Estée Lauder (EL) Returns To Quarterly Profit With US$0.45 EPS Challenging Bearish Narratives

Estee Lauder Companies Inc. Class A EL | 69.12 | -2.25% |

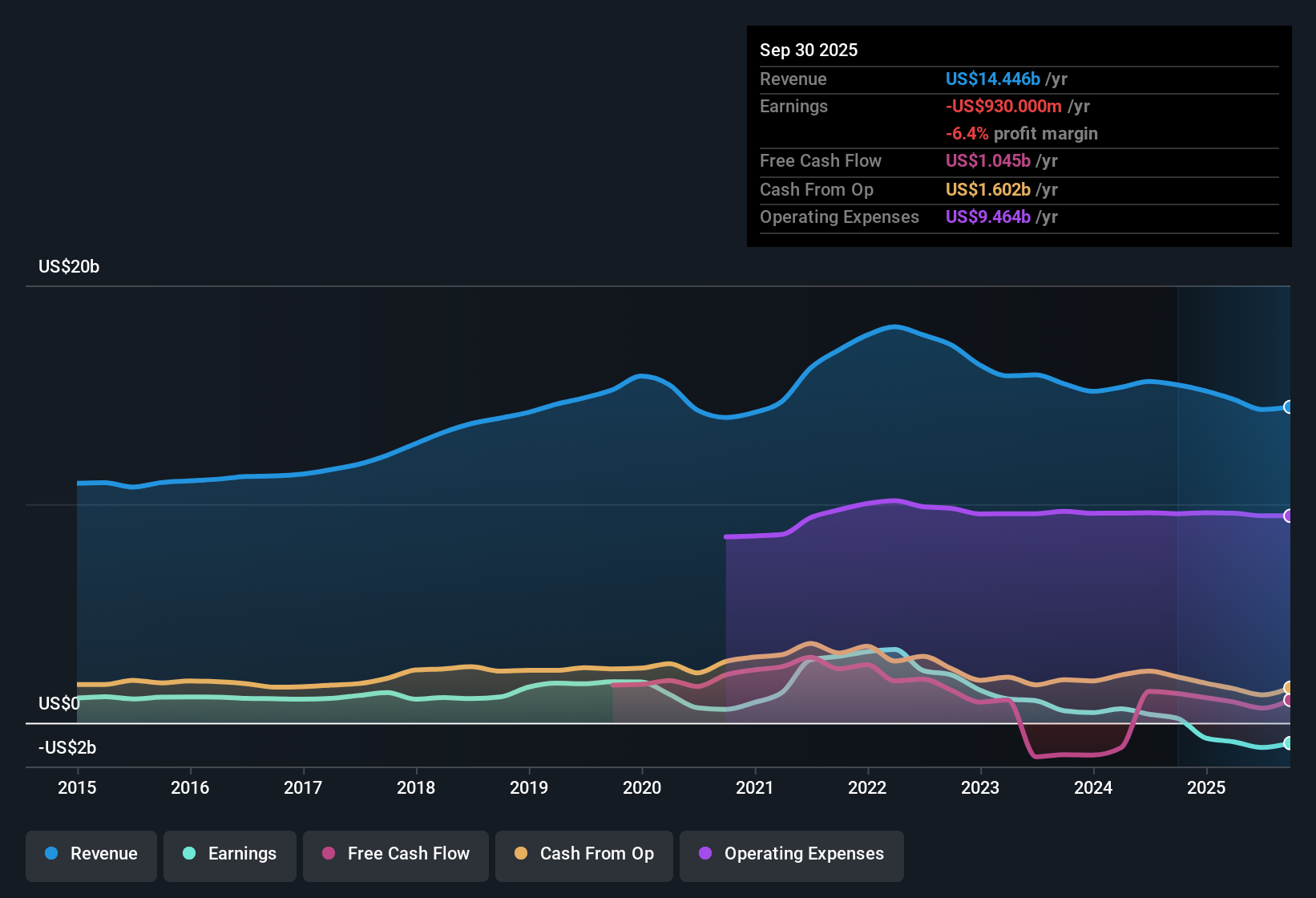

Estée Lauder Companies (EL) just posted Q2 2026 results with revenue of US$4.2 billion and basic EPS of US$0.45, alongside net income of US$162 million, putting the latest quarter firmly back in profit territory. Over the past few quarters, revenue has moved from US$3.4 billion in Q1 2025 and US$4.0 billion in Q2 2025 to US$3.5 billion in Q3 2025, US$3.4 billion in Q4 2025, US$3.5 billion in Q1 2026, and now US$4.2 billion in Q2 2026. Basic EPS has ranged from losses of US$1.64 in Q2 2025 and US$1.51 in Q4 2025 to positive US$0.44 in Q3 2025, US$0.13 in Q1 2026, and US$0.45 this quarter. This sets up a results season where investors will focus squarely on how durable this shift in profitability and margins really is.

See our full analysis for Estée Lauder Companies.With the latest numbers on the table, the next step is to see how this earnings print lines up with the prevailing market narratives about Estée Lauder and where those stories might need an update.

TTM still in loss at US$178 million

- Across the last twelve months, Estée Lauder recorded a net loss of US$178 million on US$14.7b of revenue, even though Q2 2026 itself was back in profit with US$162 million of net income.

- What stands out for the bearish view is that losses over the past five years have grown at about 54.8% per year,

- critics highlight that this longer trend of widening losses sits alongside only modest forecast revenue growth of 4.4% per year versus a 10.2% US market figure.

- the same bears also point to the high debt load and a 1.41% dividend yield that is not covered by current earnings as signs the recent profitable quarter has not yet changed the bigger picture.

Revenue at US$4.2b, but growth running behind market

- Q2 2026 revenue of US$4.2b contributes to trailing twelve month revenue of US$14.7b, while forecasts point to 4.4% annual revenue growth compared with a 10.2% figure for the broader US market.

- Supporters of a more bullish take argue that the key driver is not top line outpacing the market but a swing back to profitability,

- and they point to Q2 2026 basic EPS of US$0.45 and Q1 2026 EPS of US$0.13 as evidence that per share results can return to positive territory after several loss making quarters.

- at the same time, earnings are forecast to grow about 41.52% per year with an expected return to profitability within three years, so bulls focus more on that projected earnings path than on the slower revenue growth rate.

Mixed valuation signals at US$99.47 share price

- At a current share price of US$99.47, the stock sits about 13.5% below an indicated DCF fair value of roughly US$115.06, yet it trades on a P/S of 2.5x compared with 2x for peers and 1x for the US Personal Products industry.

- Consensus style thinking often weighs this gap against earnings and balance sheet data,

- since the trailing twelve month EPS is a loss of US$0.49 despite recent quarterly profits, investors see that P/S premium as harder to justify purely on current profitability.

- however, with forecasts calling for a return to profitability within three years, some see the current discount to DCF fair value as reflecting that expected earnings recovery while still leaving room for questions about the higher multiples versus peers.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Estée Lauder Companies's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Estée Lauder is still working through a trailing twelve month loss of US$178 million, slower forecast revenue growth, and a dividend not covered by current earnings.

If you are uneasy about those earnings pressures and balance sheet questions, take a few minutes to assess companies in our solid balance sheet and fundamentals stocks screener (45 results) that aim to prioritise financial strength and resilience right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.