Enterprise Products Partners Ups Payout As LNG And Power Demand Build

Enterprise Products Partners L.P. EPD | 37.57 | +0.37% |

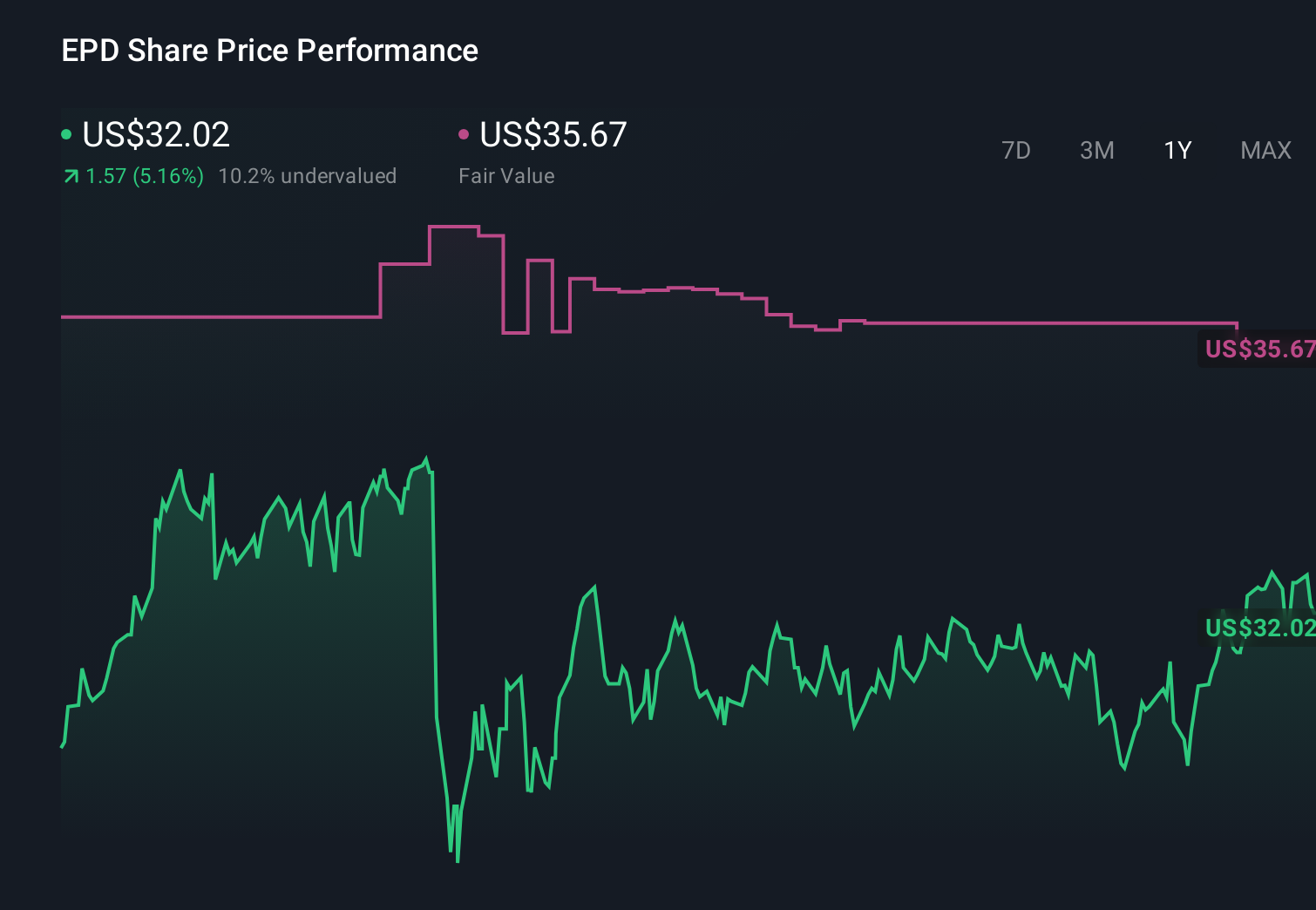

- Enterprise Products Partners (NYSE:EPD) announced a quarterly cash distribution increase.

- The partnership continued executing unit buybacks alongside the higher cash payout.

- Management highlighted confidence in long term cash flow to support these capital returns.

- EPD is positioned to benefit from strong electricity demand and expanding LNG exports.

Enterprise Products Partners operates a large midstream network tied to energy production, processing, and transport, so its cash flows are closely linked to long term demand for energy infrastructure. With electricity demand and LNG exports expected to play a growing role in global energy, EPD’s asset base sits at the center of key supply chains rather than short term pricing moves.

For income focused investors, the mix of a higher cash distribution and ongoing buybacks can be an important signal about how management views the durability of its cash generation. If electricity demand and LNG exports stay supportive over time, that backdrop could help EPD maintain flexibility around future capital returns and investment priorities.

Stay updated on the most important news stories for Enterprise Products Partners by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Enterprise Products Partners.

The 2.8% quarterly cash distribution uplift and ongoing unit buybacks signal that management is comfortable returning more cash to unitholders while still funding the business. For income oriented investors, a higher cash payout, paired with a 6.7% to 6.8% yield, underlines the importance of Enterprise Products Partners as a cash flow story tied to long term energy infrastructure demand.

Enterprise Products Partners Narrative, Confidence in Cash Flows vs Market Caution

Recent investor interest, including EPD being one of the most searched names and a sector perform rating with a raised US$35 price target, suggests a narrative that balances income appeal with measured expectations for near term performance. The expectation for current quarter earnings of US$0.70 per unit, slightly below the prior year, reinforces that the story many investors focus on is less about short term earnings swings and more about long run fee based cash generation.

EPD Risks and Rewards in Focus

- Trading at what some analysts view as good value compared with peers and industry and supported by income focused interest.

- Exposure to electricity demand and LNG export infrastructure that could support fee based cash flows over time.

- The 6.63% distribution is not fully covered by free cash flow, which may matter if operating conditions tighten.

- A high level of debt means funding costs and balance sheet strength remain key things for investors to monitor.

What to Watch Next

Looking ahead, investors may want to watch how distribution coverage, buyback pace, and actual LNG and electricity linked volumes track against expectations, as these will shape how durable this capital return profile looks. You can stay close to how the broader story is evolving by following a community of investors and reading shared narratives in this dedicated hub.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.