Evaluating AZZ After Its Strong 31% Rally and Recent Industrial Strength in 2025

AZZ Inc. AZZ | 0.00 |

If you are wondering what to do with AZZ after its impressive rally, you are not alone. This is a stock that refuses to sit still. Despite a modest slip of 0.7% over the past week and a 7.3% dip in the past month, AZZ’s shareholders have every reason to feel upbeat. The year-to-date return stands tall at 30.7%, and over the past year, shares have soared 33.1%. The real jaw-dropper is that over the last three and five years, AZZ has delivered gains of 188.0% and 210.0%, respectively. Not many stocks can match that kind of compounding momentum.

What is fueling these movements? Much of AZZ's growth seems driven by broader industrial demand and investor optimism surrounding infrastructure and energy trends. While short-term volatility has created some nerves lately, a longer view paints a picture of consistently strengthening fundamentals and an increasingly favorable market perception of AZZ’s risk profile.

So, is the stock’s current price justified, or is the market getting ahead of itself? According to a widely used valuation scoring system, AZZ checks the box as undervalued in 3 out of 6 categories and earns a value score of 3. That means it looks reasonably priced—but only by half the usual valuation standards. Of course, traditional methods do not always tell the whole story. In the next section, we will break down the valuation approaches that matter and at the end, reveal an even more insightful way to gauge whether AZZ is truly a buy right now.

Approach 1: AZZ Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) approach estimates a company's value by projecting its future cash flows and discounting them back to their present value. For AZZ, this model relies on anticipated cash flows over the next decade to judge what the stock should be worth today.

Currently, AZZ generates $396.43 million in free cash flow, with analysts projecting incremental growth for the next five years. Notably, free cash flow is expected to reach $218 million by 2028 according to current forecasts. Beyond that, further growth is estimated based on conservative assumptions. Over a full 10-year span, the annual free cash flow outlook fluctuates, reflecting both analyst inputs through 2028 and more cautious projections after that.

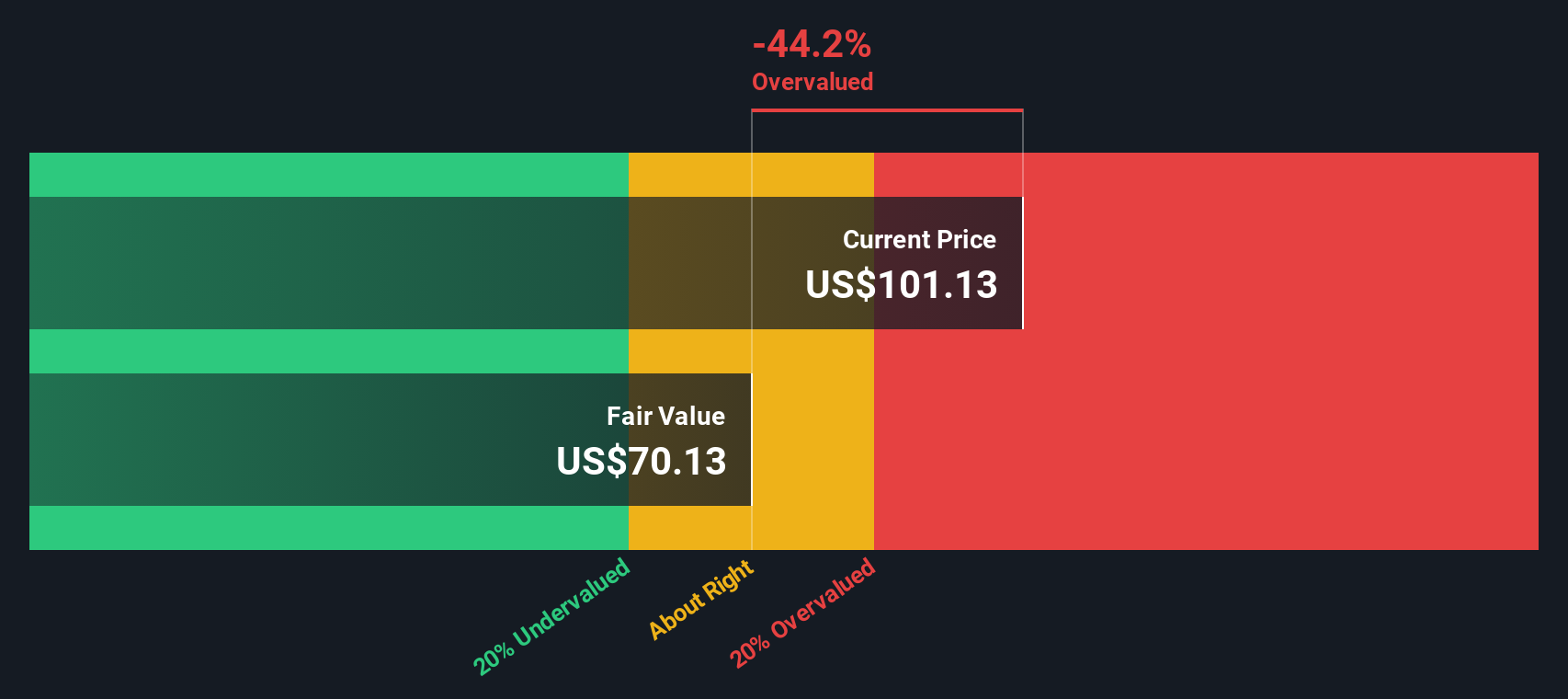

Based on these calculations, the DCF model produces an intrinsic value for AZZ of $83.68 per share. This figure is nearly 29.5% below AZZ's current market price, indicating that, by this estimate, the stock is noticeably overvalued when considering its presently expected cash flow growth.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AZZ may be overvalued by 29.5%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: AZZ Price vs Earnings

