Ecolab (ECL) Leaves Russell Growth Indexes, Is The Upside Already Priced In?

Ecolab Inc. ECL | 0.00 |

Why Ecolab’s index removal matters for investors

Ecolab (ECL) has been removed as a constituent from several Russell growth benchmarks, including the Russell 1000 Growth and Russell Top 200 Growth indices, prompting index related selling and portfolio adjustments.

For investors, the key question now is how this technical shift in index membership relates to Ecolab’s fundamentals, including its current share price, recent returns and the size and composition of its underlying business.

Over the past month Ecolab’s 1 month share price return of 8.83% and year to date share price return of 6.08% point to firming momentum. The 3 year total shareholder return of 54.06% sits well ahead of its 4.50% 1 year total shareholder return, suggesting more moderate recent gains on a longer build up.

If Ecolab’s index exit has you thinking about where else capital might rotate, this could be a good moment to scan for opportunities in 20 top founder-led companies

With Ecolab stock up 8.83% over the past month and trading at $278.60 against an average analyst price target of $317.38, investors have to ask: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 12.2% Undervalued

The most followed narrative on Ecolab pegs fair value at $317.14, above the last close of $278.60. This frames the recent index exit against a richer long term story.

Ecolab is focusing on expanding its One Ecolab growth initiative, aiming to capitalize on market share gains and increased value pricing. This initiative is expected to drive revenue growth and improve net margins by delivering exceptional value to customers.

Want to see what sits behind that confidence in Ecolab? The narrative leans heavily on revenue expansion, firmer margins and a premium earnings multiple. Curious which specific forecasts justify that fair value and how they tie back to your own expectations.

Result: Fair Value of $317.14 (UNDERVALUED)

However, Ecolab’s story could shift quickly if heavy industrial demand weakens further or customers resist surcharges and price increases, which would put pressure on margins and volumes.

Another View: What Ecolab’s P/E Says About Valuation Risk

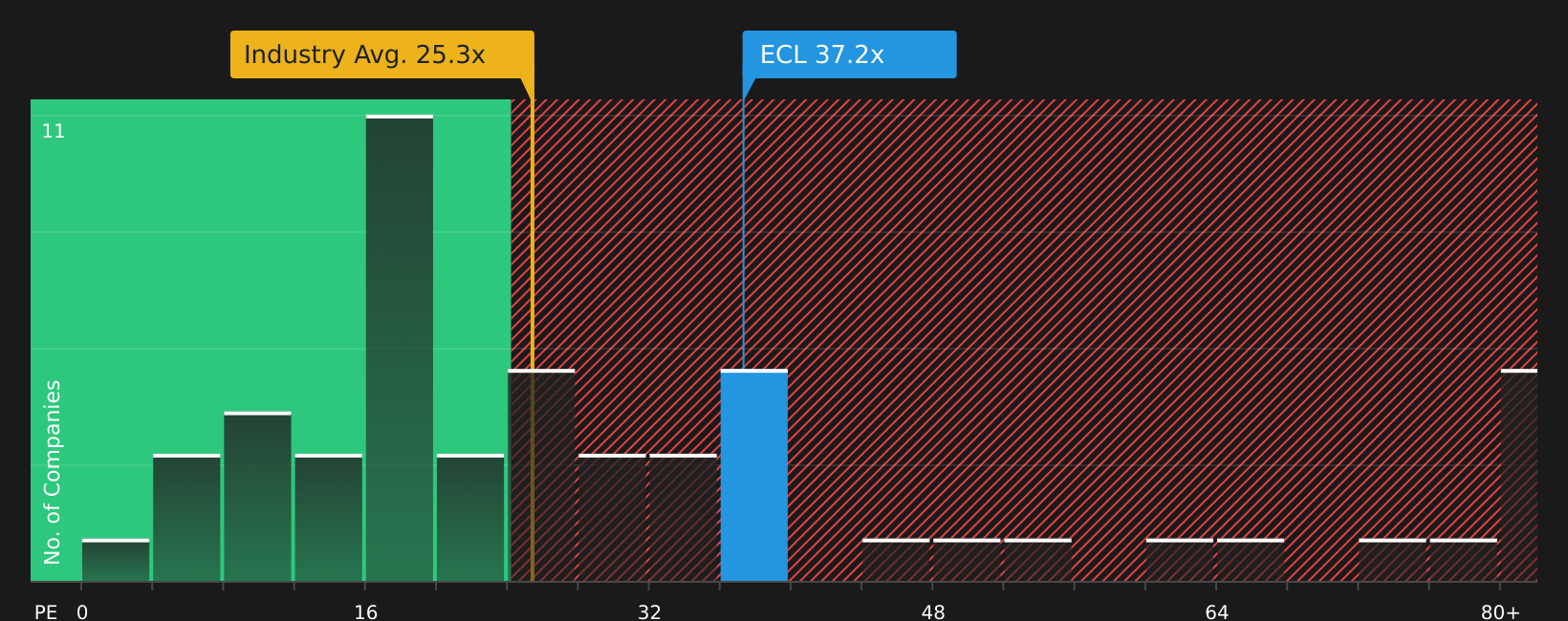

While the popular narrative tags Ecolab as 12.2% undervalued versus a $317.14 fair value, the current P/E of 37.2x tells a different story. It sits well above the US Chemicals industry at 24.6x, the peer average at 23.6x, and the fair ratio of 24.9x.

That gap suggests investors today are paying a clear premium, which can work either as a cushion if earnings keep tracking expectations, or as a source of downside risk if growth or margins disappoint. The key question is whether you think Ecolab’s performance will keep justifying that premium.

Next Steps

If this combination of optimism and caution around Ecolab feels familiar, use the data to move quickly and shape your own view with 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond Ecolab?

If Ecolab’s story has sharpened your thinking, do not stop here. Broaden your watchlist with other stocks that match the kind of criteria you care about most.

- Target potential upside by scanning companies that combine quality fundamentals with attractive valuations using the 42 high quality undervalued stocks.

- Prioritise resilience by reviewing stocks that show stronger balance sheets and fundamentals through the solid balance sheet and fundamentals stocks screener (48 results).

- Spot early opportunities by checking a screener containing 19 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.