Eton Pharmaceuticals (ETON) Could Be 18% Undervalued As Valuation Questions Build

Eton Pharmaceuticals, Inc. ETON | 0.00 |

Eton Pharmaceuticals (ETON) came into focus after Chief Business Officer David Krempa exercised 10,000 Restricted Stock Units, converting them into common shares as part of a multi-year equity grant.

The recent equity grant vesting comes at a time when Eton Pharmaceuticals’ share price has moved to $37.51, with a 30-day share price return of 18.74% and a year-to-date share price return of 130.69%, while the 1-year total shareholder return stands at 159.94% and the 3-year total shareholder return is above 10x. This points to strong momentum over both shorter and longer periods.

If this kind of move has caught your attention, it can be a useful moment to broaden your watchlist with other opportunities using the Simply Wall St screener for 40 healthcare AI stocks

After a move like Eton Pharmaceuticals has just logged, some investors see a long runway still open, while others suspect most of the upside is already in the rear view mirror. What does the current valuation actually suggest?

Most Popular Narrative: 18% Undervalued

On the most followed view, Eton Pharmaceuticals’ fair value of $45.67 sits above the last close at $37.51, framing the recent rally as only part of a bigger story.

Eton's investments in digital patient support platforms, targeted education campaigns, and specialist distribution (e.g., Eton Cares) are removing historical barriers to access and supporting higher therapy adoption and retention, driving increased penetration in niche markets and supporting recurring revenues.

Want to see what kind of revenue ramp, margin profile, and future earnings power this narrative is baking in for Eton Pharmaceuticals? The projections tie together rapid top line expansion, a sharp profitability swing, and a future valuation multiple more commonly associated with mature compounders, not a company that is reporting a small loss today. The details behind that jump are where the story really gets interesting.

Result: Fair Value of $45.67 (UNDERVALUED)

However, Eton Pharmaceuticals still faces real pressure points, including its reliance on a concentrated rare disease portfolio and the risk that payer or government pricing decisions undercut the current thesis.

Another View on Eton Pharmaceuticals’ Valuation

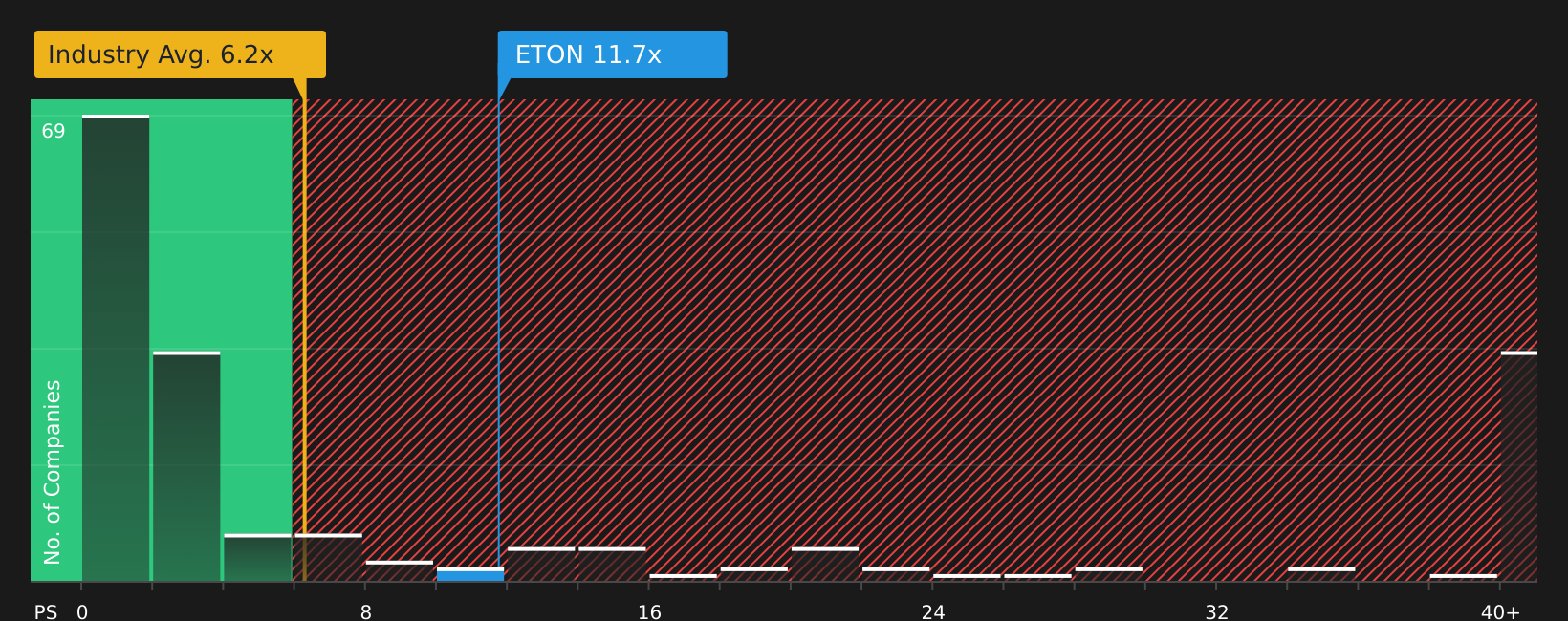

While the narrative and analyst targets frame Eton Pharmaceuticals as undervalued at $37.51 versus a $45.67 fair value, the current P/S ratio of 11.8x tells a tougher story. It sits well above the US pharmaceuticals industry at 6.4x, the peer average at 5.1x, and even the fair ratio of 7.3x. This suggests the market could move toward a lower multiple over time. Is this a case of growth expectations justifying the premium, or are investors paying too far in advance for future outcomes?

Next Steps

With both enthusiasm and concern in the mix for Eton Pharmaceuticals, it makes sense to move quickly and test the story against your own judgement using the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Eton Pharmaceuticals?

If you want to keep building on what you have seen with Eton Pharmaceuticals, do not sit on the sidelines while other opportunities line up.

- Target consistent cash generators by scanning companies built around meaningful shareholder payouts with the 8 dividend fortresses.

- Zero in on potential value opportunities by filtering for companies that pair quality fundamentals with appealing pricing using the 44 high quality undervalued stocks.

- Protect your downside by reviewing stocks that score well on resilience and risk metrics through the 79 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.