Evaluating Restaurant Brands International Stock After Recent 8.5% Jump in the Past Month

Restaurant Brands International, Inc. QSR | 0.00 |

Thinking about what to do with your Restaurant Brands International shares? You are not alone. Anyone eyeing this fast food giant's stock has reason to be curious right now. Over the past week, shares have climbed 3.0% and are up an impressive 8.5% in just the last month. Year-to-date, the return sits at 5.7%. Yet, when looking over a longer horizon, you will notice a more modest gain of 45.9% over five years, but a flat performance in the past year. These numbers reflect a market that is weighing optimism against lingering uncertainties, pointing to a shift in how investors are evaluating risk and growth potential in the restaurant sector.

Other than broader shifts in consumer habits and ongoing conversations about international expansion, there have not been any major headlines driving recent momentum. This suggests the move could be less about news and more about changing sentiment around the company’s outlook, perhaps hinting that investors are starting to reevaluate its long-term value potential.

Now, when it comes to valuation, the stock earns a value score of 2 out of 6. This means it is currently undervalued in two of the six key valuation checks we will examine. That might not suggest a “deep bargain,” but it does indicate there are pockets of opportunity if you know where to look.

Let us dig into the numbers and see what each of those valuation methods actually tells us about whether Restaurant Brands International is a buy right now. And, stay tuned to the end for a smarter way to get the most useful picture of the company’s true value.

Restaurant Brands International scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

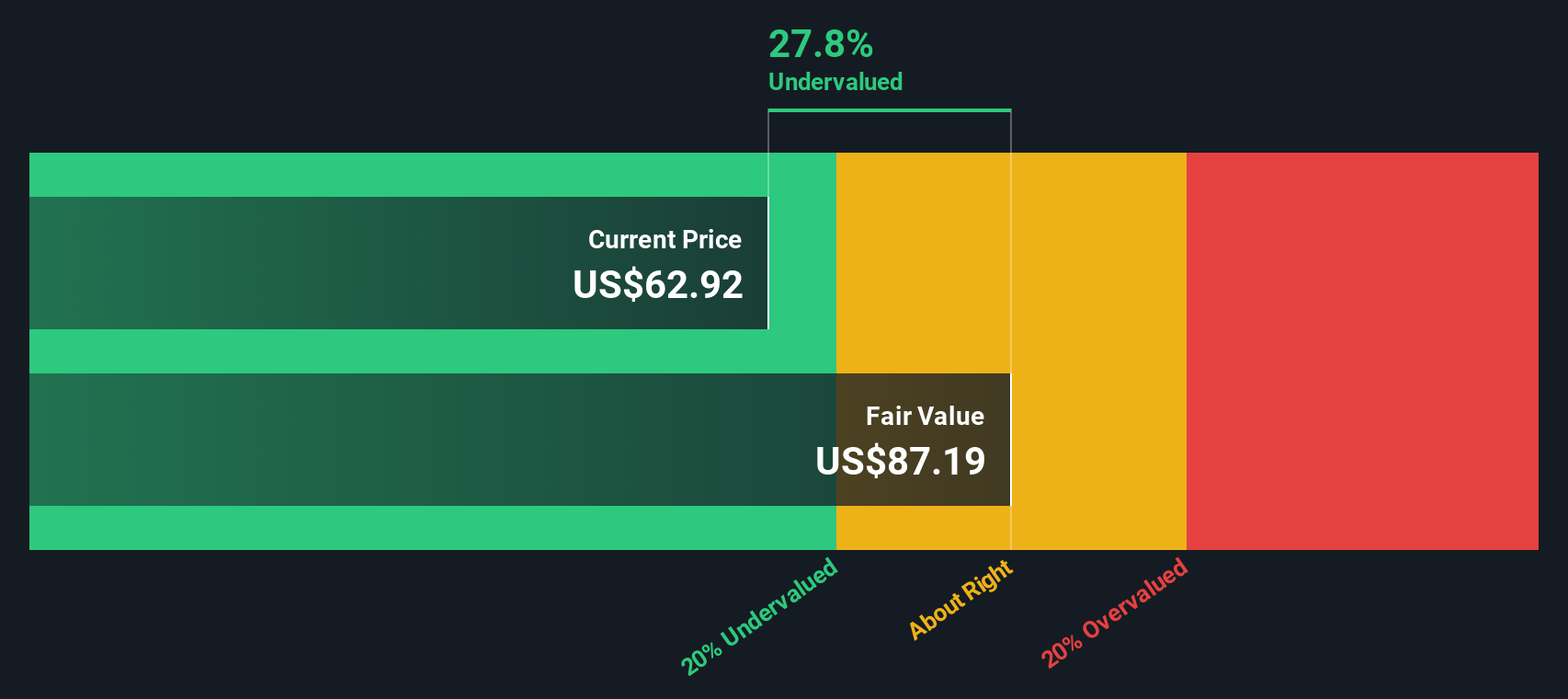

Approach 1: Restaurant Brands International Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to their present value. Essentially, it tries to answer: how much are all of Restaurant Brands International’s future projected cash profits worth today, given the risks and time value of money?

