Evaluating Intuit (INTU) After AI Jitters OpenAI Enterprise Launch And Analyst Downgrades

Intuit Inc. INTU | 422.48 | -0.80% |

Intuit (INTU) is back in focus after a steep selloff in software stocks, as fresh AI disruption worries, OpenAI’s new enterprise platform, and analyst downgrades collide with new product partnerships such as Affirm integration.

Those AI worries and analyst downgrades have shown up clearly in the chart, with Intuit’s share price down 32.8% on a 1 month basis and 30.9% year to date, while the 5 year total shareholder return of 9.8% is far less dramatic. Recent headlines, from OpenAI’s enterprise launch to the new Affirm and Checkr integrations plus pre earnings nerves, have reinforced a sense that momentum is fading in the short term even as the business keeps signing new partnerships.

If this AI driven selloff has you looking beyond a single ticker, it could be a good moment to scan 56 profitable AI stocks that aren't just burning cash for ideas that pair AI exposure with existing profitability.

With Intuit now trading 45% below one intrinsic value estimate and at roughly a 21x forward P/E based on analyst forecasts, is this AI driven reset creating a genuine entry point, or is it simply bringing expectations closer to already priced-in growth?

Most Popular Narrative: 44.8% Undervalued

With Intuit last closing at $434.91 against a most followed fair value of about $787.76, the current reset sits well below that narrative line in the sand and puts extra weight on the growth and margin story behind those numbers.

The accelerating adoption of Intuit's AI-driven all-in-one platform, including virtual teams of AI agents and human experts, positions the company to consolidate customers' tech stacks, drive automation of workflows, and unlock substantial ROI for customers, supporting higher average revenue per customer (ARPC) and net margin expansion over time.

Curious what has to happen for that fair value to stack up? The narrative leans on steady revenue compounding, rising profit margins, and a premium earnings multiple that still assumes disciplined execution.

Result: Fair Value of $787.76 (UNDERVALUED)

However, Mailchimp softness and slower online ecosystem customer growth, plus Credit Karma’s exposure to consumer lending cycles, could all challenge those upbeat AI driven assumptions.

Another View: What The Market Multiple Is Saying

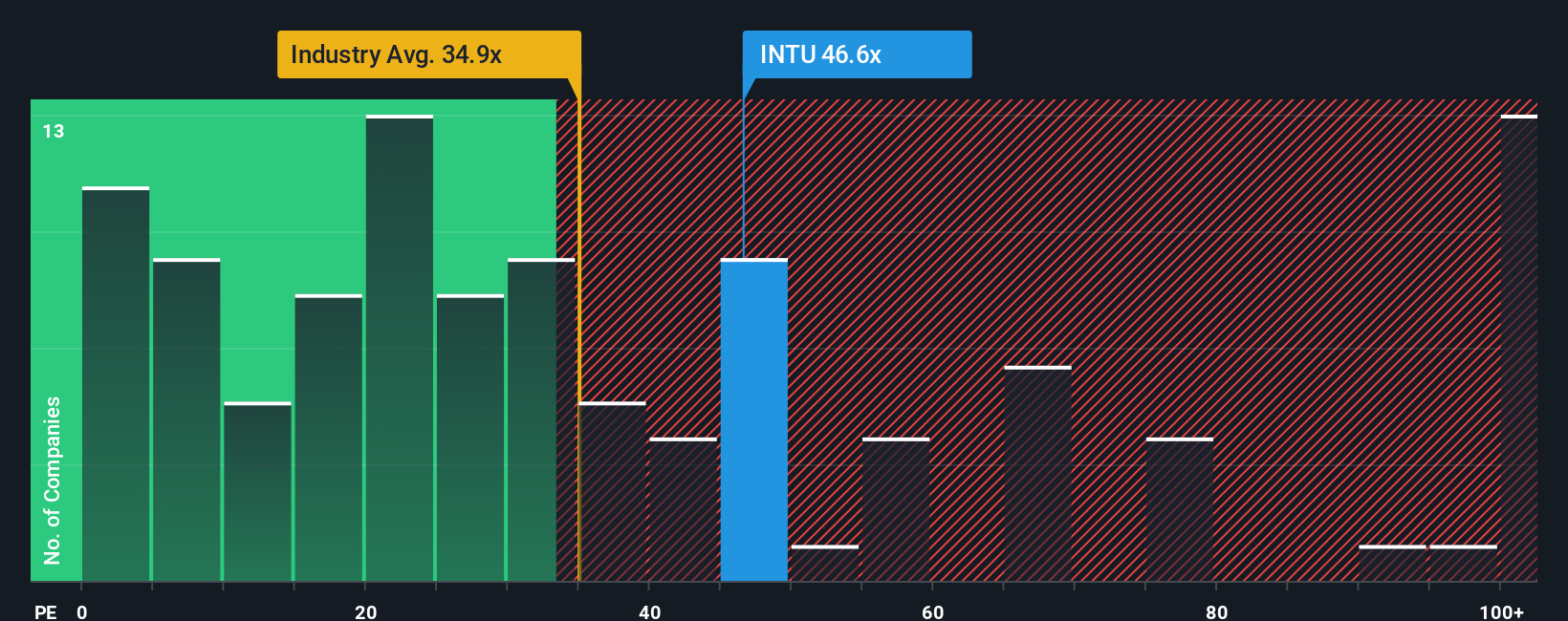

The SWS DCF model suggests Intuit is undervalued, yet the market is still putting a premium price on the stock. At a 29.4x P/E, Intuit trades above the US Software industry average of 25.7x, but below its peer group at 35.6x and the SWS fair ratio of 35.8x. That mix of premium and discount signals both upside potential and valuation risk. Which side of that tradeoff do you think carries more weight?

Build Your Own Intuit Narrative

If you see the data differently or want to stress test your own assumptions, you can build a custom Intuit storyline in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Intuit.

Ready to hunt for your next idea?

If this Intuit reset has you thinking about diversification, use the tools at your fingertips and give yourself more options instead of waiting on one story to play out.

- Spot potential mispricings by scanning our 55 high quality undervalued stocks that pair compressed valuations with solid fundamentals.

- Lock in potential income ideas by checking out 15 dividend fortresses that focus on higher yielding companies.

- Prioritize resilience by reviewing 81 resilient stocks with low risk scores that screen for companies with sturdier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.