Event Reminder | Get Ready for 04:15 PM Today (Wed., Nov. 5th)

Target Hospitality Corp. TH | 9.28 11.52 | +0.32% +24.14% Pre |

Amazon.com, Inc. AMZN | 208.27 210.67 | +3.64% +1.15% Pre |

Paramount Global Ordinary Shares - Class A PARAA | 16.91 16.91 | Delist 0.00% Pre |

S&P 500 index SPX | 6528.52 | +2.91% |

NASDAQ IXIC | 21590.63 | +3.83% |

01

Event Report:

ADP In Spotlight Amid Gov't Shutdown

The US labor market faces an unprecedented data vacuum as the federal government shutdown extends into its second month, halting all official economic releases from the Bureau of Labor Statistics (BLS).

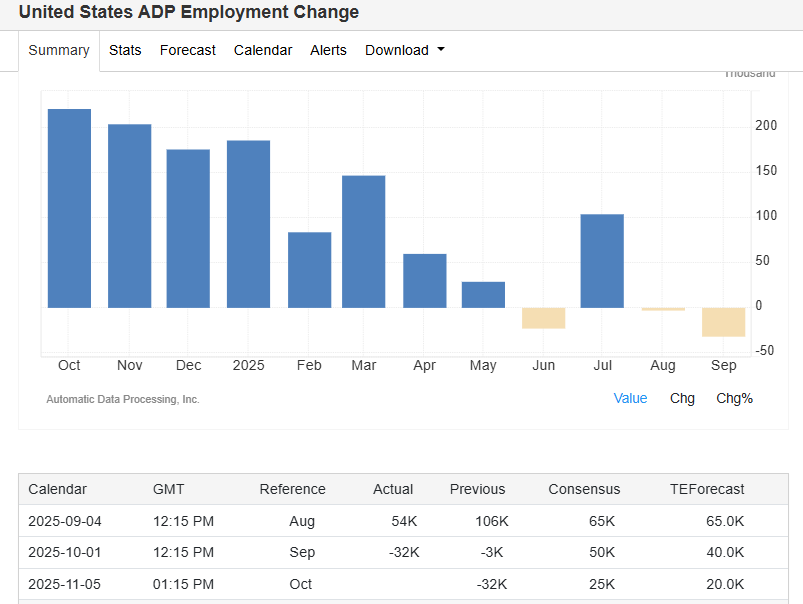

In this void, the October ADP National Employment Report, scheduled for Wednesday, November 5, gains critical significance as the sole high-frequency indicator of US employment trends.

Also will be unveiled on the same day are the gauges including the following:

| Event | Riyadh Time | Malaysia Time | Importance | Previous | Forecast |

|---|---|---|---|---|---|

| ADP Employment Change | 16:15 | 21:15 | ★★☆ | -32K | 20.0K |

| Treasury Refunding Announcement | 16:30 | 21:30 | ★☆☆ | N/A | N/A |

| S&P Global Composite PMI Final | 17:45 | 22:45 | ★☆☆ | 53.9 | 54.8 |

| S&P Global Services PMI Final | 17:45 | 22:45 | ★☆☆ | 54.2 | 55.2 |

| ISM Services PMI | 18:00 | 23:00 | ★★★ | 50.0 | 50.8 |

| ISM Services Business Activity | 18:00 | 23:00 | ★☆☆ | 49.9 | 50.2 |

| ISM Services Employment | 18:00 | 23:00 | ★☆☆ | 47.2 | 47.5 |

| ISM Services New Orders | 18:00 | 23:00 | ★☆☆ | 50.4 | 50.7 |

| ISM Services Prices | 18:00 | 23:00 | ★☆☆ | 69.4 | 69 |

| EIA Crude Oil Stocks Change | 18:30 | 23:30 | ★★☆ | -6.858M | N/A |

| EIA Gasoline Stocks Change | 18:30 | 23:30 | ★★☆ | -5.941M | N/A |

| EIA Crude Oil Imports Change | 18:30 | 23:30 | ★☆☆ | -1.025M | N/A |

The report will provide the first glimpse into whether September’s alarming job loss of 32,000 private sector positions—the sharpest decline since March 2023—persisted into October.

The shutdown has forced investors and policymakers to rely on fragmented private data. ADP’s survey, derived from over 25 million anonymized payroll records, now serves as a proxy for the delayed Nonfarm Payrolls report. US Labor Secretary Lori Chavez-DeRemer has confirmed that BLS data will remain suspended until the government reopens, amplifying the weight of ADP’s release.

