Europe's AI Push Faces Major Roadblock: High Energy Costs Threaten Industrial Competitiveness

Artificial intelligence (AI) has started to deliver measurable gains in European Union (EU) manufacturing sectors. But the bigger question – whether the bloc can compete with China and the US without the cheap power required for advanced AI compute – now sits at the center of Europe's industrial future.

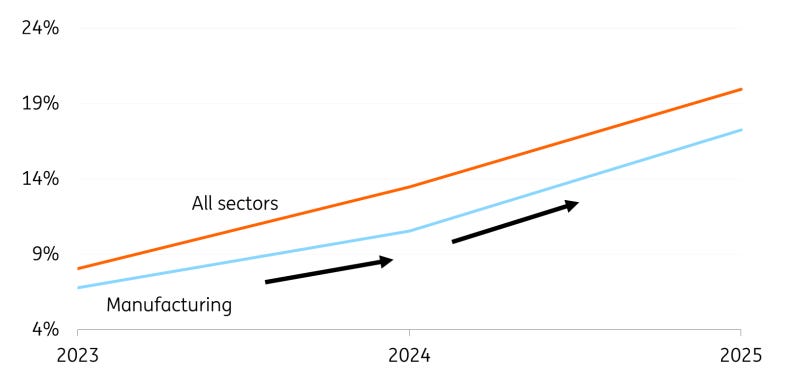

Adoption of AI in the EU has doubled since 2023, with 17% of all manufacturers using the technology to boost productivity and efficiency. Yet, the number still lags the broader economy and its peers in the US and China.

At stake is whether Europe can translate early AI gains into long‑term competitiveness — or fall further behind rivals with deeper compute capacity and cheaper energy.

Today, over 75% of the world's advanced AI compute sits in the US, with China coming in second at around 15%, according to Nina Schick, a Sovereign AI Strategist. Europe has less than 4%, she said, leaving Europe's industrial backbone under-optimized.

The EU has hobbled its competitiveness in AI with "Caligulan" bureaucracy, over-regulation, and "lethally" high energy prices. The latest jump in inflation, driven by higher energy prices in March after the conflict in the Middle East, underscores the fragility of the European energy market.

"Europe needs deregulation, lower taxes, lower energy prices, and reindustrialization," Jacob S. Helberg, the US Under Secretary of State for Economic Affairs, said in Brussels on Wednesday. "Europe desperately needs these reforms, not because Washington demands it. Because the evidence demands it."

Upside for EU Is Substantial

The European Central Bank (ECB) has estimated that AI could boost euro area productivity by more than 4% over the next decade. The potential upside for EU manufacturers is substantial, assuming favorable conditions.

Firm-level studies suggest AI adoption can increase annual employee productivity growth by as much as three percentage points, according to a March 24 report by ING Think.

"Manufacturing companies that implement AI tend to outperform competitors that don't, both in terms of productivity and market share," Edse Dantuma, ING economist, said in the report. "While the benefits vary by task and therefore by company, the industry is at risk of falling behind on a major new technology with potentially significant productivity gains."

The ING's analysis pointed to the overlooked winner of AI adoption. Logistics, supply chains, procurement, customer service, and engineering workflows will represent vast opportunities for efficiency gains.

"The greatest potential of AI is not in the core process of production itself," Dantuma noted.

AI Applications Have Real‑World Benefits

AI applications are not abstract — they have real‑world productivity benefits.

They can reliably predict when machinery will fail, reducing downtime by 35–45% and maintenance costs by 25–30%. They can also optimize inventory across complex supply chains, lowering inventory carrying costs by 15–30%, depending on the application.

Generative AI can accelerate product design cycles by producing and testing virtual prototypes. Companies have reported up to an 87% reduction in design time, while virtual prototyping has been associated with a 75% reduction in development time and a 50% reduction in development costs.

For a continent grappling with labor shortages and demographic decline, this is not just an opportunity—it is a necessity. AI also offers a partial solution to Europe's chronic skills gap by automating repetitive tasks and allowing workers to focus on higher-value activities.

Siemens AG has reduced automation costs at its Erlangen plant in Germany by 90% in certain assembly steps by deploying AI-driven robots that pick up various parts and materials and place them in automated assembly lines.

EU's Path to Scaling Is Uncertain

Yet the EU's path to scaling these AI gains is uneven. Adoption varies widely by firm size and geography.

Large companies are three times more likely to use AI than smaller firms, highlighting a structural divide that could widen over time. Meanwhile, uptake differs sharply between countries, with Northern Europe leading and parts of Eastern Europe lagging.

