Evaluating JetBlue Airways (JBLU) After Its Recent Share Price Weakness

JetBlue Airways Corporation JBLU | 4.57 4.50 | +1.11% -1.45% Pre |

What JetBlue’s Recent Performance Signals for Investors

JetBlue Airways (JBLU) has drawn attention after a 21% decline over the past month, leaving the share price at US$4.51 and prompting fresh questions about how investors view the airline’s risk and recovery profile.

The recent 21% one-month share price decline sits against a softer one-year total shareholder return loss of 15% and a 78% total shareholder return loss over five years. This suggests sentiment has been fading rather than building over time as investors reassess JetBlue’s risks and recovery prospects.

If this kind of volatility has you looking beyond airlines, it could be a good time to scan for infrastructure names benefiting from long-term demand and check out 26 power grid technology and infrastructure stocks

With JetBlue shares at US$4.51, trading close to analyst targets yet sitting on multi year total return losses, investors may need to consider whether the current weakness represents a mispricing or whether the market already reflects expectations for future growth.

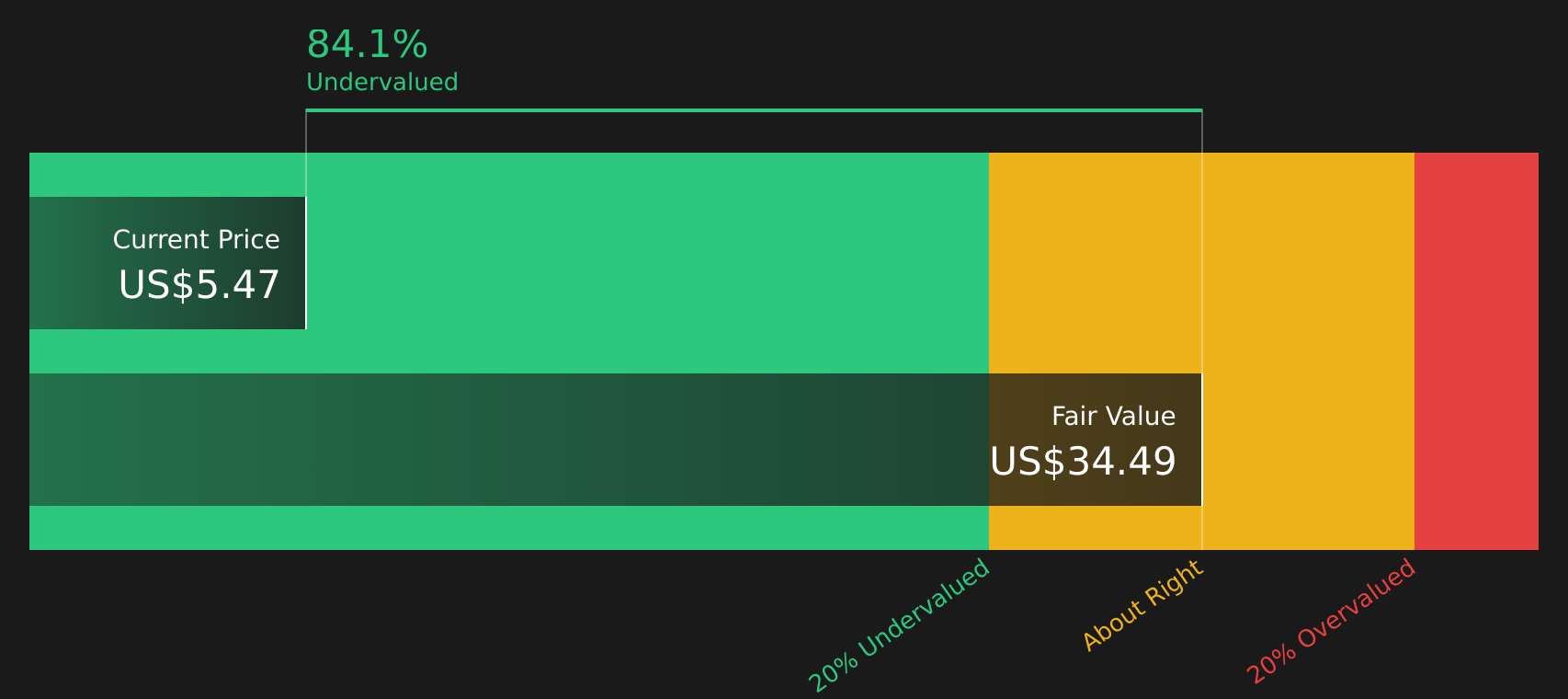

Most Popular Narrative: 8.5% Undervalued

JetBlue’s most followed narrative pegs fair value at about $4.93 per share, slightly above the latest close at $4.51. This frames a modest undervaluation gap.

The rebound in leisure travel and resilient demand, especially among Millennials and Gen Z prioritizing experiences, continues to drive close-in bookings and support premium cabin and loyalty revenue growth, which is likely to result in higher ticket revenues and topline expansion.

Want to see how this leisure heavy story turns into a valuation call? The core thesis leans on specific growth rates, margin repair and future earnings power. The full narrative spells out which numbers need to line up for that fair value to hold.

Result: Fair Value of $4.93 (UNDERVALUED)

However, this story can shift quickly if fuel costs stay elevated or if close in bookings soften. This would pressure margins and test the recovery case.

Another View: Cash Flows Tell a Tougher Story

While the most popular narrative points to an 8.5% gap to fair value at $4.93, the SWS DCF model paints a less generous picture. On that cash flow view, JetBlue’s estimated value is $3.09, below the current $4.51 price, which frames the stock as overvalued instead of undervalued. That kind of disconnect raises a key question: which set of assumptions do you think is closer to reality for JetBlue’s future cash generation and margins?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out JetBlue Airways for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed messages in JetBlue’s story, it makes sense to review the numbers yourself and decide quickly where you stand on the balance of 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If JetBlue’s mixed signals leave you on the fence, broaden your watchlist now. Fresh opportunities rarely wait around for investors who stay focused on one stock.

- Spot potential future standouts early by checking out 31 elite penny stocks with strong financials before attention and capital crowd in.

- Target companies that combine quality with appealing prices using the 61 high quality undervalued stocks, so you are not relying on a single recovery story.

- Prioritize resilience and sleep better at night by focusing on the 69 resilient stocks with low risk scores, especially if recent volatility has tested your confidence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.