Enterprise Products Partners Extends Payout Streak While Funding Growth Projects

Enterprise Products Partners L.P. EPD | 37.33 37.33 | +0.62% 0.00% Post |

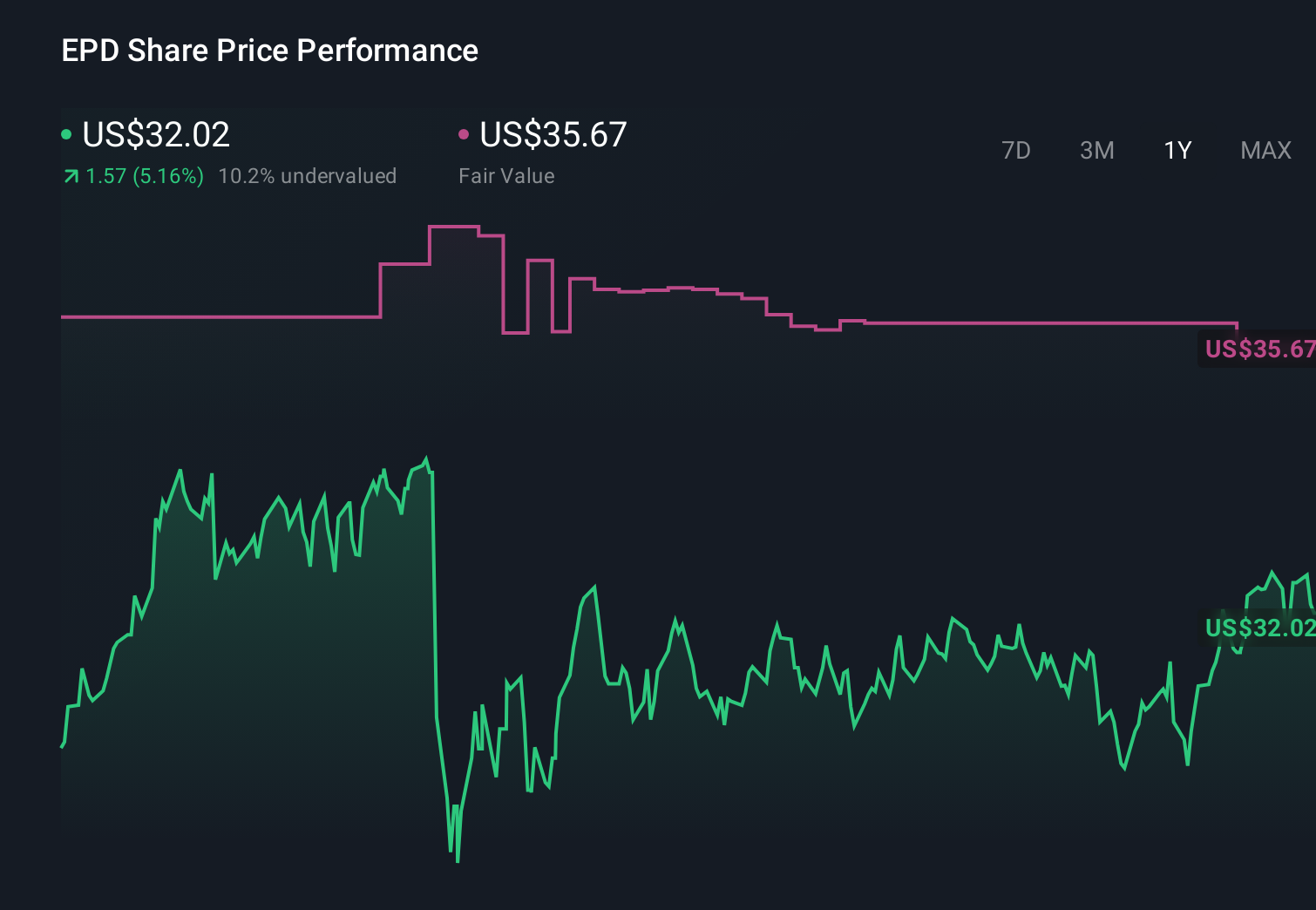

- Enterprise Products Partners (NYSE:EPD) has extended its track record of distribution increases to 27 consecutive years.

- The partnership reports continued stable cash flows that support both its current distributions and new infrastructure investments.

- Management is directing capital toward additional midstream projects while maintaining what it describes as robust distribution coverage.

Enterprise Products Partners is a major midstream energy partnership focused on pipelines, storage, and related infrastructure that help move oil, gas, and natural gas liquids across the United States. For readers watching the midstream space, the combination of long term contracts and fee based revenue is a key part of why cash flow stability often features prominently in discussions of NYSE:EPD. The latest update on distributions and coverage sits within a sector backdrop where income reliability is a priority for many investors.

For income focused holders, the new information around distribution coverage and project spending matters because it speaks to how NYSE:EPD is attempting to balance current payouts with future growth projects. The continuation of a 27 year distribution increase streak, alongside ongoing infrastructure spending, indicates that management is currently emphasizing both steady cash returns and expansion of the asset base. Readers evaluating NYSE:EPD today will likely pay close attention to how these projects and coverage metrics change over time.

Stay updated on the most important news stories for Enterprise Products Partners by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Enterprise Products Partners.

The latest update reinforces Enterprise Products Partners' income-focused story, with 27 consecutive years of distribution increases supported by what management describes as strong, stable cash flows and solid coverage. Full year 2025 net income of US$5,814m and continued fee based midstream operations help explain how the partnership is funding both a high distribution and new infrastructure, while the completion of US$1,437.45m in unit buybacks since 2019 signals a willingness to return excess cash to unitholders beyond regular payouts.

How this ties into the Enterprise Products Partners narrative

The news aligns with the existing narrative that sees EPD using growth capital on gas and NGL projects while also using discretionary cash for unit repurchases and debt reduction. Record EBITDA cited around the recent quarter and new assets coming online are consistent with that storyline of volume driven, fee based growth, and investors comparing EPD with peers such as Kinder Morgan and Williams can see a similar focus on long term contracts and export infrastructure.

Risks and rewards investors are weighing

- ⚠️ Distribution is flagged as not well covered by free cash flows, which could limit flexibility if operating conditions become less favorable.

- ⚠️ A high debt load means interest costs and access to credit remain important watchpoints, especially as new projects are built.

- 🎁 Earnings are forecast to grow, which, if realized, could support continued distributions and ongoing capital returns.

- 🎁 Some analysts view the units as good value relative to peers, which can be appealing for income oriented investors comparing midstream options.

What to watch next

From here, investors may want to track how new midstream projects ramp up, whether buybacks remain part of the toolkit, and how distribution coverage evolves as capital is split between payouts, growth spending, and debt. If you want to see how other investors are connecting these updates with longer term themes, take a look at the community narratives for EPD on this dedicated page.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.