ESCO Technologies (ESE) Following Analyst Upgrades Is The Stock Already Fully Valued

ESCO Technologies Inc. ESE | 0.00 |

Analyst interest builds around ESCO Technologies after strong year-to-date run

ESCO Technologies (ESE) has drawn fresh attention after a Zacks report highlighted its 75.6% year-to-date return and a favorable Rank #2 rating, with analysts pointing to improving earnings estimates as a key driver.

At a share price of $339.88, ESCO Technologies has had a strong run, with the 30 day share price return of 16.44% feeding into a year to date share price return of 71.99% and a 3 year total shareholder return of 230.27%. This suggests that recent momentum has built on an already strong longer term record.

If ESCO Technologies’ surge has you thinking about where else strong execution might show up, this could be a good moment to broaden your search and check out 35 power grid technology and infrastructure stocks

With ESCO Technologies now trading near US$340 after strong recent gains, the key question is whether current earnings and analyst expectations justify this price, or if the stock is already pricing in much of its potential future performance.

Most Popular Narrative: 19.1% Undervalued

Compared with ESCO Technologies' last close at $339.88, the most followed narrative assigns a Fair Value of $420, building a case around multi segment growth and capital allocation.

The divestiture of VACCO and strong balance sheet provide ESCO with significant dry powder to pursue further high-ROIC bolt-on acquisitions in adjacent markets, which could accelerate the top-line growth trajectory and drive further expansion in net margins through operational leverage and portfolio mix upgrade.

Curious how this acquisition heavy playbook supports that higher Fair Value for ESCO Technologies? The narrative leans on fast compounding revenues, steady margins, and a premium future earnings multiple that is usually reserved for very different sectors.

Result: Fair Value of $420 (UNDERVALUED)

However, the bullish ESCO Technologies narrative also relies on continued government and utility spending, as well as on successful integration of acquisitions like Maritime, both of which can disappoint.

Another View: ESCO Technologies Through a Cash Flow Lens

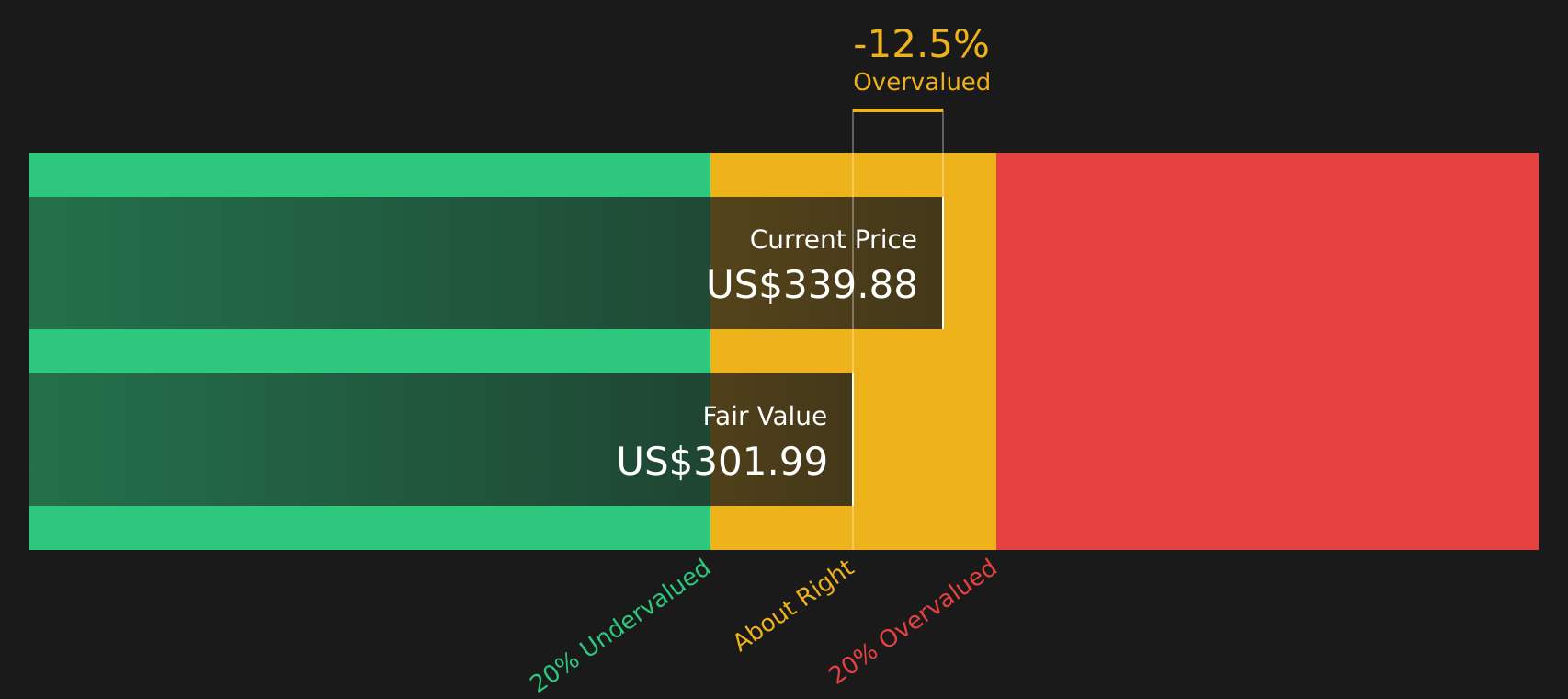

While the most popular ESCO Technologies narrative points to a Fair Value of $420 based on growth, margins, and a rich future P/E, the SWS DCF model tells a cooler story. On that cash flow view, the stock at $339.88 sits above an estimate of $301.99, which screens as overvalued rather than undervalued. For a position that has already enjoyed a strong run, how comfortable are you if future cash generation ends up closer to this more cautious scenario?

For a closer look at how those cash flow assumptions stack up against the growth narrative, take a moment with the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ESCO Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment around ESCO Technologies split between upside potential and richer pricing, this is a good time to look at the numbers yourself and move quickly to form your own view, starting with the 2 key rewards.

Looking for more investment ideas beyond ESCO Technologies?

If ESCO Technologies has sharpened your interest, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Spot potential turnaround stories early by scanning 21 elite penny stocks with strong financials that already show stronger financial footing than many investors might expect.

- Focus on quality at a sensible price by checking 44 high quality undervalued stocks that pair healthier balance sheets with cash flows that support their current market value.

- Prioritize staying power and capital preservation by reviewing 71 resilient stocks with low risk scores that score well on resilience while still offering room for investor interest to build.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.