Evaluating SentinelOne (S) Valuation After Insider Buying And AI Platform Updates

SentinelOne, Inc. Class A S | 13.33 | +0.15% |

SentinelOne (S) is back in focus after fresh insider buying by a company director. This coincided with new AI-driven Singularity platform upgrades, renewed partnership buzz, and acquisition activity in the AI security space.

Even with fresh insider buying and AI security headlines in play, momentum has been mixed, with a 1-day share price return of 3.65% sitting against a 30-day share price return of 8.04% and a 1-year total shareholder return decline of 43.49%, suggesting enthusiasm is rebuilding from a weaker longer term base.

If SentinelOne’s AI push has caught your attention, it could be a good moment to see what else is happening across high growth tech and AI stocks and compare different ways the market is pricing growth stories.

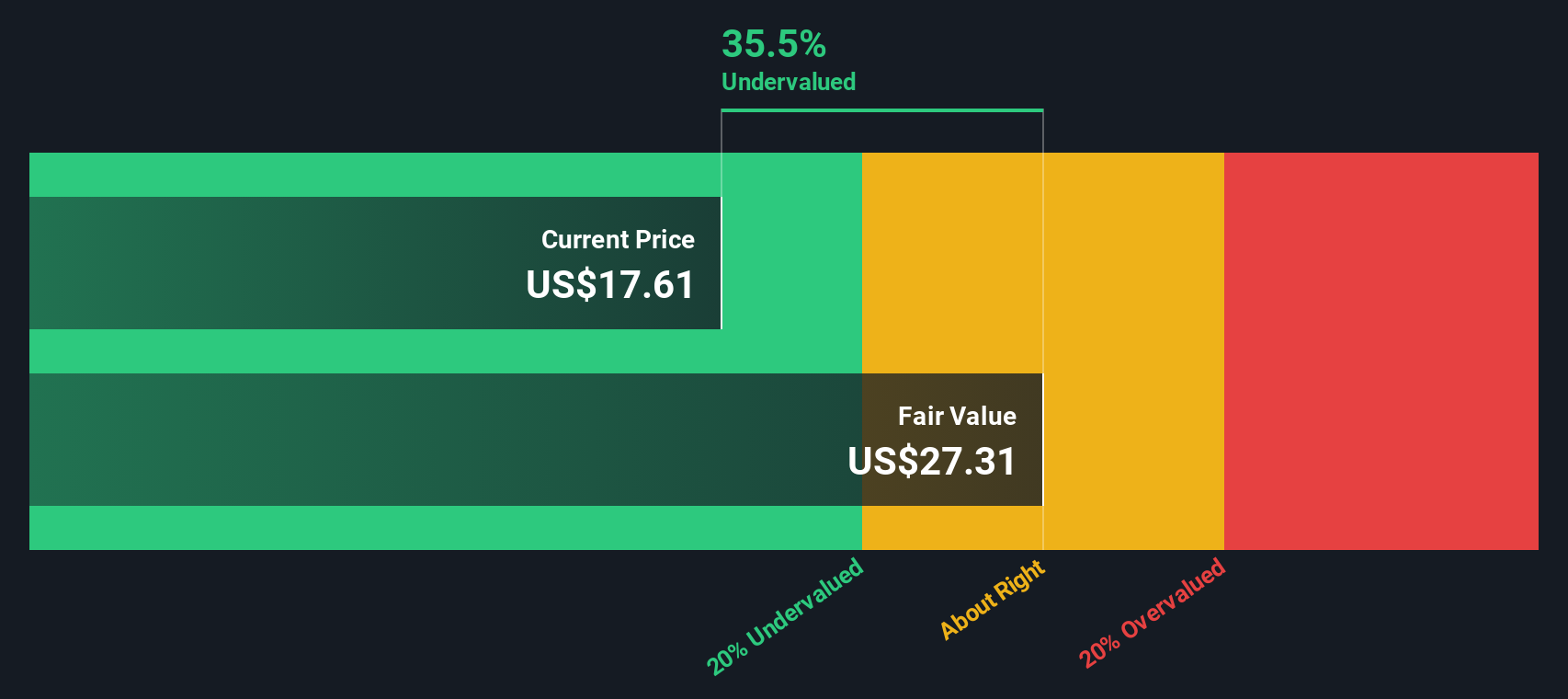

With shares around $13.62, a value score of 4, an estimated intrinsic discount of 41.81% and a 43.49% 1 year total return decline, is SentinelOne a mispriced AI security player, or is the market already baking in future growth?

Most Popular Narrative: 35.6% Undervalued

Against SentinelOne’s last close of $13.62, the most followed narrative pins fair value at about $21.15, framing the current share price as a sizeable discount.

The new SentinelOne Flex licensing model is accelerating multi-product adoption, leading to larger deal sizes, increased platform retention, and rising recurring revenue, all of which support both near-term and long-term net margin expansion through reduced sales friction and deeper customer integration.

Want the full story on why this valuation leans higher? The narrative leans on sustained double digit revenue growth, margin uplift, and a punchy earnings multiple. Curious which assumptions really carry the weight? Read on to see what the numbers are pointing to.

Result: Fair Value of $21.15 (UNDERVALUED)

However, there are still watchpoints, including reliance on large partners and the risk that acquisitions and new AI products weigh on margins before they add meaningful revenue.

Another View: Market Pricing Signals A Tighter Gap

Our DCF model puts fair value closer to $23.41, which also points to SentinelOne trading below estimated worth, although by a smaller margin than the $21.15 narrative. If both methods say undervalued but to different degrees, which set of assumptions feels more realistic to you?

Build Your Own SentinelOne Narrative

If you are not convinced by these views or prefer to test your own assumptions, you can build a complete SentinelOne thesis yourself in just a few minutes, starting with Do it your way.

A great starting point for your SentinelOne research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If SentinelOne has sparked your interest, do not stop there. The screener can surface other ideas that fit your style before the crowd catches on.

- Spot potential turnaround stories by checking out these 3536 penny stocks with strong financials that combine smaller share prices with underlying financials that may be stronger than you expect.

- Explore AI-focused opportunities through these 29 AI penny stocks where themes in automation and machine learning are reflected in real businesses.

- Focus on value by filtering for these 859 undervalued stocks based on cash flows and compare how pricing lines up against cash flow based assessments across different sectors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.