Emerson Electric (EMR) Could Be 13% Undervalued Following New Gas Monitor Launch

Emerson Electric Co. EMR | 0.00 |

Emerson Electric (EMR) recently introduced the Rosemount 928 wireless gas monitor, a new sensor aimed at improving combustible gas detection in industrial settings through WirelessHART connectivity and more flexible, data rich monitoring.

Recent price action around Emerson Electric has been relatively steady, with the share price at $141.56 and a 90 day share price return of 5.14%. The 3 year total shareholder return of 67.21% points to stronger longer term momentum than the recent 7 day dip of 0.88% in the share price return might suggest.

If this kind of industrial automation story interests you, it could be a good time to look at other companies tied to energy and infrastructure by checking the 35 power grid technology and infrastructure stocks

Given Emerson Electric’s steady run to $141.56 and its mix of automation growth stories and index inclusion as a defensive value stock, does the current balance of risk and reward still lean toward buyers, or toward patience as valuation comes next?

Most Popular Narrative: 13.4% Undervalued

Compared with the last close at $141.56, the most followed narrative for Emerson Electric points to a fair value of $163.47, using a 10.01% discount rate and a detailed long term earnings roadmap as the backbone of that view.

The company's transformation toward a pure-play automation leader, emphasizing innovation, commercialization of new products, and operational excellence, continues to yield improved profitability (e.g., margin expansion, higher free cash flow) and positions Emerson to capitalize on long-term modernization and infrastructure trends.

Want to see what is behind that fair value gap for Emerson Electric? The core of this narrative is a specific revenue path, rising profitability and a future earnings multiple that many investors usually reserve for faster growing sectors. Curious which exact earnings and margin assumptions need to line up to support that outcome? The full narrative lays out the numbers and the reasoning that connect today’s price to that $163.47 estimate.

Result: Fair Value of $163.47 (UNDERVALUED)

However, the Emerson Electric story can change quickly if the execution of large projects stumbles or if trade and currency pressures squeeze margins in key automation segments.

Another View on Emerson Electric’s Valuation

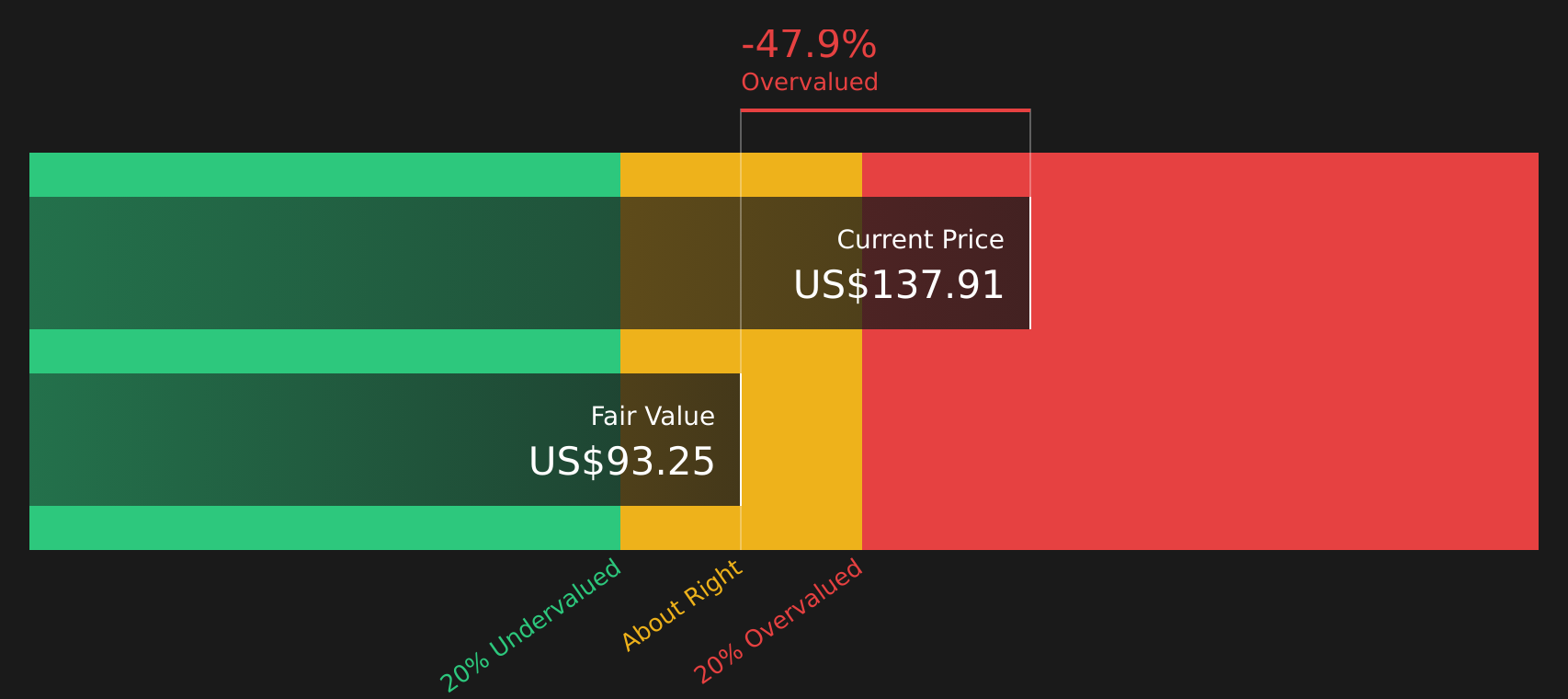

While the most followed Emerson Electric narrative sees about 13.4% upside to a fair value of $163.47, the SWS DCF model tells a different story. On that measure, EMR at $141.56 is trading above an estimated future cash flow value of $93.74, which points to an overvalued reading instead. Which set of assumptions feels closer to how you think this business will actually perform?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and caution around Emerson Electric resonates, it makes sense to act now by reviewing the data yourself and weighing both sides of the story using the 5 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Emerson Electric?

If you are serious about building a stronger portfolio, do not stop at Emerson Electric. Use these targeted stock ideas to pressure test and broaden your watchlist.

- Target consistent income by reviewing 8 dividend fortresses that focus on cash returns and income resilience through changing market conditions.

- Hunt for quality at a reasonable price with 41 high quality undervalued stocks that combine fundamentals and valuation checks in one place.

- Strengthen your downside protection by focusing on 74 resilient stocks with low risk scores that aim to keep risk scores contained while still offering upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.