Evaluating Quest Diagnostics (DGX) After Dividend Hike Strong Earnings Guidance And Expanded Buyback

Quest Diagnostics Incorporated DGX | 191.42 191.42 | -1.41% 0.00% Pre |

Quest Diagnostics (DGX) is back in focus after a busy February 10 update, combining higher quarterly and full year 2025 earnings, fresh 2026 guidance, a 7.5% dividend increase, and a larger share repurchase authorization.

Those earnings, acquisition plans, dividend lift and larger buyback sit against a share price of $206.87, with a 7 day share price return of 8.2% and a 90 day share price return of 11.6%, while the 5 year total shareholder return of 96.4% points to momentum that has rewarded patient holders.

If this update has you thinking about what else is moving in healthcare and diagnostics, it could be worth scanning our list of 25 healthcare AI stocks as a next step.

With Quest now trading at $206.87, an intrinsic discount flag of 32% and a modest gap to the average analyst target, you have to ask whether the market is overlooking value here or already factoring in the next leg of growth.

Most Popular Narrative: 4% Overvalued

Quest Diagnostics closed at $206.87 against a widely followed fair value view of about $199 per share, which frames today’s rally in a different light.

Strategic execution on accretive acquisitions, including the large LifeLabs deal, and expanded health system partnerships (e.g., with Fresenius) are boosting patient volumes, expanding geographic reach, and producing procurement and operational synergies that are expected to materially lift revenue and earnings.

Curious how much earnings growth and margin expansion this narrative is baking in, and what kind of future P/E multiple that requires? The full story links those moving pieces into one valuation case.

Result: Fair Value of $199 (OVERVALUED)

However, you still need to weigh risks such as potential reimbursement cuts under PAMA, as well as pressure on pricing and margins as competition and payer consolidation build.

Another Take: Multiples Paint A Different Picture

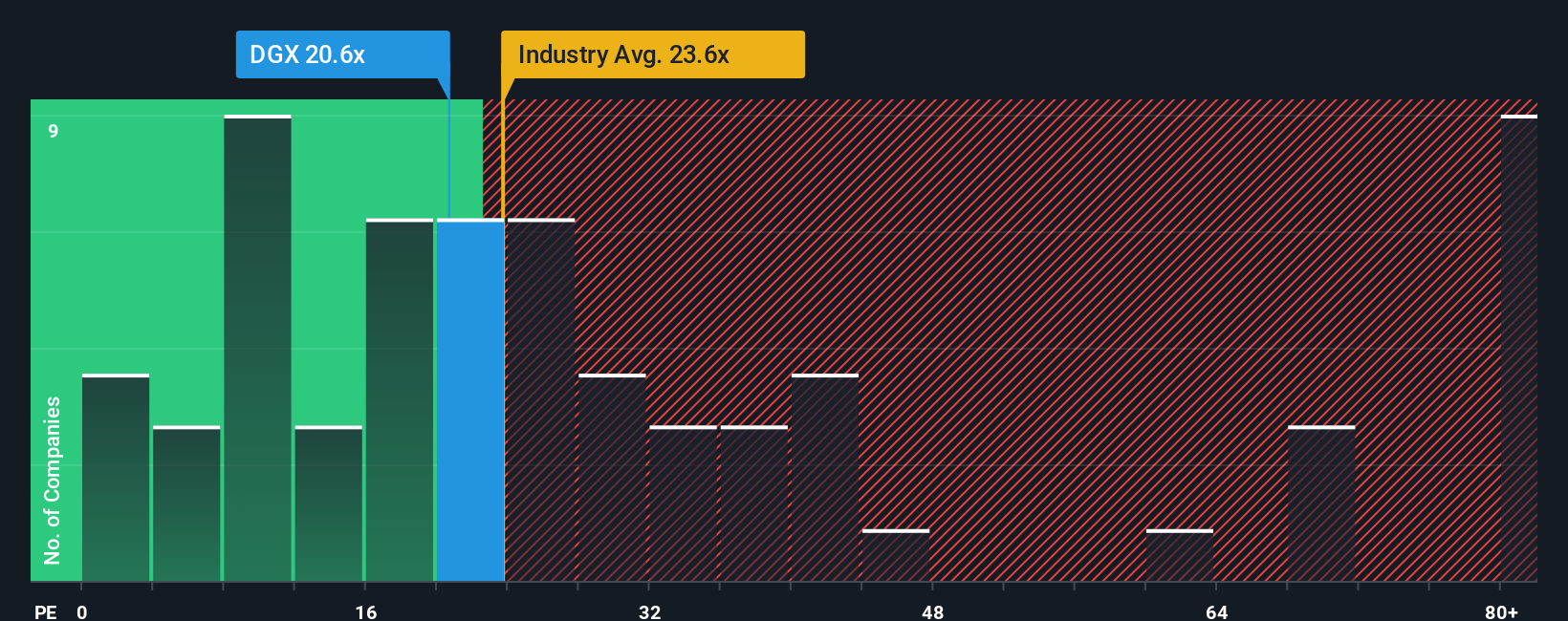

While the narrative based fair value pins Quest Diagnostics at about $199 and labels the stock overvalued, its current P/E of 23x sits below peers at 34.5x and below its own fair ratio of 28x. That gap suggests the market is pricing in more risk, or leaving something on the table depending on how you see the story playing out.

Build Your Own Quest Diagnostics Narrative

If you look at the numbers and reach a different conclusion, or simply prefer your own process, you can build a custom thesis in just a few minutes by starting with Do it your way.

A great starting point for your Quest Diagnostics research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Quest has sharpened your focus, do not stop here. Widen your watchlist now so you are not catching up on opportunities later.

- Target long term compounding potential by scanning our list of 54 high quality undervalued stocks that combine solid fundamentals with room for the market to reassess their pricing.

- Strengthen your income stream by reviewing 13 dividend fortresses that aim to pair higher yields with business models that can support regular payouts.

- Prioritise peace of mind by checking our 83 resilient stocks with low risk scores which highlight companies with more resilient risk profiles than many broad market names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.