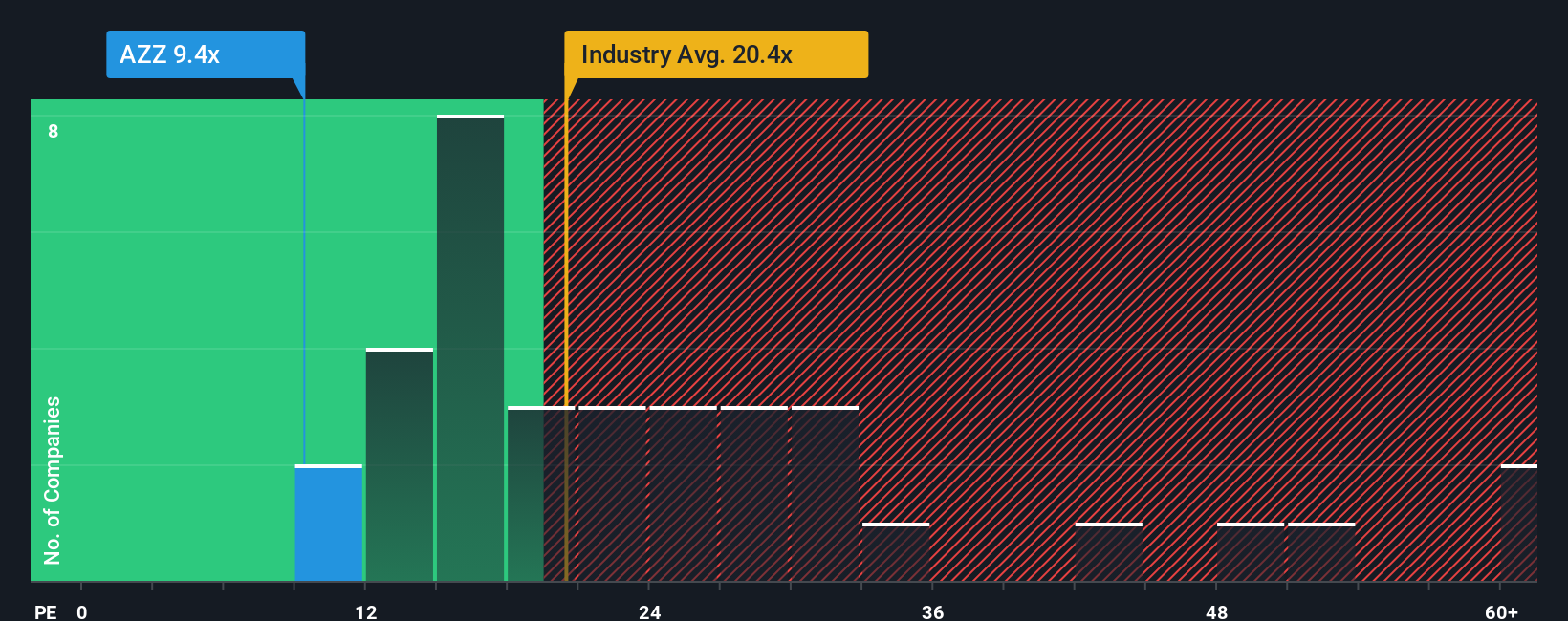

For a company like AZZ that has consistent profitability, the price-to-earnings (PE) ratio is a particularly meaningful valuation yardstick. This metric shows how much investors are willing to pay today for $1 of the company’s earnings, which makes it especially relevant for companies with a steady track record of profit. Generally, a higher PE reflects expectations of stronger growth and lower perceived risk. A lower PE can suggest the market sees limited upside or greater uncertainty ahead.

AZZ’s current PE is 12.5x. To put this in context, it sits well below the industry average PE of 22.4x and even further beneath the peer average of 31.2x. On the surface, this looks like AZZ is trading at a significant discount to both its sector and its closest competitors.

However, there is more nuance when you apply Simply Wall St’s proprietary "Fair Ratio." This is a tailored metric that blends company-specific factors such as earnings growth, profit margins, business risks, market cap, and its precise place within the Building industry. Unlike a raw comparison against the industry or a handful of peers, the Fair Ratio aims to deliver a fairer benchmark based on AZZ’s unique fundamentals. In this case, the Fair Ratio for AZZ is 13.4x.

With AZZ trading at 12.5x versus a Fair Ratio of 13.4x, the stock is modestly undervalued on a PE basis. This suggests investors are paying slightly less than what is fair given the company’s outlook and profile.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AZZ Narrative

Earlier we hinted at a more powerful way to understand valuation. Meet Narratives. In essence, a Narrative tells the story behind the numbers: it is your own perspective on a company’s future, connecting what you believe about AZZ’s business outlook to your assumptions for revenue, margins, earnings and ultimately a fair value for the shares.

Unlike static ratios or models, Narratives blend a company’s real-world story and strategy with a personalized financial forecast, enabling you to see how your expectations would drive valuation. This approach lets you map out how changes in demand, margins or market position could shift what AZZ is actually worth. Narratives are also an accessible tool on Simply Wall St’s Community page, used by millions of investors to collaborate and compare views.

By creating or following different Narratives, you can easily compare the resulting Fair Value to the current share price. This can help you decide whether to buy, hold or sell. Narratives are refreshed automatically as new data comes in, such as updates from earnings or news events, ensuring your valuation view stays relevant.

For example, one recent Narrative for AZZ assumes robust production growth and sustained capital efficiency, resulting in a bullish fair value of $141.00 per share. Another more cautious estimate, factoring in margin pressure and integration risks, puts a fair value at $105.00. By exploring these perspectives, you can decide what makes sense for your own investment strategy rather than relying solely on conventional metrics.

Do you think there's more to the story for AZZ? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.