Evaluating CNX Resources (CNX) After Earnings Beat And Expanded Share Buyback Authorization

CNX Resources Corporation CNX | 38.71 | +0.73% |

CNX Resources (CNX) is back in focus after reporting fourth quarter 2025 results that came in well ahead of expectations, along with a large expansion of its existing share repurchase authorization.

The earnings beat and expanded buyback have come alongside steady share price momentum, with a 1 month share price return of 6.42% and a 3 month share price return of 13.19%. Over a longer horizon, CNX Resources has delivered a 1 year total shareholder return of 40.58% and a 5 year total shareholder return of 198.00%. This indicates that recent gains are building on already strong longer term performance rather than a short lived spike.

If CNX Resources has caught your attention, this could be a moment to see what else is happening across energy. You can scan similar producers and infrastructure names via aerospace and defense stocks.

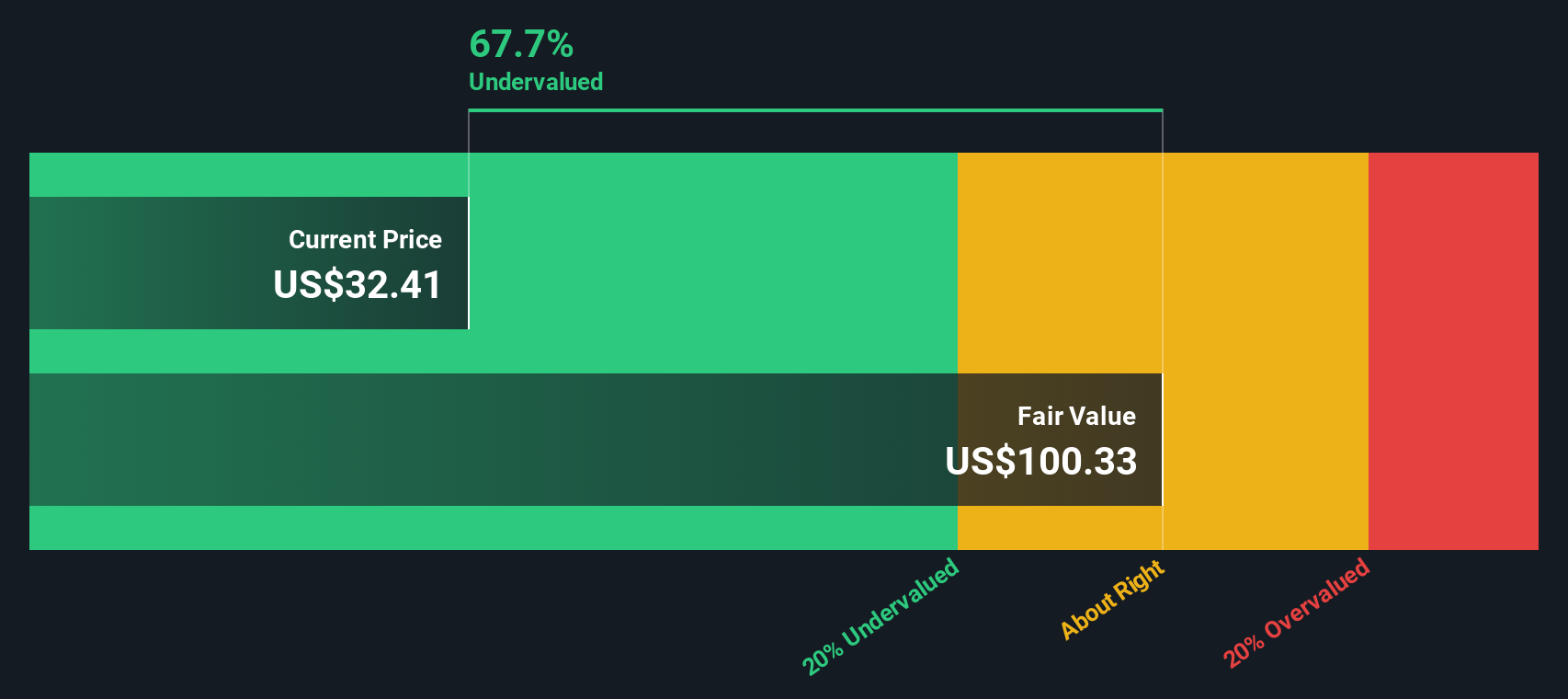

With a value score of 5, a reported intrinsic discount of about 65%, and a share price that sits above the average analyst target, the key question now is whether CNX is still mispriced or if the market is already looking ahead and incorporating potential future growth.

Most Popular Narrative: 10% Overvalued

With CNX Resources at a last close of $38.80 against a narrative fair value of about $35.29, the current price sits above that widely followed view while still implying a constructive long term story.

Favorable policy and regulatory shifts towards cleaner burning natural gas, including programs like 45Z tax credits and renewable energy attribute markets, are creating new, high margin revenue streams (e.g., RMG sales, environmental credits), potentially enhancing both net margins and free cash flow.

Want to see what kind of revenue mix could support that gap between fair value and today’s price? The narrative leans on faster top line expansion, wider margins and a future earnings profile that looks very different from today. Curious which specific growth and profitability assumptions sit underneath that conclusion and how they stack up over the next few years? Read on to see how the full thesis fits together.

Result: Fair Value of $35.29 (OVERVALUED)

However, this narrative can unravel if expected tax credits and environmental revenues do not materialize as assumed, or if in-basin demand growth for gas falls short of projections.

Another Take On Value

While the consensus narrative sees CNX Resources as about 10% overvalued versus a fair value of $35.29, our DCF model paints a very different picture. On that view, the stock at $38.80 trades at roughly a 65% discount to an estimated value of $110.99. Which version of fair value do you think lines up better with your expectations for cash generation?

Build Your Own CNX Resources Narrative

If you see the assumptions differently, or simply prefer to work from the raw numbers yourself, you can test your own version of the story in just a few minutes: Do it your way.

A great starting point for your CNX Resources research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. The right screen can quickly surface ideas you might otherwise miss.

- Spot potential value early by scanning these 3538 penny stocks with strong financials that pair low share prices with solid underlying financials.

- Ride the AI trend with focus by checking out these 24 AI penny stocks that concentrate on artificial intelligence themes.

- Seek dependable income by reviewing these 12 dividend stocks with yields > 3% that highlight companies with yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.