Ecolab (ECL) Valuation Check As CDP Double A Rating Draws Fresh Investor Attention

Ecolab Inc. ECL | 264.28 | -1.95% |

Ecolab (ECL) just secured another double A rating from CDP for water and climate performance, putting its sustainability profile in focus as investors weigh what that might mean for the stock.

The CDP double A rating lands at a time when Ecolab’s short term momentum is firm, with a 1 month share price return of 7.28% and a 1 year total shareholder return of 17.04%. The 3 year total shareholder return of 82.97% points to longer term enthusiasm that predates this latest recognition.

If this kind of sustainability driven story interests you, it can be useful to widen the lens and look at other healthcare stocks that support critical hygiene and care needs around the world.

With the shares at $271.74 and trading at a discount of around 8% to analyst targets but a premium to some intrinsic estimates, you have to ask: is there still upside here, or is the market already pricing in future growth?

Most Popular Narrative: 7% Undervalued

Against the last close of $271.74, the most followed narrative pegs Ecolab’s fair value closer to $292, suggesting some remaining upside in the story.

Life Sciences is positioned for accelerated long-term growth, with mid-single-digit sales growth and significant share gains in its biopharma business. Investments in innovation and capacity expansion are anticipated to achieve operating income margins close to 30%, positively affecting long-term earnings potential.

Curious what kind of revenue trajectory and margin lift need to line up for that valuation to work? The narrative leans on steadily rising earnings, richer profitability, and a premium P/E that still sits above the broader chemicals group. Want to see how those moving parts come together to back a fair value near $292?

Result: Fair Value of $292.15 (UNDERVALUED)

However, softer demand in heavy industrial markets and pressure from higher local supplier costs could easily slow the margin story that underpins that US$292 fair value.

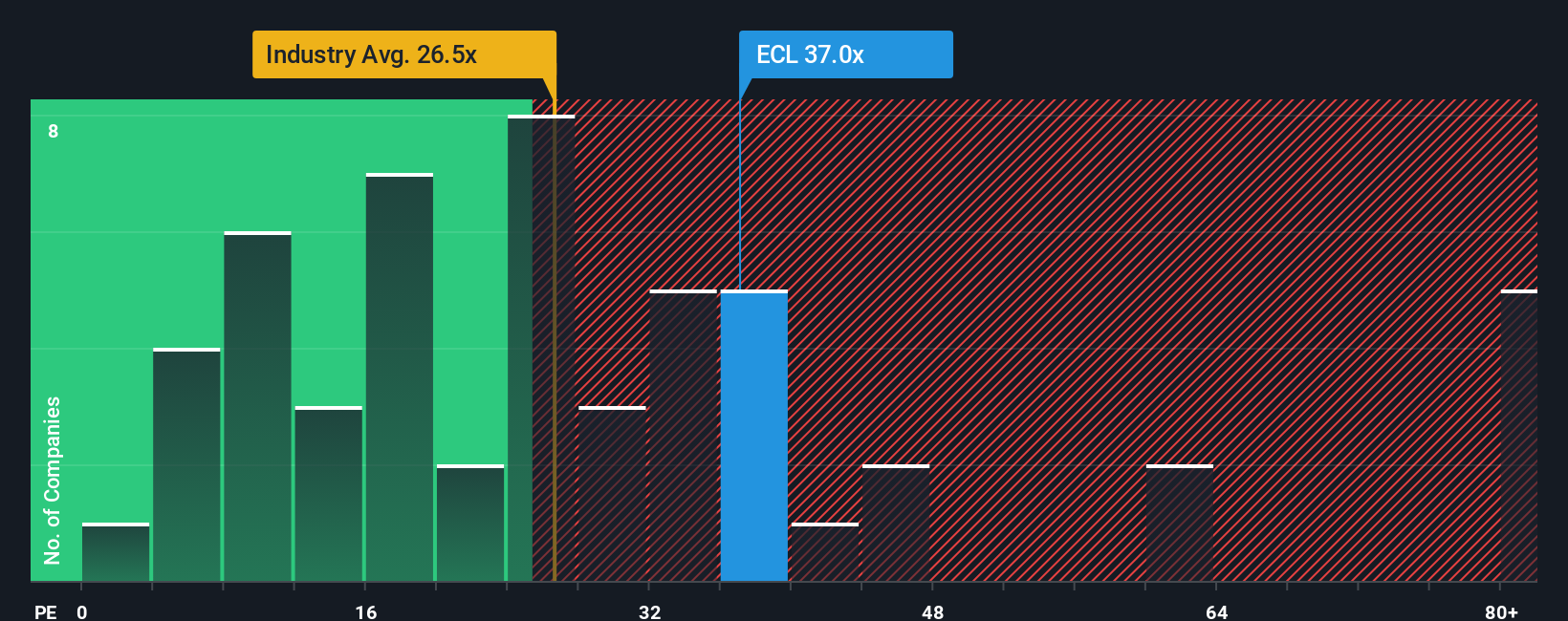

Another View: Expensive on P/E

That US$292 fair value narrative sits against a very different signal from the current P/E. At 38.8x, Ecolab trades well above the estimated fair ratio of 25.4x, the US Chemicals average of 25x, and a 24.1x peer average, which points to clear valuation risk if expectations soften.

When a stock sits this far above where its P/E could reasonably settle, it raises a simple question for you as an investor: are you comfortable paying up today for that margin and earnings story to keep playing out?

Build Your Own Ecolab Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions against the data, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your Ecolab research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Ecolab is on your radar, do yourself a favor and scan a few more angles so you are not relying on a single story or sector.

- Spot early growth stories by checking out these 3545 penny stocks with strong financials, where smaller names already show solid financial footing instead of just hype.

- Zero in on future tech themes through these 28 AI penny stocks, focusing on companies tying artificial intelligence to real business models rather than headline buzz.

- Strengthen your income side with these 11 dividend stocks with yields > 3%, filtering for yields above 3% so potential returns are not only about share price moves.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.