Emerson Electric (EMR) Valuation Check After Q1 2026 Beat And Raised EPS Outlook

Emerson Electric Co. EMR | 0.00 |

Emerson Electric (EMR) is back on investors’ radar after its Q1 2026 earnings report and a higher full year EPS forecast, with management pointing to electrification and nearshoring as key demand drivers.

The Q1 earnings beat and raised EPS guidance arrived after a strong run, with a 90 day share price return of 14.26% and a 1 year total shareholder return of 26.02%, suggesting momentum has been building over both shorter and longer periods.

If this earnings update has you thinking about where else industrial demand and electrification themes could lead, it might be worth scanning 23 power grid technology and infrastructure stocks as a starting list of related ideas.

With the shares at $150.75, a value score of 2 and a P/E below the Electrical Equipment industry’s 44.5 average, is Emerson still quietly undervalued, or is the market already pricing in years of growth?

Most Popular Narrative: 8.4% Undervalued

At $150.75, the most followed narrative sees Emerson Electric’s fair value closer to $164.51, pointing to a modest gap between price and underlying story.

The company's transformation toward a pure-play automation leader, emphasizing innovation, commercialization of new products, and operational excellence, continues to yield improved profitability (e.g., margin expansion, higher free cash flow) and positions Emerson to capitalize on long-term modernization and infrastructure trends.

Want to see what is baked into that valuation gap? Revenue growth, margin uplift, and earnings power all play a part, but not in equal measure.

Result: Fair Value of $164.51 (UNDERVALUED)

However, that gap only holds if tariffs, currency swings, and AspenTech integration risks do not chip away at margins or disrupt the automation and software story that investors are banking on.

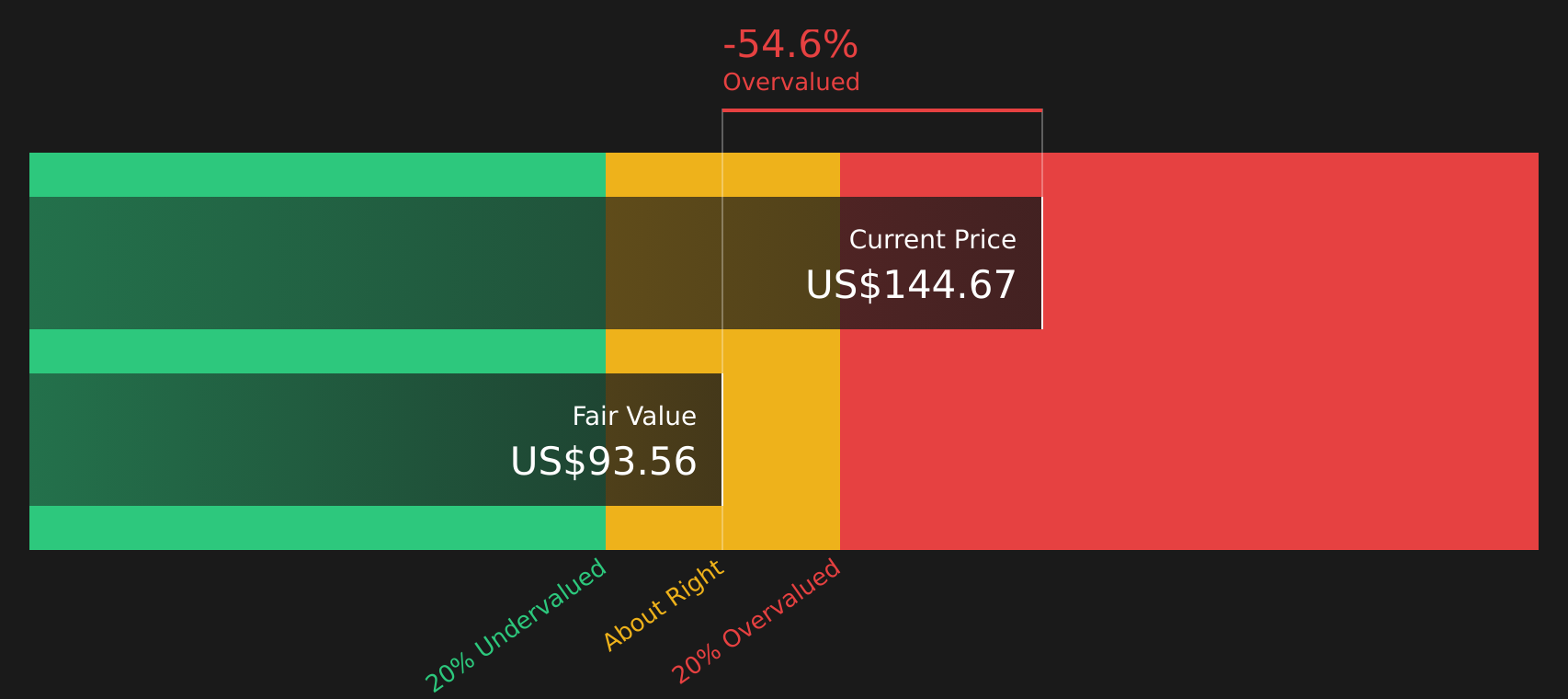

Another Angle On Value

That 8.4% gap to fair value is one story. The SWS DCF model tells a different one, with Emerson at $150.75 compared with an estimated future cash flow value of $79.53, which screens as overvalued. Is the market paying up for quality, or getting ahead of itself?

Next Steps

All this mixed sentiment only helps if you turn it into your own view.

Ready for more investment ideas?

If Emerson has sharpened your thinking, do not stop here. Broaden your watchlist now so you are not looking back wishing you had started sooner.

- Target steadier compounding by reviewing 74 resilient stocks with low risk scores that aim to keep downside in check while still giving your capital room to work.

- Hunt for potential mispricing with screener containing 24 high quality undiscovered gems that combine solid fundamentals with limited market attention.

- Strengthen the core of your portfolio through solid balance sheet and fundamentals stocks screener (39 results) that prioritize financial resilience and staying power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.