Evaluating Markel Group (MKL) After Recent Share Pullback And Fair Value Signals

Markel Group Inc. MKL | 1898.98 | -0.19% |

What Markel Group’s Recent Returns Say About the Stock

Markel Group (MKL) has seen mixed share performance recently, with a 0.6% decline over the past day, a 1.8% pullback over the past week, and a 6.5% drop over the past month.

Even so, the stock shows an 8.9% gain over the past 3 months and a 13.1% total return over the past year, giving investors a blend of shorter term volatility and longer term resilience to assess.

With the share price at $2,047.08, Markel Group’s recent pullback contrasts with a solid 1 year total shareholder return of 13.1%. This hints that short term momentum has cooled after a stronger run in recent years, where the 3 year and 5 year total shareholder returns of 45.7% and 108.5% respectively give longer term holders a very different experience from the latest monthly moves.

If Markel’s recent swings have you thinking about where else capital could work hard, it might be a good moment to check out fast growing stocks with high insider ownership.

With Markel trading near its $2,041.40 analyst price target and screens suggesting roughly a 9.6% premium to some intrinsic estimates, you have to ask: is this a fresh entry point, or is future growth already baked in?

Most Popular Narrative: 0.2% Undervalued

Markel Group’s most followed narrative pegs fair value at about $2,051, almost exactly in line with the recent $2,047.08 share price, yet still a touch higher.

The expansion and success of Markel Ventures, marked by recurring cash flow from non-insurance businesses and recent contributions from new stable-growth units (like EPI and Valor), provide stronger earnings diversification and are expected to reduce volatility in consolidated net income and margins.

Curious how a diversified insurance group lands near this fair value? The narrative leans heavily on measured revenue growth, steady margins, and disciplined capital deployment. Want to see which payout and buyback assumptions really move the model?

Result: Fair Value of $2,051 (ABOUT RIGHT)

However, persistent legacy reserve risks and execution challenges around reorganization and decentralization could quickly undermine the “about right” valuation story if they break the current assumptions.

Another View On Markel’s Valuation

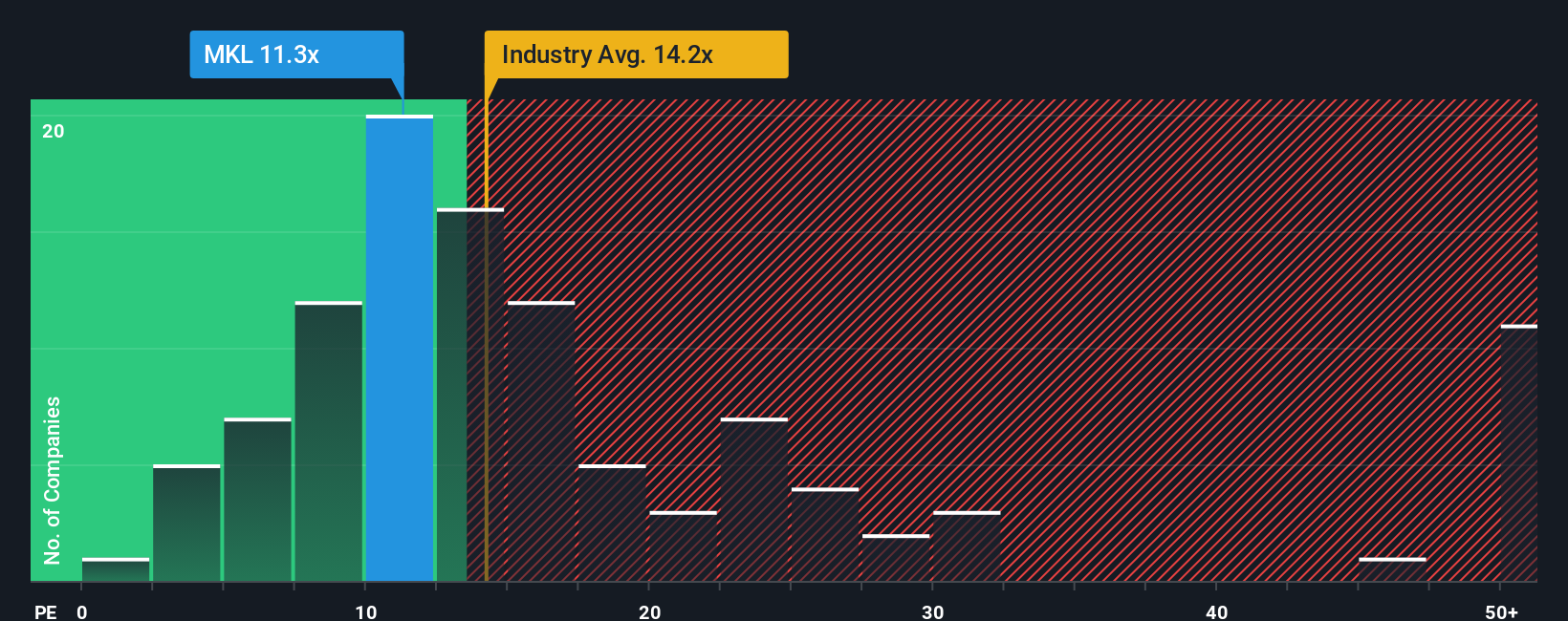

The narrative-based fair value of about $2,051 suggests Markel is roughly in line with its modeled worth, but the earnings multiple tells a different story. At a P/E of 14.2x versus a fair ratio of 12.8x, Markel screens as expensive, with industry and peer averages around 12.7x to 12.5x. If sentiment cools, that gap could potentially close through changes in the price rather than the ratio.

Build Your Own Markel Group Narrative

If you look at this and think the assumptions miss something or simply want to test your own view, you can build a custom Markel story in just a few minutes, starting with Do it your way.

A great starting point for your Markel Group research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Ready To Hunt For More Investment Ideas?

If Markel has sharpened your thinking, do not stop here. Put that momentum to work and scan for fresh ideas that match your style.

- Target reliable income by reviewing these 12 dividend stocks with yields > 3% that might help you build a steadier cash flow stream from your portfolio.

- Spot potential growth stories early by checking out these 24 AI penny stocks that tap into rising demand for artificial intelligence.

- Position yourself for long term gains by investigating these 880 undervalued stocks based on cash flows that currently trade below their estimated cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.