Even With A 29% Surge, Cautious Investors Are Not Rewarding The Mediterranean and Gulf Cooperative Insurance and Reinsurance Company's (TADAWUL:8030) Performance Completely

MEDGULF 8030.SA | 14.30 | +0.56% |

The Mediterranean and Gulf Cooperative Insurance and Reinsurance Company (TADAWUL:8030) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 42% over that time.

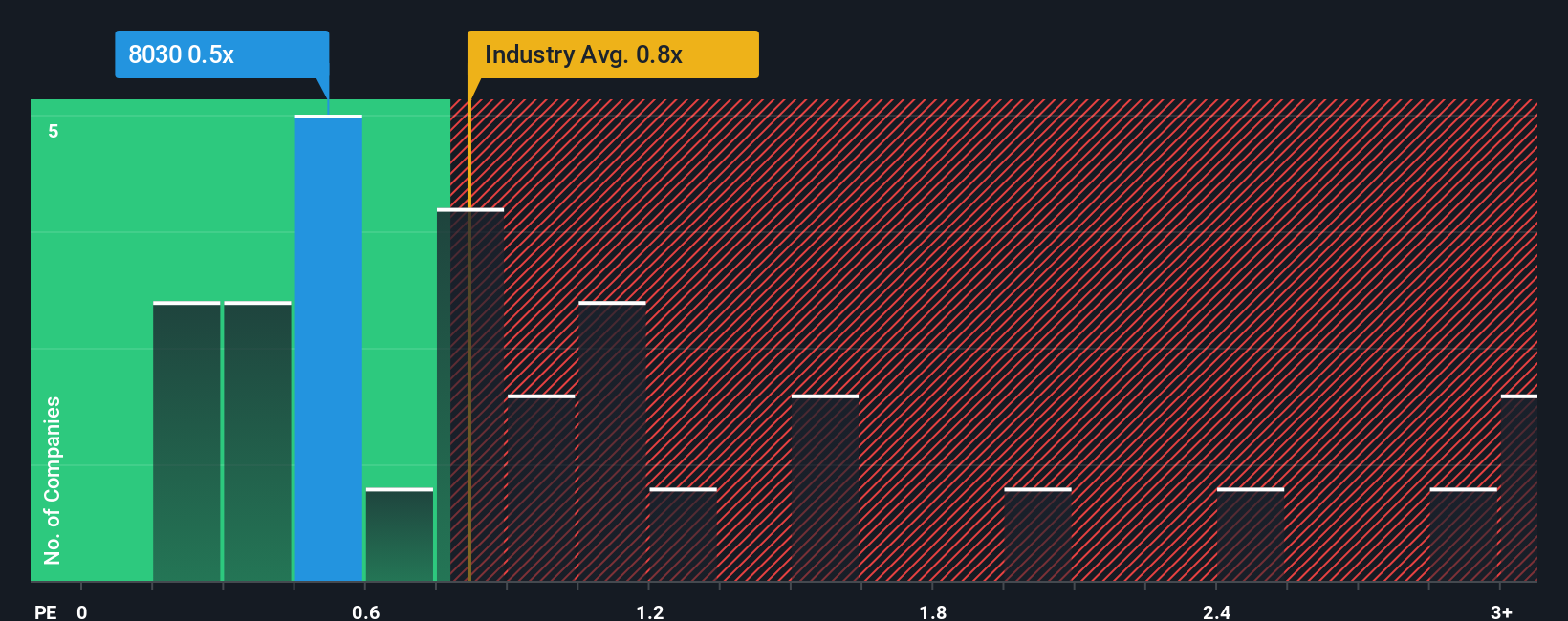

Although its price has surged higher, there still wouldn't be many who think Mediterranean and Gulf Cooperative Insurance and Reinsurance's price-to-sales (or "P/S") ratio of 0.5x is worth a mention when the median P/S in Saudi Arabia's Insurance industry is similar at about 0.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

What Does Mediterranean and Gulf Cooperative Insurance and Reinsurance's Recent Performance Look Like?

Revenue has risen firmly for Mediterranean and Gulf Cooperative Insurance and Reinsurance recently, which is pleasing to see. It might be that many expect the respectable revenue performance to wane, which has kept the P/S from rising. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Mediterranean and Gulf Cooperative Insurance and Reinsurance's earnings, revenue and cash flow.How Is Mediterranean and Gulf Cooperative Insurance and Reinsurance's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Mediterranean and Gulf Cooperative Insurance and Reinsurance's is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company managed to grow revenues by a handy 15% last year. The latest three year period has also seen an excellent 74% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing that to the industry, which is only predicted to deliver 4.3% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised revenue results.

With this information, we find it interesting that Mediterranean and Gulf Cooperative Insurance and Reinsurance is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Bottom Line On Mediterranean and Gulf Cooperative Insurance and Reinsurance's P/S

Mediterranean and Gulf Cooperative Insurance and Reinsurance appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Mediterranean and Gulf Cooperative Insurance and Reinsurance currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.