Enterprise Financial Services (EFSC) Lifts Its Dividend, Is The Upside Already Priced In?

Enterprise Financial Services Corp EFSC | 0.00 |

Dividend growth puts Enterprise Financial Services in focus

Enterprise Financial Services (EFSC) is drawing attention after lifting its annualized dividend by 11.5%, supported by a 25% payout ratio and consensus expectations for earnings growth that together highlight the stock’s current income profile.

The recent dividend increase comes as Enterprise Financial Services trades at $66.86, with a 90 day share price return of 25.42% and a 1 year total shareholder return of 22.67%, suggesting momentum has been building both in the short and longer term.

If this dividend story has you rethinking your watchlist, it could be a good moment to broaden your search and check out 20 top founder-led companies

With Enterprise Financial Services trading close to its analyst price target and carrying an intrinsic value estimate that suggests a sizeable discount, the key question is whether there is genuine upside here or whether the market is already pricing in future growth.

Price-to-Earnings of 12.4x: Is it justified?

Enterprise Financial Services currently trades on a P/E of 12.4x, which sits slightly above both its estimated fair P/E of 11.1x and the US Banks industry average of 12.3x.

The P/E ratio compares the share price with earnings per share and, for a bank like Enterprise Financial Services, it gives a quick read on how the market is valuing its profit stream relative to peers.

Here, the market is applying a small premium to Enterprise Financial Services versus the wider US Banks industry. However, the SWS fair ratio model points to a lower level that the valuation could gravitate toward if sentiment and fundamentals line up.

At the same time, the current P/E of 12.4x sits below the peer average of 13.6x. The stock is priced richer than the industry as a whole but cheaper than its closer peer group, which sets up a mixed picture on how much investors are willing to pay for its earnings compared with different benchmarks.

Result: Price-to-earnings of 12.4x (ABOUT RIGHT)

However, investors in Enterprise Financial Services still face risks, including any shift in bank credit conditions or a reassessment of its current valuation premium.

Another view on Enterprise Financial Services valuation

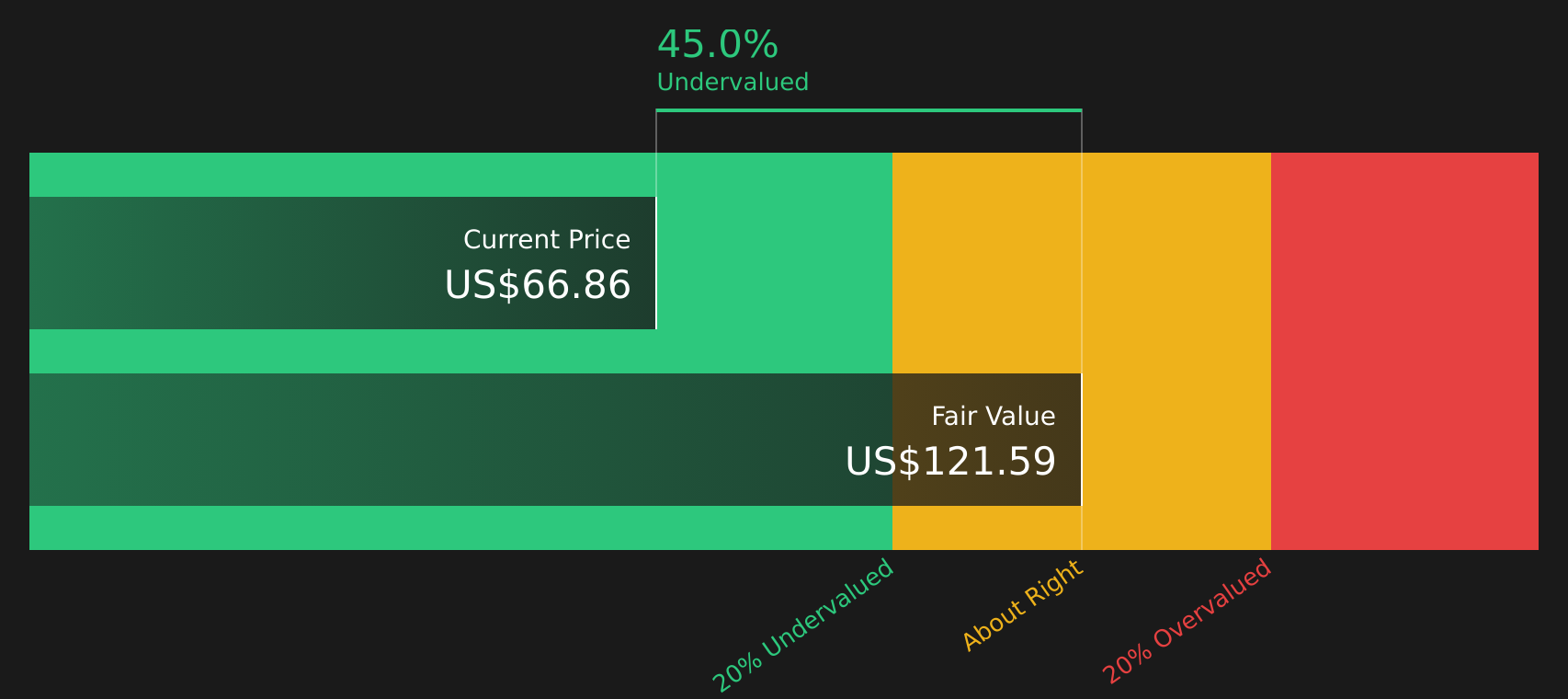

The P/E discussion presents Enterprise Financial Services as roughly fairly priced, but the SWS DCF model suggests a different perspective. At $66.86, EFSC is trading at a 45% discount to an estimated future cash flow value of $121.59. This indicates that the market may be heavily discounting its long term cash generation. Investors may want to consider which signal carries more weight in their own analysis.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enterprise Financial Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of dividend growth and valuation signals around Enterprise Financial Services has you thinking, consider acting while the data is fresh and forming your own view by checking the 4 key rewards

Looking for more investment ideas beyond Enterprise Financial Services?

Do not stop with Enterprise Financial Services; broaden your watchlist now by scanning fresh opportunities that match your style before other investors move first.

- Target steady income by reviewing stocks with strong yields and resilient payouts through the 8 dividend fortresses.

- Zero in on companies that combine quality with attractive pricing using the screener containing 19 high quality undiscovered gems.

- Prioritize capital preservation and smoother returns by checking stocks highlighted in the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.