Equitable Holdings Q4 Profit Of US$202 Million Tests Loss-Focused Bear Narratives

Equitable Holdings, Inc. EQH | 41.98 | -0.05% |

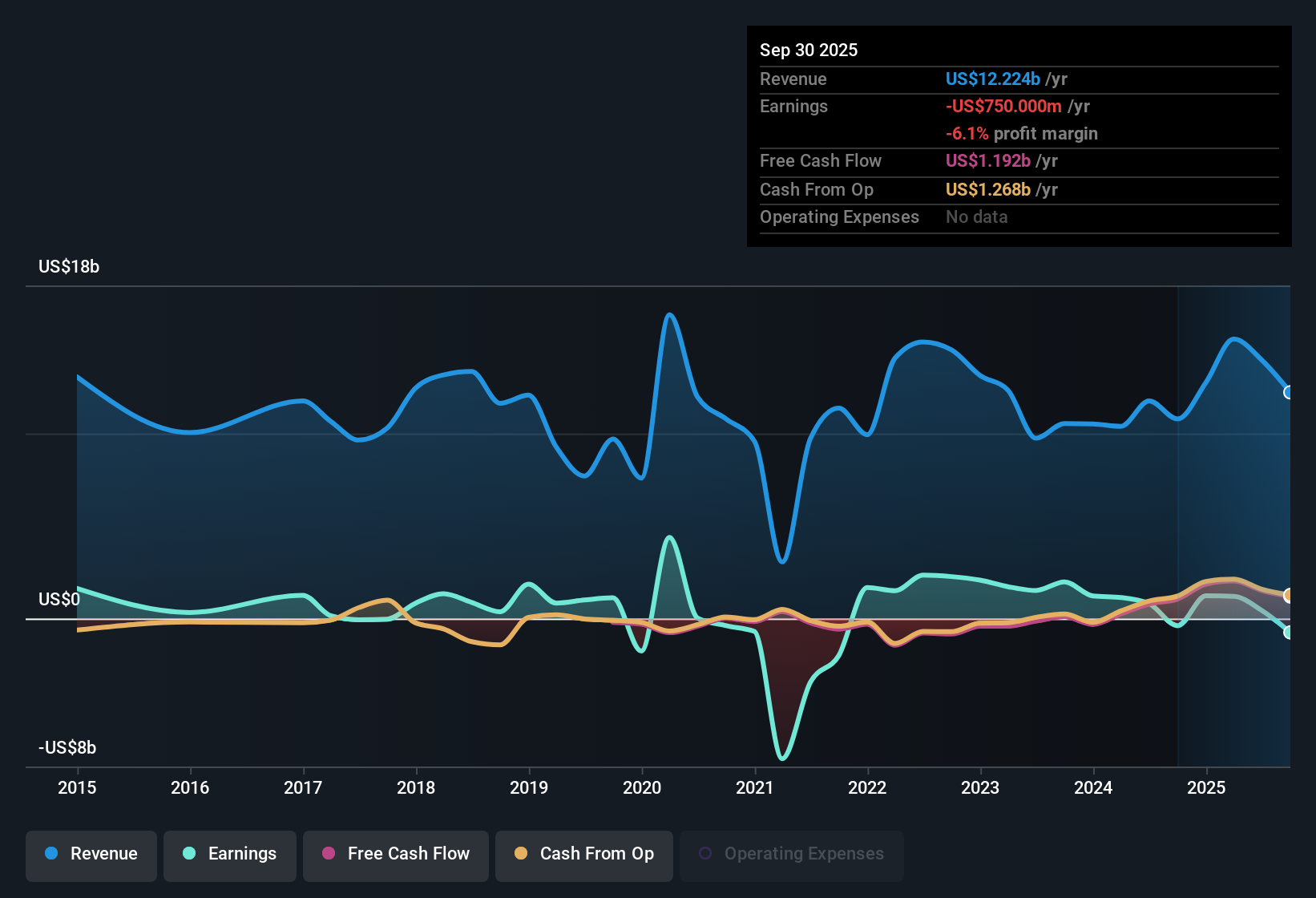

Equitable Holdings (EQH) has wrapped up FY 2025 with fourth quarter revenue of about US$3.3 billion, basic EPS of US$0.71 and net income of US$202 million, putting a cleaner quarter at the end of what has been a volatile earnings year. Over the past six quarters, revenue has moved between US$1.4 billion and US$4.6 billion while basic EPS has ranged from a loss of US$4.47 per share to a profit of US$2.80 per share, with trailing twelve month EPS at a loss of US$4.83 per share on revenue of US$11.7 billion and a net loss of US$1.4 billion. Against that backdrop, investors are likely to focus on how consistently the latest quarterly profit can support more stable margins and reduce the swings in earnings quality.

See our full analysis for Equitable Holdings.With the headline numbers on the table, the next step is to see how this earnings profile lines up against the widely held narratives around growth potential, risk and the timing of a possible profitability reset.

Losses On Trailing Basis Despite Q4 Profit

- Even with Q4 net income of US$202 million, the trailing twelve months still show a net loss of US$1.4b on revenue of about US$11.7b, with basic EPS at a loss of US$4.83 per share.

- What stands out for the bullish view that EQH is working toward a profitability reset is this split picture, with a profitable Q4 alongside trailing losses. This lines up with data showing losses have been shrinking over the past five years and that earnings are forecast to grow 53.44% per year as the business targets a move into sustained profit.

Revenue Growth Forecast Above Market

- EQH’s revenue is forecast to grow at 14.1% per year compared with a 10.3% per year forecast for the broader US market, so expectations are for the top line to expand faster than a general market benchmark.

- Bulls often point to this higher 14.1% revenue growth outlook together with the forecast shift from current losses of US$1.4b to profitability within three years. They argue that a business growing faster than the market with improving earnings should eventually see that reflected in its share price, yet the current trailing EPS loss of US$4.83 and a recent quarterly swing from a US$1.3b loss in Q3 to a US$202 million profit in Q4 show that the path there is still very uneven.

Cheap P/S But Debt And Dividend Trade Off

- EQH is trading on a P/S of 1.1x compared with 2.6x for the US Diversified Financial industry and 1.5x for peers, and the provided DCF fair value of US$102.49 is well above the current share price of US$43.40. At the same time the company carries high debt and its 2.49% dividend was not covered by earnings over the trailing twelve months.

- Critics of the bullish case argue that this apparent discount, with the share price also shown as 57.7% below a fair value estimate, needs to be weighed against balance sheet pressure and income strain. The trailing loss of US$1.4b together with a dividend not backed by current earnings supports that more cautious stance even though the low P/S multiple and DCF fair value of US$102.49 suggest there could be upside if the profit turnaround and revenue growth actually come through.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Equitable Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

EQH's trailing loss of US$1.4b, uncovered 2.49% dividend and high debt levels highlight pressure on both income reliability and balance sheet strength.

If that mix of losses and leverage has you wanting sturdier options, check out our solid balance sheet and fundamentals stocks screener (46 results) to focus on companies with stronger financial footing right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.