For Restaurant Brands International, analysts estimate the most recent Free Cash Flow at $1.26 Billion. Over the coming years, projections point to consistent growth, with free cash flow expected to reach $2.39 Billion by 2028. Longer-term estimates, extrapolated beyond analyst forecasts, support this rising trend and indicate the company's ability to keep generating increasing levels of cash in the years ahead.

When all these future cash flows are discounted back, the DCF model calculates an intrinsic value of $81.76 per share. With the current share price implying a 15.2% discount to this fair value estimate, the stock presently appears undervalued based on its projected cash-generating strength.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Restaurant Brands International is undervalued by 15.2%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

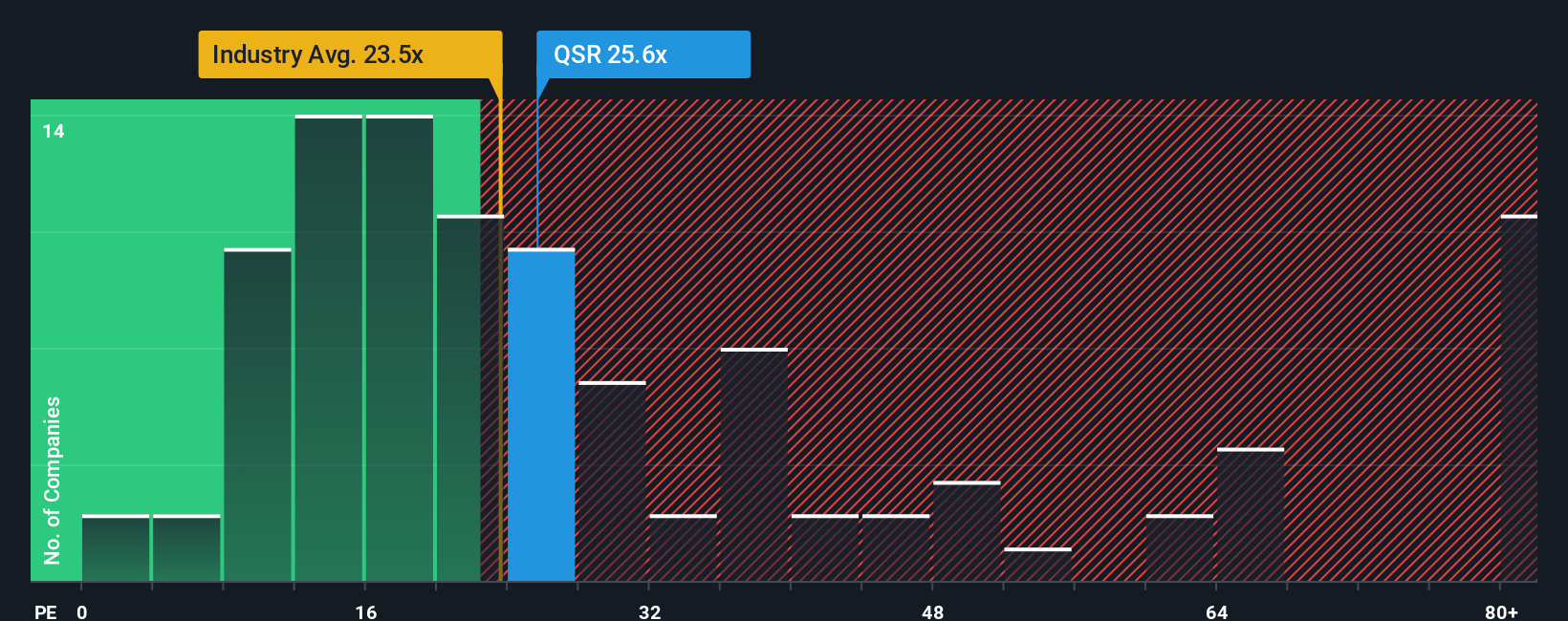

Approach 2: Restaurant Brands International Price vs Earnings

The Price-to-Earnings (PE) ratio is a popular valuation tool for profitable companies like Restaurant Brands International because it directly connects a company’s market price to its earnings power. Investors use the PE ratio to gauge how much they are paying for each dollar of current profit, making it an intuitive benchmark for established, earnings-generating businesses.

