether EchoStar can turn its asset base into durable, positive free cash flow without eroding equity through restructuring, or whether the current discount simply reflects those risks accurately.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.