Evaluating Emerson Electric (EMR) After Recent Share Price Weakness And Mixed Valuation Signals

Emerson Electric Co. EMR | 0.00 |

Why Emerson Electric (EMR) Is On Investors’ Radar

Emerson Electric (EMR) has drawn attention after recent trading, with the stock closing at US$133.05. Investors are weighing this price against the company’s current fundamentals and its recent share price performance.

Recent trading has been softer, with the share price down 3.5% over the last session and 10.2% over 90 days. However, the 1 year total shareholder return sits at 12.1% and the 3 year total shareholder return at 70.4%, suggesting longer term holders have still seen solid compounding.

If this kind of industrial automation story interests you, it could be a good moment to broaden your search and check out 38 power grid technology and infrastructure stocks

With Emerson shares easing in recent months despite positive multi year returns and reported revenue and net income growth, the key question is simple: is today’s valuation leaving upside on the table, or already reflecting future growth?

Most Popular Narrative: 19.1% Undervalued

Emerson Electric’s most followed narrative sets a fair value of about $164.51 per share, comfortably above the last close at $133.05, and anchors that view on multi year demand for automation and software led solutions.

The accelerating adoption of digital automation and artificial intelligence solutions in global industrial markets is fueling strong demand for Emerson's advanced software platforms and AI-enabled products, such as Ovation 4.0 and Nigel AI adviser, which is resulting in robust order growth and positions the company for sustained revenue expansion.

Curious what sits behind that confidence in future cash flows? The narrative leans heavily on multi year revenue growth, rising margins, and a premium earnings multiple to back into that fair value.

Result: Fair Value of $164.51 (UNDERVALUED)

However, investors still need to watch for tariff and FX pressures on margins, as well as any slowdown in AspenTech or wider industrial software momentum that could challenge this upbeat narrative.

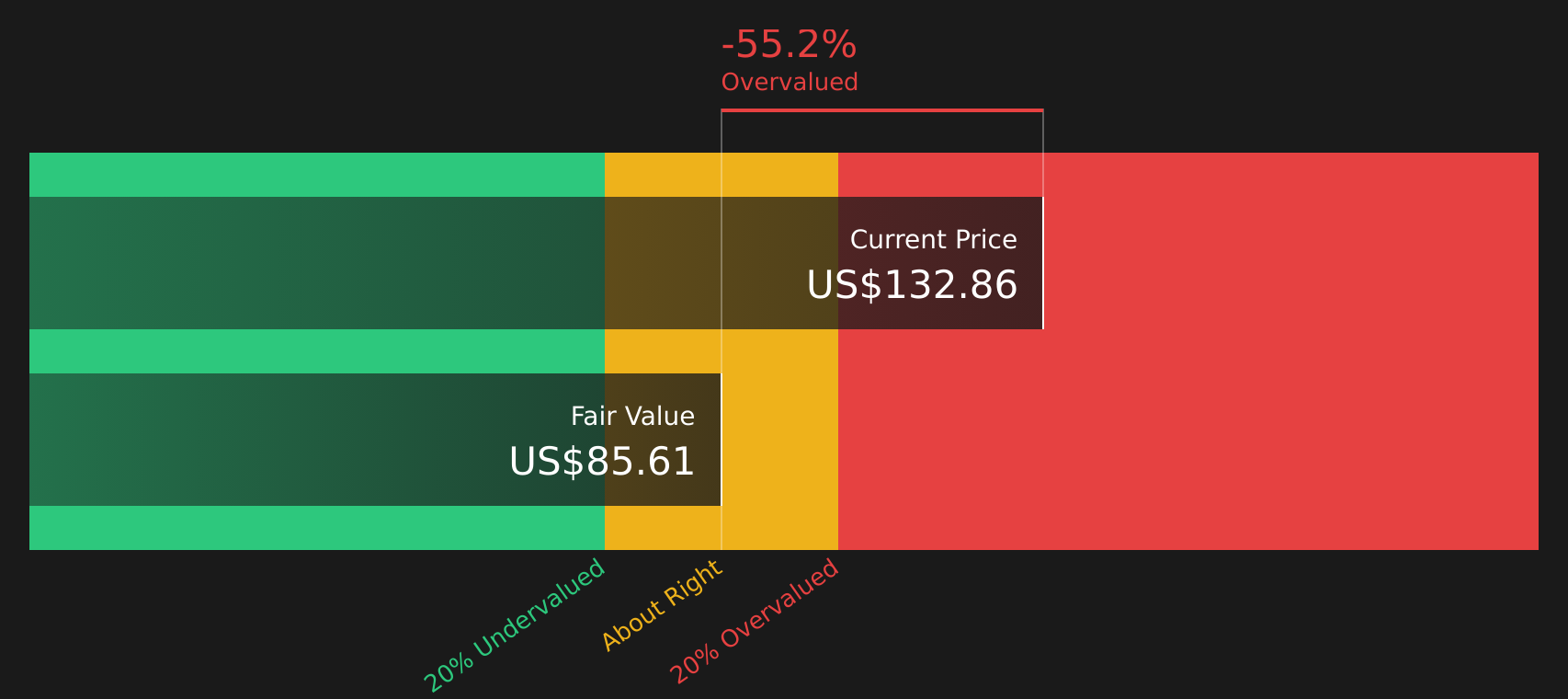

Another Angle On Valuation

The SWS DCF model presents a very different picture. On this view, Emerson Electric’s estimated future cash flow value sits at about $84.83 per share, which is well below the current $133.05 price and suggests that the shares may be overvalued. When one method implies upside and another signals caution, which set of assumptions seems more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models, are you leaning bullish or cautious on Emerson Electric? Act while the data is fresh and weigh both sides by checking the 6 key rewards and 1 important warning sign

Looking for more investment ideas?

If Emerson Electric has your attention, do not stop here. Broaden your watchlist now so you do not miss other opportunities building below the surface.

- Target potential bargains by scanning companies that combine strong fundamentals with prices that still look appealing using the 49 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that offer 5%+ yields and aim for resilience with the 12 dividend fortresses.

- Reduce unpleasant surprises by focusing on companies with steadier profiles and quality scores through the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.