It is important to note that the fair value for any PE ratio is influenced by growth prospects and perceived risks. Fast-growing firms often trade at higher PE multiples as investors expect future profits to increase. In contrast, higher risk or flat growth puts pressure on the valuation. For context, Restaurant Brands International currently trades at a PE ratio of 26x. This is a touch above both the Hospitality industry average of 23x and the peer group average of 25x, suggesting the market has marginally higher expectations for its performance or lower perceived risk compared to its peers.

Simply Wall St’s proprietary “Fair Ratio” offers a more comprehensive way to evaluate this number. Unlike traditional comparisons that only look at peer or industry averages, the Fair Ratio factors in a wider set of considerations, including the company’s projected earnings growth, profit margins, size, and industry-related risks. For Restaurant Brands International, the Fair Ratio stands at 31.5x. Because the company’s current PE of 26x is notably below this figure, the stock looks undervalued by this metric. This may indicate possible upside if the company delivers on earnings growth as expected.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Restaurant Brands International Narrative

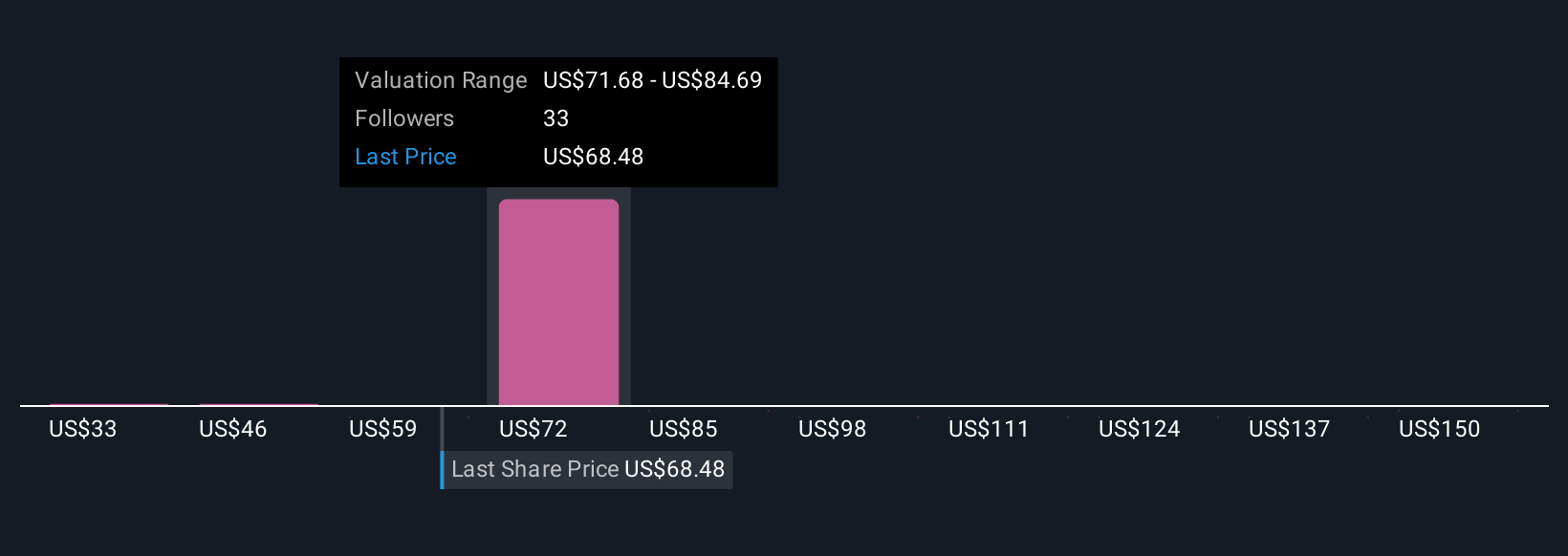

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is more than just a number. It is your personal story and perspective about a company’s future, combined with your own estimates for future revenue, earnings, and margins. Narratives connect what is happening in the real world to a set of forward-looking forecasts and, ultimately, to your fair value calculation.

With Simply Wall St’s Narratives feature, available for free on the Community page and already used by millions of investors, you can easily create, update, and compare your own view of Restaurant Brands International to others. Narratives help you decide when to buy or sell by directly comparing your fair value to the current share price. This evaluation updates whenever there is important news or earnings results that could impact the underlying story.

For example, one Restaurant Brands International Narrative might estimate fast revenue growth and rising profit margins thanks to international franchising and digital innovation, supporting a higher fair value of $93.0 per share. Another might focus on margin risks and fierce competition, resulting in a more cautious view and a fair value closer to $60.0 per share.

Do you think there's more to the story for Restaurant Brands International? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.