Envista Holdings (NVST) Valuation Check After Earnings Beat, Profit Swing And Share Buybacks

Envista Holdings NVST | 26.91 26.91 | +1.97% 0.00% Pre |

Why Envista’s latest earnings matter for investors

Envista Holdings (NVST) has just reported fourth quarter and full year 2025 results that came in ahead of Wall Street expectations, alongside 2026 guidance that points to further revenue and EBITDA growth.

The company moved from a large loss in 2024 to a profit in 2025, with management linking this shift to broad based contributions across its business units, new product launches and tighter operational efficiency.

The earnings beat and guidance update have quickly fed into the market’s view of Envista, with the share price up 17.77% over the past day and a 90 day share price return of 45.14% pointing to building momentum. That short term move contrasts with a 3 year total shareholder return of negative 27.12%, so recent gains are coming off a weaker longer term base as investors reassess the company’s profitability and risk profile.

If strong earnings have you rethinking where growth could come from next, it might be worth checking our screener of 26 healthcare AI stocks as another way to find opportunities linked to shifts in healthcare technology and demand.

With Envista now profitable again, the share price up sharply and the stock trading slightly above the average analyst target, the key question is whether there is still mispricing here or if the market is already factoring in future growth.

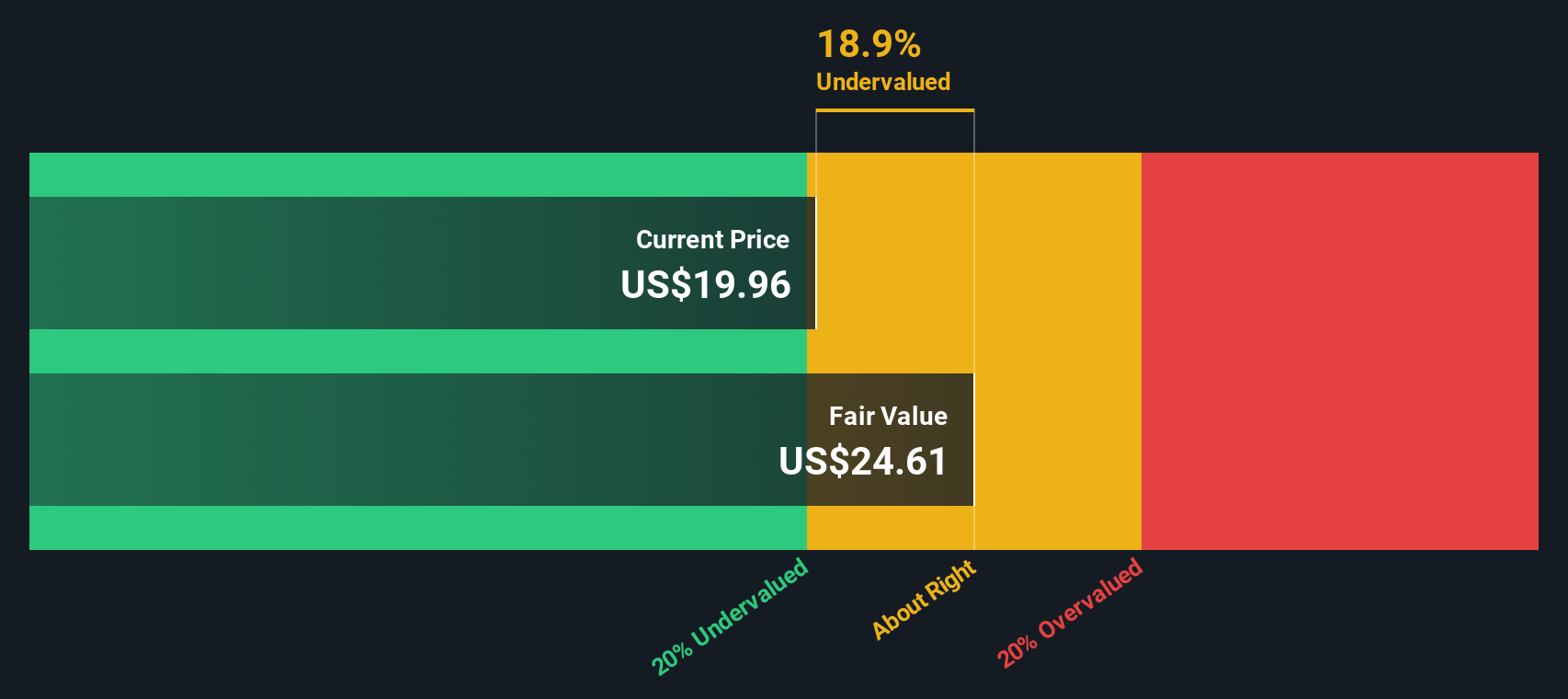

Most Popular Narrative: 3.9% Overvalued

Envista last closed at $29.10 compared with a most followed fair value narrative of $28.00, which leans slightly cautious on where the share price sits today.

The accelerating aging of populations globally and increasing oral health awareness are combining to drive a supercycle in restorative procedures and elective dental treatments, positioning Envista to capture a disproportionate share of wallet in both premium implants and orthodontics, leading to sustained above market revenue growth for years to come.

Want to see how steady top line assumptions, rising margins and a lower future earnings multiple still point to that fair value? The full narrative lays out the growth, profitability and valuation bridge in a way raw price moves alone cannot.

Result: Fair Value of $28.00 (OVERVALUED)

However, there are still real pressure points here, including slower patient growth in mature markets and rising regulatory and tariff costs that could squeeze margins and weaken the bullish case.

Another View: Our DCF Model Sees Slight Upside

While the most followed narrative frames Envista as about 3.9% overvalued at $29.10 versus a $28.00 fair value, our DCF model points the other way and suggests the shares trade around 5.1% below an estimated future cash flow value of $30.67. Which lens do you trust more when the signals conflict this closely?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Envista Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Envista Holdings Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a custom view of Envista in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Envista Holdings.

Looking for more investment ideas?

If Envista has sharpened your thinking, do not stop here. Broaden your watchlist with focused ideas that match how you like to invest.

- Target potential value by scanning companies that look mispriced on quality and fundamentals through our 52 high quality undervalued stocks.

- Prioritise resilience by zeroing in on businesses that score well on financial strength with the solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for future standouts by filtering a screener containing 24 high quality undiscovered gems before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.