Element Solutions (ESI) Stock May Trade Near Fair Value While Earnings Carry A Premium

Element Solutions Inc ESI | 0.00 |

Element Solutions stock has more than doubled over the last three years, yet its valuation checks send a mixed signal, with the Discounted Cash Flow (DCF) estimate pointing to a share price that sits close to intrinsic value while market multiples suggest the stock trades at a premium.

- Element Solutions has delivered a 145.4% return over three years, which puts added pressure on today's valuation to be supported by the business fundamentals rather than past share price gains alone.

- Expectations for steady cash generation from Element Solutions' specialty chemicals portfolio can support the current price, but any disappointment in margins or capital allocation may quickly influence how much investors are willing to pay.

- On Simply Wall St's broader checks, Element Solutions scores 0 out of 6 for value, which indicates the stock does not screen as a clear bargain right now.

The issue now is whether Element Solutions' strong three year run has already priced in most of its fundamentals, or if the current level still offers enough value for new investors coming in today.

Is Element Solutions Fairly Priced on Cash Flow?

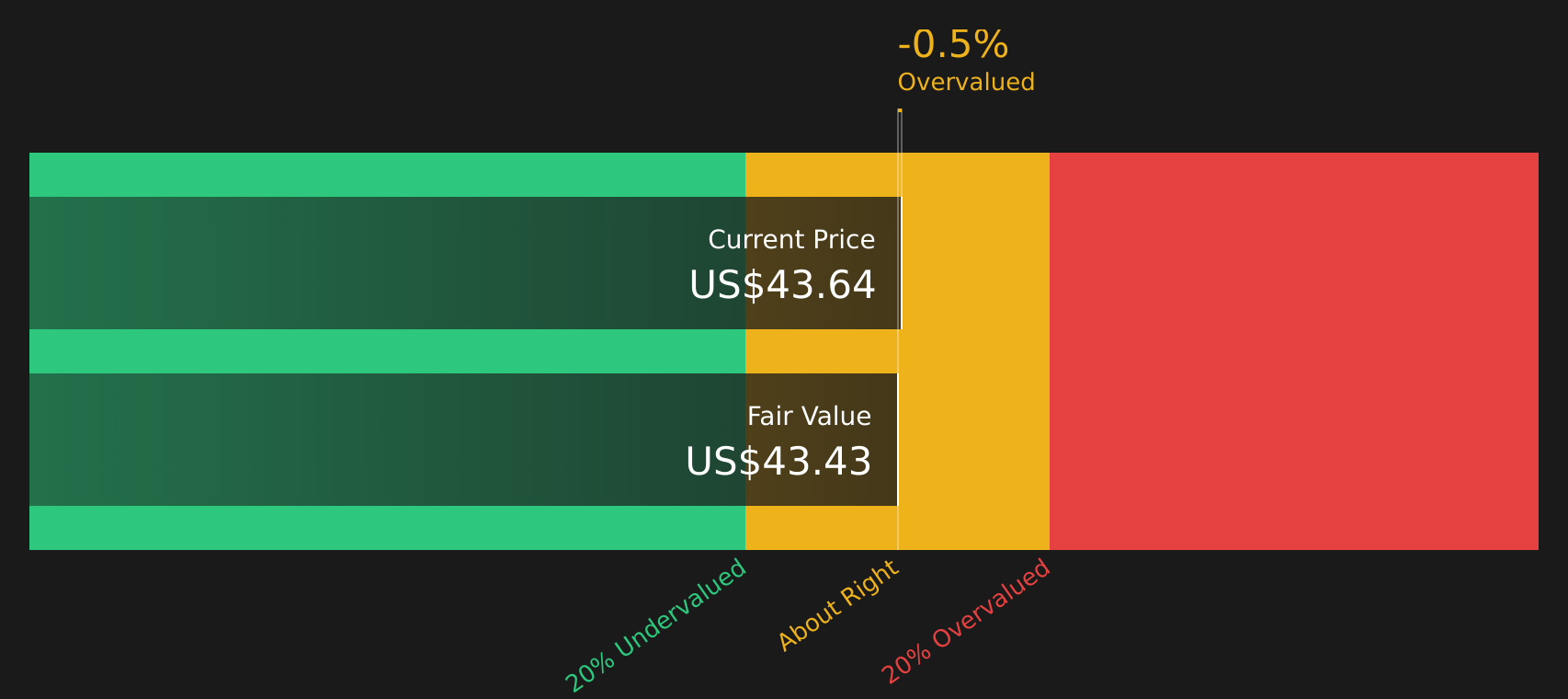

The Discounted Cash Flow (DCF) model estimates what Element Solutions is worth based on the cash it can generate for shareholders. On this view, the company is modeled with growing free cash flows, from latest twelve month free cash flow of about $123.9 million to higher levels over the coming years, using a 2 Stage Free Cash Flow to Equity approach.

Those projections translate into an estimated intrinsic value of about $43.36 per share. Compared with the current share price, the DCF output implies the stock is roughly 0.6% above that estimate, which is effectively a very small premium. For investors, that means the current market price for Element Solutions appears closely aligned with what its modeled cash generation supports rather than offering a clear discount or a clear excess.

On this cash flow view, Element Solutions stock appears to be approximately fairly valued at today’s price.

Element Solutions is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Element Solutions Getting Expensive on Earnings?

The P/E ratio is a common way to check what investors are willing to pay for each dollar of Element Solutions' earnings. Right now, the stock trades at about 71.5x earnings, which is well above the Chemicals industry average of roughly 25.7x and also higher than the peer group average of about 32.3x.

Simply Wall St's fair P/E estimate for Element Solutions, which reflects factors such as its industry, size and risk profile, is around 31.4x. That is less than half of the current multiple, indicating the market is assigning a relatively high price to the existing earnings base compared with what this framework would point to as a more typical level.

On the P/E lens, Element Solutions stock currently appears overvalued compared with both its sector and the modelled fair multiple.

The Element Solutions Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Element Solutions pick up where this valuation puzzle leaves off by spelling out the specific combinations of future growth, margins and earnings that would need to occur for the stock to look meaningfully cheaper or more expensive than it does today, based on frameworks shared on the Community page. Each narrative connects its number to a clear view of how Element Solutions' growth profile, profitability and key risks might evolve, giving you a reference point you can revisit as new information becomes available.

Share a narrative on Element Solutions to put your own number driven view on where its growth, margins and execution go from here, and see how that thesis stacks up as new results come through.

By adding your angle now, you can be one of the first voices in the Simply Wall St community that others refer back to as the Element Solutions story evolves.

Do you think there's more to the story for Element Solutions? Head over to our Community to see what others are saying!

The Bottom Line

For Element Solutions, the Discounted Cash Flow (DCF) work suggests the stock sits close to intrinsic value, so the bigger question is whether the earnings multiple premium can stay in place. Market pricing looks overvalued on P/E, which, together with the weaker value checks, implies you are paying up for the current earnings profile. The key swing factor from here is whether margins and cash generation can meet expectations strongly enough to justify that richer multiple, or whether sentiment cools and the valuation settles closer to sector norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.