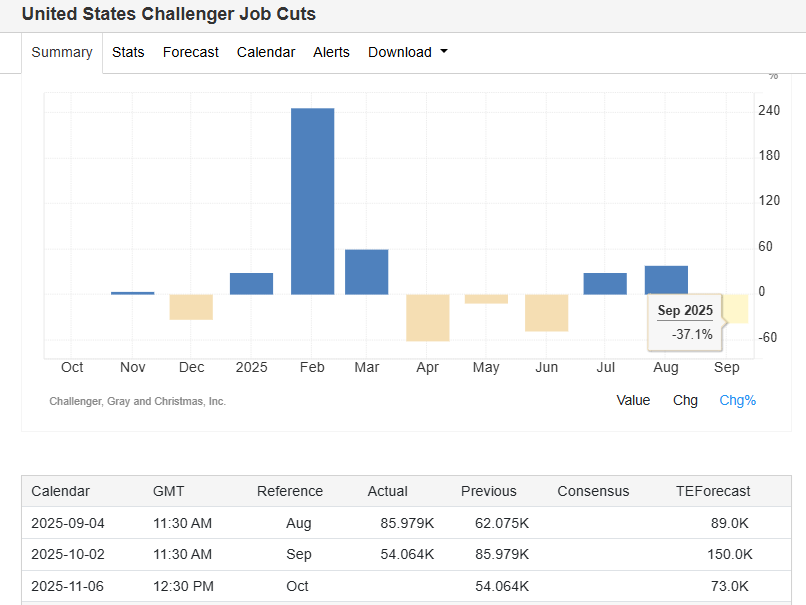

Concurrently, alternative metrics from Indeed and Challenger highlight a 37% drop in job postings since March 2022 and nearly 950,000 layoffs year-to-date—the highest since 2020—signaling underlying labor fragility.

02

Expectations, Interpretation:

Narrow Path for Fed Policy

Consensus Forecasts and Key Themes

Economists expect a modest rebound in October ADP employment, projecting an increase of 27,000 jobs, a partial recovery from September’s contraction of 32,000.

This optimism hinges on resilient service-sector hiring and seasonal demand, but risks are skewed downward due to:

- Broadening layoffs: Companies like Target Corporation(TGT.US), Amazon.com, Inc.(AMZN.US), and Paramount Global Ordinary Shares - Class A(PARAA.US) have cut thousands of roles, with the tech, retail, and government sectors leading losses.

- Cooling wage growth: ADP’s wage growth metrics have slowed to 4.5% year-over-year, aligning with weaker labor demand.

- PMI divergences: While services activity remains expansionary (ISM Services Index at 50.7), manufacturing continues to contract, pressuring goods-producing jobs.

How Will the Fed Interpret the Data?

The ADP report will directly influence the Federal Reserve’s December rate decision, but officials remain divided amid data scarcity and persistent inflation:

- Dovish signals:

A weak ADP print (e.g., near zero or negative) would validate concerns about labor deterioration, supporting calls for another 25-basis-point cut. Chicago Fed President Austan Goolsbee has emphasized balancing inflation fears with employment risks, noting unemployment remains stable at 4.3% but warning of "clearer weakening".- Hawkish constraints:

Fed officials, including Goolsbee and Governor Lisa Cook, stress that inflation—still at 3% year-over-year—exceeds the 2% target, making premature easing risky. The Fed’s October meeting minutes revealed internal dissent, with Stephen Milan advocating for a 50-basis-point cut while Jeffrey Schmid opposed any easing.- Market pricing:

Futures imply a 63% probability of a December cut, down from 95% a week ago, reflecting uncertainty. A subdued ADP report could push odds toward 70–80%, while a strong reading may quash hopes of near-term easing.

Baseline interpretation: ADP data aligning with expectations (~27,000) will be framed as "stable but fragile," affirming a gradual cooling without crisis. However, a second consecutive negative reading would intensify recession fears and pressure the Fed to prioritize labor market support.

03

Market Impact:

Equities Amid Policy Ambiguity, Earnings Volatility

Short-Term Reaction Scenarios

The ADP report arrives amid a packed earnings week (e.g., Palantir(PLTR.US), Advanced Micro Devices, Inc.(AMD.US)) and simmering trade tensions, leaving equities sensitive to labor surprises:

- ADP above expectations (≥40,000):

Likely triggers a 0.5–1.0% decline in the S&P 500 as traders price out December rate cuts. Cyclical sectors (e.g., financials, industrials) would underperform, while tech stocks face pressure from higher discount rates.- ADP in line (20,000–30,000):

A neutral outcome, allowing markets to focus on corporate earnings. The Nasdaq may extend gains fueled by AI-driven optimism (e.g., Amazon’s recent rally), but volatility will linger ahead of Friday’s Michigan consumer sentiment data.- ADP below expectations (≤10,000 or negative):

Could spark a 1.0–2.0% rally by reinforcing dovish Fed bets. Defensive sectors (utilities, consumer staples) and rate-sensitive tech stocks would lead gains, though prolonged weakness may revive fears of a profit slump.

Broader Market Sentiment and Vulnerabilities

Investor positioning reflects two competing narratives:

- Soft-landing optimism: Strong Q3 earnings (Nasdaq up 2.5% last week) and resilient consumer spending support hopes for a gentle slowdown. A "Goldilocks" ADP print (20,000–40,000) would sustain this view.

- Policy uncertainty: The Fed’s data-dependent stance and internal divisions amplify volatility. Citi warns that rising continuing jobless claims (above 1.8 million) could signal deeper cracks, threatening the rally’s sustainability.

Key risks: High equity valuations (S&P 500 P/E ≈22x) and sector concentration leave markets exposed to ADP-driven swings. If the report hints at accelerating layoffs—particularly in transportation or retail—it could trigger a broader de-risking, as noted by Indeed’s Cory Stahle: "That’s where you really start to worry".