Equinix (EQIX) Valuation Check As Earnings Optimism Builds On Expected EPS And Revenue Growth

Equinix, Inc. EQIX | 1052.98 | -0.42% |

Equinix (EQIX) is back in focus as investors watch for its February 11, 2026 earnings release, with expectations for higher year over year earnings per share and revenue shaping near term sentiment.

At a share price of US$807.46, Equinix has seen mixed momentum recently, with a 30 day share price return of 2.46% but a 1 year total shareholder return decline of 11.97%, suggesting enthusiasm around the upcoming earnings report sits against a softer longer term backdrop.

If Equinix has you thinking about where the next digital infrastructure opportunities might be, it could be worth scanning 33 AI infrastructure stocks as a way to spot other contenders benefiting from similar themes.

With the stock trading at US$807.46, alongside an indicated intrinsic discount and a gap to analyst price targets, the key question is whether Equinix is genuinely undervalued at this level or whether the market is already pricing in future growth.

Most Popular Narrative: 16.4% Undervalued

Equinix's most followed narrative points to a fair value of $965.56 compared with the current $807.46 share price, putting a spotlight on earnings and cash flow assumptions behind that gap.

The rapid expansion and customer adoption of Equinix Fabric and interconnection services (with 8% Y/Y growth, over 4,000 customers, and record interconnection revenue) create new high margin, asset light revenue lines, supporting expansion of overall net margins.

Curious what kind of revenue growth, margin lift and future earnings multiple are baked into that fair value number? The narrative highlights ambitious earnings expansion, higher profitability and a premium valuation, while still assuming less generous future pricing than today. The full story ties those moving parts together in a way the current share price does not fully reflect. Want to see exactly how that adds up and where the assumptions get stretched?

Result: Fair Value of $965.56 (UNDERVALUED)

However, you still need to weigh execution risk on major capital projects, as well as the reliance on a concentrated group of large cloud and hyperscale customers.

Another Angle On Valuation

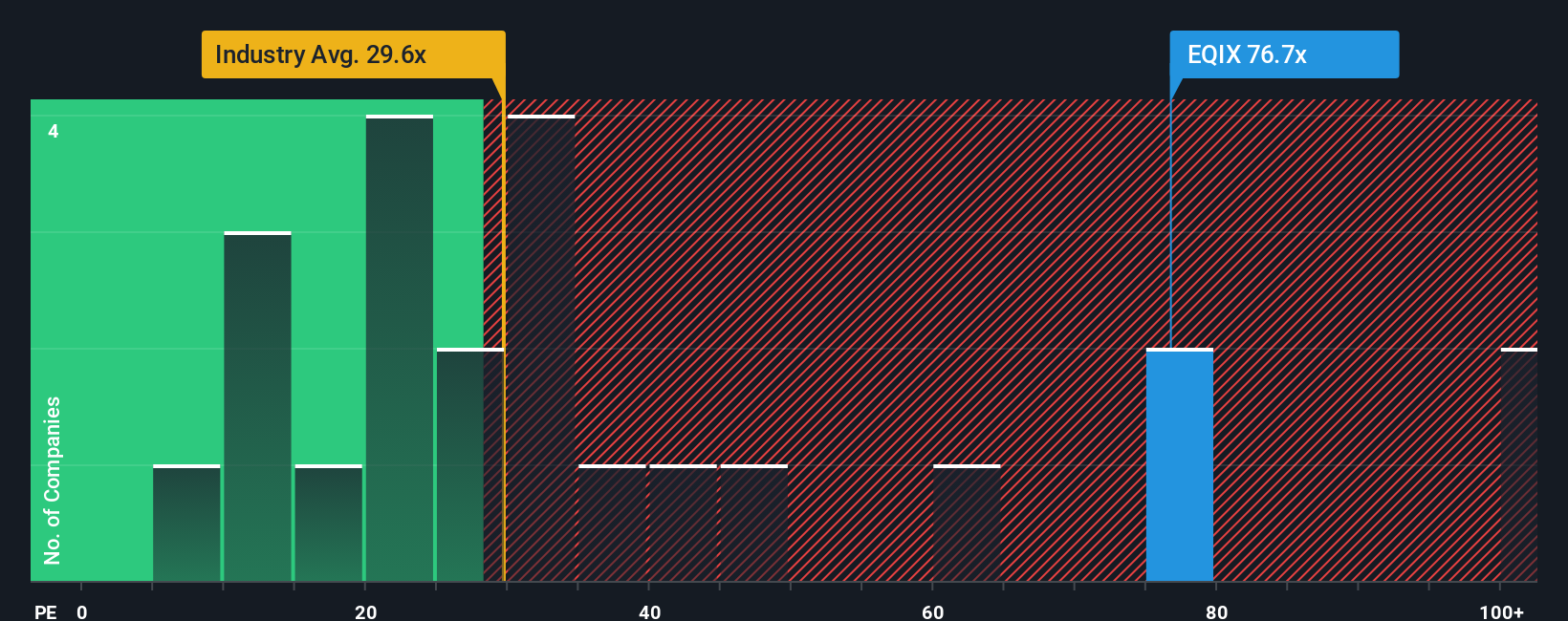

The narrative and analyst targets suggest Equinix looks undervalued, but its current P/E of 74x is far above both the US Specialized REITs industry average of 26.5x and a fair ratio of 37.3x, as well as a 28x peer average. That kind of gap can signal valuation risk if growth or margins fall short, so which reference point do you trust most?

Build Your Own Equinix Narrative

If you see the numbers differently or prefer to test your own assumptions, you can create a new Equinix narrative in just a few minutes by starting with Do it your way.

A great starting point for your Equinix research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready To Find Your Next Idea?

If Equinix has piqued your interest, do not stop here, some of the most compelling opportunities often sit just outside the names everyone is already watching.

- Target quality at a discount by scanning our list of 55 high quality undervalued stocks that combine appealing prices with resilient fundamentals.

- Prioritize resilience and sleep better at night by focusing on 80 resilient stocks with low risk scores that score well on stability and downside protection.

- Spot under followed opportunities early by checking out our screener containing 25 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.