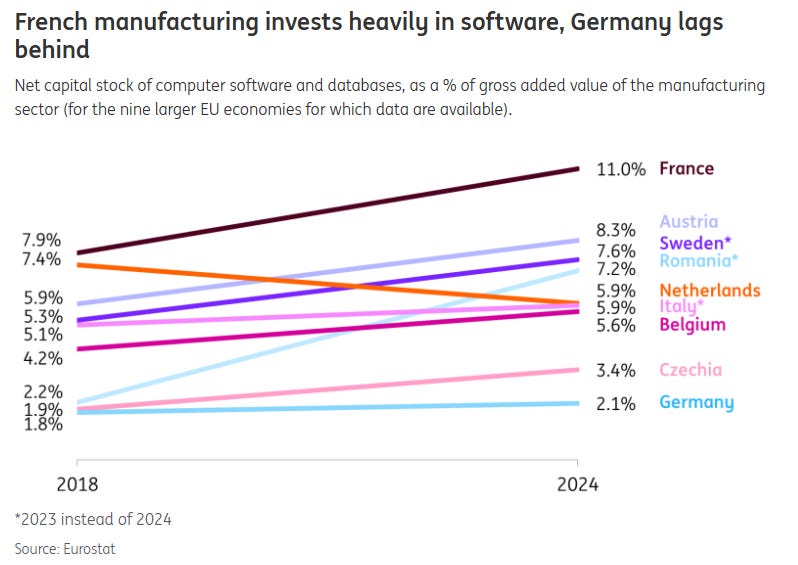

Germany, Europe's biggest economy, will have to make significant progress in the field of AI, according to ING Think. In 2024, software ownership amounted to only 2.1% of added value. This is considerably lower than the average of 6.3%. France tops the list with 11.0%, followed by Austria at 8.3% and Sweden at 7.6%.

The challenge is not purely technological. Organizational and cultural barriers remain significant. Many firms struggle to integrate AI into workflows, and pilot projects often fail to scale.

"Research shows that 95% of GenAI pilots fail because organizations try to avoid friction," said Dantuma.

Thus, a successful AI transformation requires leadership, strategy, and a willingness to rethink the old processes.

EU Has a Physical AI Advantage

For the World Economic Forum (WEF), the question is not where the gains are, but rather, how Europe might compete structurally. WEF has argued that Europe is unlikely to win a head-on battle in software-centric AI, where US tech giants dominate.

Instead, its advantage lies in physical AI — the integration of AI into machines, infrastructure, and industrial systems. Siemens and ASML Holding NV lead among publicly traded European companies in physical‑AI applications.

These companies are well-positioned to deploy AI to enhance physical processes, from robotics to logistics. Other examples include Swedish industrial equipment manufacturer Atlas Copco and Finland's lifting equipment leader Konecranes.

But this model depends heavily on coordination. Physical AI requires large volumes of real-world data, often spanning multiple firms and sectors. No single company can generate enough data to train robust models on its own.

"The silver bullet isn't new tech," Richard Forrest, CEO of Kearney Europe, wrote. "It's collaboration."

Europe Starts in a Position of Weakness

Europe has started from a position of relative weakness. Only 3% of euro-area patents are AI-related, compared to about 9% for the US, and it lags behind in advanced AI computing.

Europe also pays substantial royalties to foreign technology holders, underscoring dependence on external innovation. Limited access to capital further constrains firms' ability to scale new technologies.

"The greatest impact will be achieved if AI materially boosts the pace of innovation," Philip Lane, Chief Economist at the ECB, said in a speech on March 23. "This could increase the long-run potential growth rate."

The outcomes depend heavily on the speed and breadth of adoption, particularly among smaller firms, he added. Larger manufacturing companies with 250 or more employees use AI three times as often (namely 64% of the total) as smaller companies with 10 to 50 employees (21%), according to ING Think.

EU Has a Sobering Energy Problem

Layered on top of these structural challenges is an impossible-to-ignore constraint. AI is an energy-intensive technology.

Global data-center electricity consumption will more than double by 2030, reaching 945 terawatt-hours, exceeding Japan's current consumption, according to the International Energy Agency. Training large models, running data centers, and deploying industrial AI systems all require vast amounts of electricity.

As global demand for computing rises, access to cheap, reliable power has become a decisive competitive factor. Energy costs directly shape the economics of data centers, AI training, and industrial deployment, with higher prices translating into slower adoption and reduced competitiveness at the very moment global rivals are scaling up.

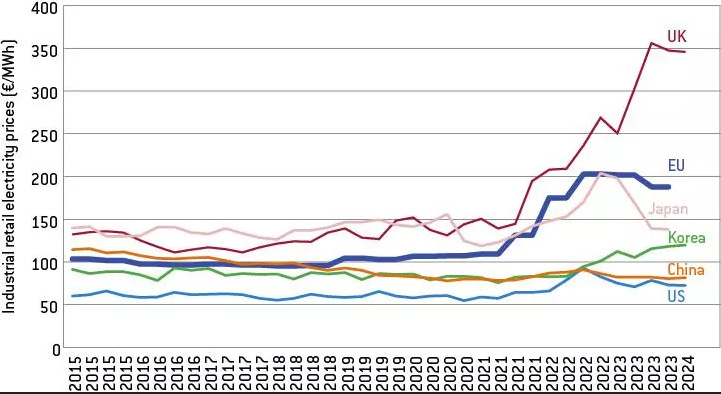

Europe's position here is precarious. Industrial electricity prices are significantly higher than in the US and China, reflecting both structural market design and dependence on imported fuels.

Europe Remains Dependent on Imported Energy

Europe remains heavily dependent on imported fossil fuels. As a result, price shocks — such as those triggered by conflict in the Middle East — have already begun to impact the euro area.

Annual inflation climbed to 2.5% in March, up from 1.9% in February, driven by the Middle East conflict. The Consumer Price Trend over the next 12 months in the euro area increased on Monday to 43.40 points in March from 26.20 points in February.

"The winner of the next industrial revolution will not be the region with the best engineers," said David Frykman, a General Partner at Norrsken VC. "It will be the region that can deliver the cheapest, most abundant power."

For Europe, the race to scale AI may ultimately be a race to secure affordable power — and the clock is already ticking.

Disclaimer: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. European Capital Insights is not responsible for any financial decisions made based on the contents of this article. Readers may use this article for information and educational purposes only.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.