Evaluating Carrier Global (CARR) After Portfolio Exit And HVAC Focus Shape Investor Expectations

Carrier Global Corp. CARR | 55.71 | -2.09% |

Carrier Global (CARR) has just finished exiting its non-core operations and is now centered on HVAC and climate solutions, as investors watch upcoming earnings and a dividend payment alongside regulatory and heat pump trends.

Carrier Global’s share price has climbed 11.32% year to date and delivered a 12.76% 1 month share price return. Its 1 year total shareholder return of a 7.56% decline contrasts with 3 and 5 year total shareholder returns of 32.51% and 63.06%. This suggests recent momentum is improving while longer term holders have still seen meaningful gains.

If you are looking beyond HVAC and climate solutions for climate or electrification themes, this could be a good moment to scan auto manufacturers for other ideas linked to efficiency and energy transition.

With Carrier Global now focused on climate and HVAC, an 11.32% year-to-date gain, modest revenue and net income growth, and the share price sitting below one valuation estimate, is there still a buying opportunity here, or is the market already pricing in future growth?

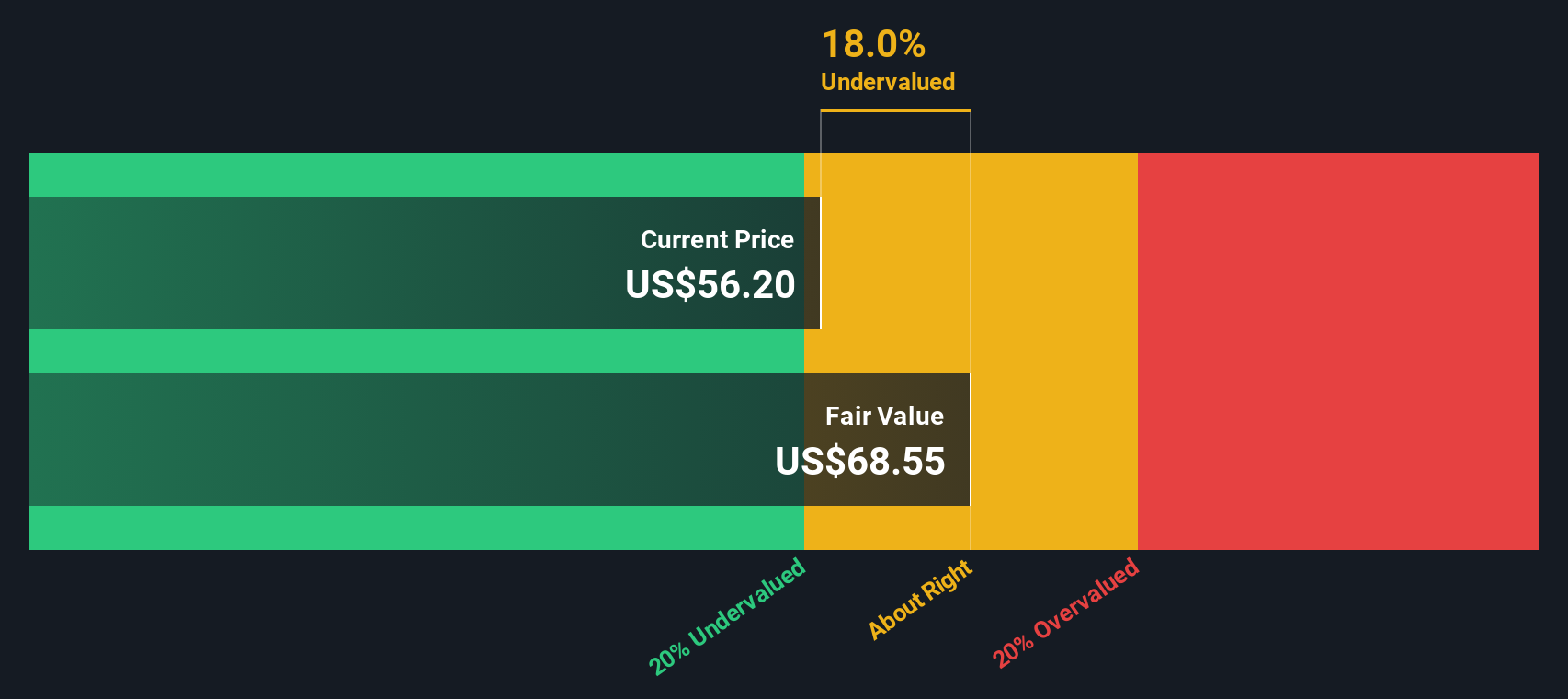

Most Popular Narrative: 16.4% Undervalued

Against Carrier Global’s last close of $59.58, the most followed narrative points to a fair value of $71.24, supported by a detailed long term cash flow view.

The company's efforts in operational efficiency, such as using Carrier Excellence to enhance productivity and mitigate tariff impacts through cost containment and supply chain adjustments, are likely to support margin expansion and improved earnings per share.

Want to see what is behind that earnings uplift story? The narrative focuses on revenue growth, margin expansion and a future earnings multiple that needs careful scrutiny.

Result: Fair Value of $71.24 (UNDERVALUED)

However, there are still pressure points to watch, including tariff exposure that could weigh on margins, as well as softer demand in certain regions or light commercial HVAC weighing on sales.

Another Angle On Valuation

Our SWS DCF model suggests Carrier Global at $59.58 sits about 5.7% below an estimated fair value of $63.18, so it appears only mildly undervalued compared with the much larger 16.4% gap implied by the narrative. Which view better fits the level of risk you are comfortable taking?

Build Your Own Carrier Global Narrative

If you see Carrier differently, or simply prefer to weigh the assumptions yourself, you can stress test the numbers and Do it your way in under 3 minutes.

A great starting point for your Carrier Global research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Carrier Global caught your eye, do not stop here. Broaden your watchlist with focused screens that can surface different types of opportunities in just a few minutes.

- Target potential mispricing by checking out these 868 undervalued stocks based on cash flows that may trade below their implied worth on cash flow measures.

- Tap into growth themes by scanning these 25 AI penny stocks that are tied to artificial intelligence trends and related demand.

- Strengthen your income watchlist by filtering for these 14 dividend stocks with yields > 3% that might align with your yield expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.