Evaluating Seadrill (SDRL) After Recent Share Price Momentum And Rich Earnings Multiple

Seadrill Limited SDRL | 45.63 | +2.40% |

Why Seadrill (SDRL) is back on investors’ radar

Seadrill (SDRL) has drawn fresh attention after recent trading, with the share price closing at $38.04 and showing mixed near term returns alongside a positive move over the past 3 months.

While the 1 day share price return of 4% and 7 day share price return of 1.6% have softened, Seadrill’s 90 day share price return of 33.5% and 1 year total shareholder return of 9.5% point to momentum that has lately cooled rather than reversed.

If Seadrill’s recent move has you reassessing the energy space, it could be worth broadening your watchlist with our screener of 22 power grid technology and infrastructure stocks.

With Seadrill trading at $38.04, sitting below an average analyst price target of $43.71 and screening with a low value score of 2, investors may ask whether this represents a genuine opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 12.6% Undervalued

Seadrill’s most followed narrative points to a fair value of $43.50, a touch above the $38.04 last close, and anchors that view in a specific offshore cycle story.

Supply of competitive ultra-deepwater rigs remains tight due to minimal newbuilds and uneconomical reactivations, positioning Seadrill's high-spec fleet for greater pricing power and margin improvement as the market rebalances and ultimately benefiting net margins and profitability.

Want to see why this narrative sees more value ahead? It leans heavily on one key idea, stronger earnings power built on disciplined capacity and richer contracts. Curious which revenue and margin assumptions have been baked in, and how they stack up against today’s profitability? The full story connects those moving parts to that $43.50 figure.

Result: Fair Value of $43.50 (UNDERVALUED)

However, softer utilization and contract delays, together with legal and regulatory disputes that can trigger unexpected cash outflows, could quickly challenge this earnings and margin story.

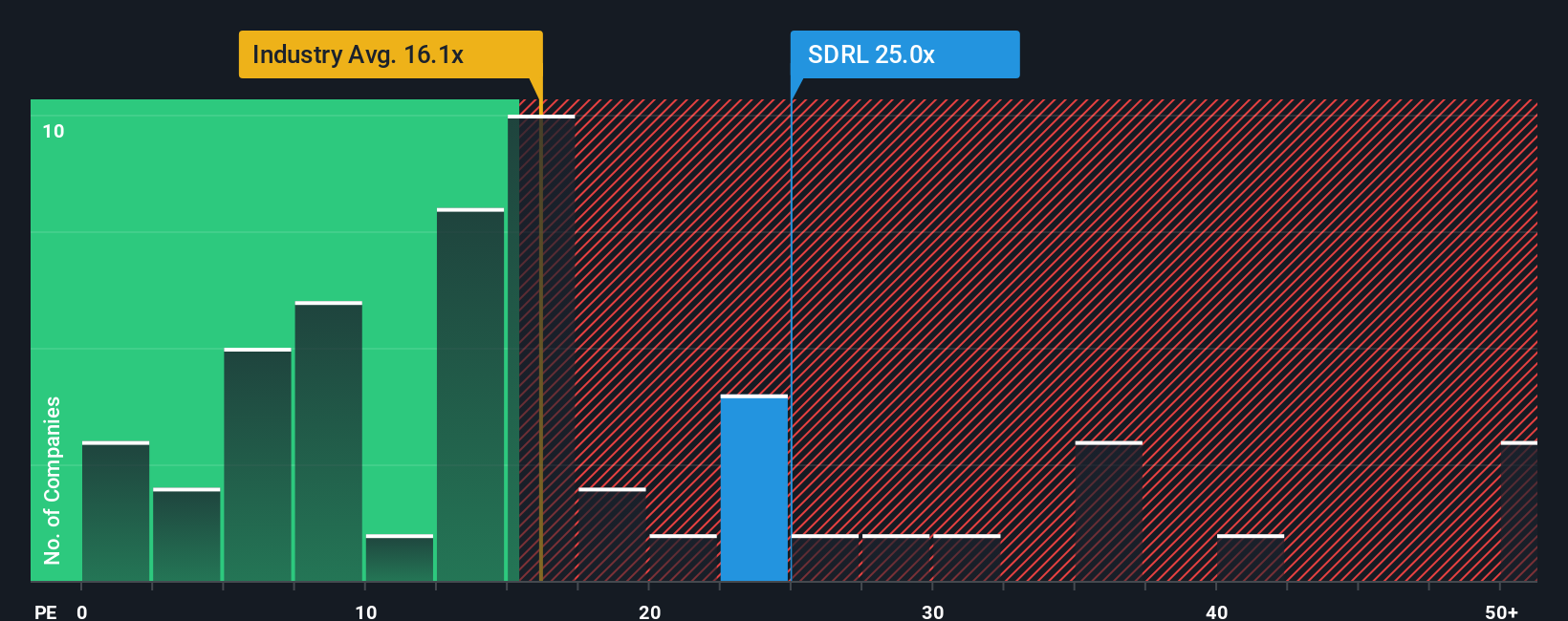

Another way to look at Seadrill’s value

There is a clear tension between the narrative fair value of $43.50 and what the earnings multiple is saying. At $38.04, Seadrill trades on a P/E of 69.8x, compared with 23.4x for the US Energy Services industry and a 15.6x peer average, while the fair ratio sits lower at 49.7x.

Those gaps point to a lot of optimism already embedded in the price, which can mean more valuation risk if earnings do not track forecasts. The question for you is whether Seadrill’s future earnings path truly supports such a rich multiple, or if expectations have run ahead of reality.

Build Your Own Seadrill Narrative

If the story so far does not quite match your view, or you prefer to test the assumptions yourself, use the tools to build your own narrative and see how your thesis stacks up in just a few minutes, Do it your way.

A great starting point for your Seadrill research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Seadrill has you thinking more broadly about your portfolio, do not stop here. Use the tools at your fingertips to keep finding ideas that fit you.

- Target quality at a discount by reviewing companies our screener flags as 55 high quality undervalued stocks with solid fundamentals and room for a better market view.

- Strengthen your income stream by checking out businesses in our list of 15 dividend fortresses that focus on returning cash to shareholders.

- Dial down portfolio stress by scanning our 81 resilient stocks with low risk scores that highlight companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.