Energy Stocks Retail Investors Are Watching As Middle East Supply Risks Ease

Excelerate Energy, Inc. Class A EE | 0.00 |

Peace signals between the U.S. and Iran, extra IAEA oversight, and a toll free reopening of the Strait of Hormuz have shifted attention back to how quickly risk premiums can change in global energy markets. For investors watching large, financially solid oil and gas stocks in the U.S., UK, Canada, and Australia, this mix of easing tensions and lingering uncertainty could reshape how certain companies are priced. This article looks at 3 stocks from the Global Energy Sector screener that appear closely tied to the news, helping you decide whether they deserve a closer look or a wider berth in your portfolio.

National Energy Services Reunited (NESR)

Overview: National Energy Services Reunited is a Houston based oilfield services company that supports drilling and production across the Middle East and North Africa, offering hydraulic fracturing, coiled tubing, cementing, artificial lift and safety systems, alongside drilling rigs, logging, fluids and thru tubing solutions.

Operations: NESR generates about US$869 million from Production Services and US$557 million from Drilling and Evaluation Services, with roughly US$1.4b of its revenue coming from the Middle East and North Africa and a small contribution from the rest of the world.

Market Cap: US$2.5b

National Energy Services Reunited sits at the heart of MENA oil activity, so a toll free reopening of the Strait of Hormuz and a formal easing in U.S. Iran tensions directly support its ability to keep rigs turning and wells serviced with fewer supply chain headaches. At the same time, the stock is described as heavily undervalued against some fair value estimates and carries strong earnings growth forecasts, yet trades on a rich P/E and relies on higher risk external borrowing, which raises questions about how much optimism is already priced in. Combined with long term national oil company contracts and growing sustainability projects, investors face a mix of resilience, concentration risk and a potentially underappreciated re rating narrative that still requires further assessment.

National Energy Services Reunited looks like an underappreciated Middle East workhorse, with earnings expectations and long term contracts that do not fully square with its rich P/E. Before deciding it is mispriced or misunderstood, review the analyst forecasts for National Energy Services Reunited

Gulf Marine Services (LSE:GMS)

Overview: Gulf Marine Services operates self propelled, self elevating support vessels that provide offshore construction, heavy lifting, accommodation, well intervention and manpower services to oil and gas and renewables clients across the Middle East and Europe.

Operations: Gulf Marine Services generates about $87.4m from E Class vessels, $54.7m from K Class vessels and $46.1m from S Class vessels, with revenue concentrated in Qatar, Saudi Arabia and the United Arab Emirates.

Market Cap: £211.8m

Gulf Marine Services is tightly linked to offshore activity in the Gulf, so a toll free reopening of the Strait of Hormuz and an interim peace deal that lowers regional risk premiums directly support demand for its vessels and services. Forecast earnings growth of around 35.5% a year and a share price that sits well below some fair value estimates have caught investors’ attention. However, margins have compressed, net profit fell after a one off $10.1m loss and all liabilities are funded through higher risk borrowing. When combined with a strong contract backlog, recent vessel deployments in new regions and an experienced, largely independent board, Gulf Marine Services becomes a stock where stabilizing geopolitics could matter a lot more than the recent share price suggests.

Gulf Marine Services’ compressed margins and higher risk borrowing could be masking a very different story as contracts stack up and regional risks ease. Get the full picture in the 2 key rewards and 2 important warning signs

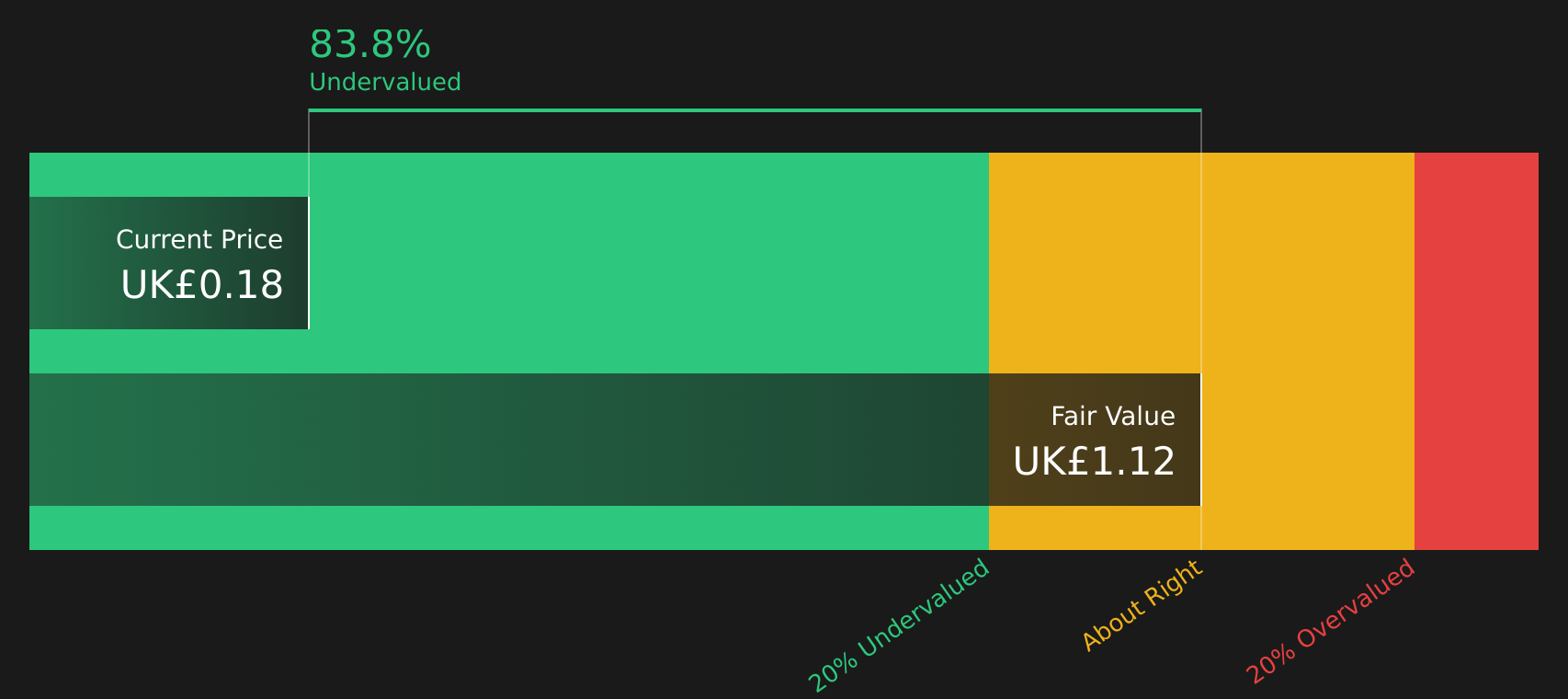

Excelerate Energy (EE)

Overview: Excelerate Energy is a Texas based LNG specialist that owns and operates floating regasification terminals, providing the ships, crew and technical services that turn imported liquefied natural gas back into usable gas for power, industrial customers and utilities around the world.

Operations: Excelerate Energy generates about US$1.35b from gas utility activities, with revenue spread across North America, Latin America, the Middle East, Asia Pacific and Europe.

Market Cap: US$4.1b

Excelerate Energy gives you exposure to LNG infrastructure at the point where energy security and cleaner fuel switching intersect, backed by long term, take or pay style contracts and projects such as Iraq’s large scale floating regasification terminal. The company benefits when routes like the Strait of Hormuz stay open, reducing disruption risk to its supply chains and to customers in regions such as the Middle East, Asia and Latin America. It still carries thin margins, a premium P/E and questions about subscale operations and lower gross profitability versus peers. That mix of contracted growth, geopolitical sensitivity and structural profitability concerns means Excelerate Energy could look either underrated or overhyped depending on how you weigh LNG demand and execution risk.

Excelerate Energy’s contracted LNG projects and premium P/E suggest the market might be missing a key angle on its future earnings power. Walk through the analyst forecasts for Excelerate Energy and see what the market might be pricing in or ignoring.

The three stocks covered here are only a starting point, as the full Global Energy Sector (Oil & Gas) screener surfaced 30 more large, financially solid oil and gas companies with equally compelling narratives. Unlock deeper context around contracts, balance sheet strength, and earnings drivers, and use Simply Wall St to identify and analyze the specific catalysts that matter most so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Gulf Marine Services or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Market attention shifts quickly, and the stocks still under the radar for now can move to full priced once momentum builds. Scan these fresh ideas before the crowd, act now.

- Spot potential breakout small caps before they get caught in a rush by scanning the 33 AI small caps while interest in the theme still builds quietly.

- Target resilient compounders that may hold up when others are dropping by reviewing the 67 resilient stocks with low risk scores while the list remains under the radar for now.

- Hunt for companies where cash flows and balance sheets already line up for the next breakout by checking the 19 high quality undiscovered gems before momentum traders arrive.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.