Exploring 3 Undervalued Small Caps With Insider Action From Various Regions

Over the last 7 days, the United States market has experienced a 1.8% drop, yet it has shown resilience with a 23% rise over the past year and an anticipated annual earnings growth of 19%. In this dynamic environment, identifying promising small-cap stocks with recent insider activity can be key to uncovering potential opportunities for investors seeking value.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Ferroglobe | NA | 0.5x | 31.11% | ★★★★★☆ |

| Appian | 1737.8x | 2.0x | 39.26% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.2x | 38.24% | ★★★★★☆ |

| First Bancorp | 10.3x | 3.9x | 21.42% | ★★★★☆☆ |

| Bank of the James Financial Group | 10.1x | 2.2x | 20.62% | ★★★★☆☆ |

| Peoples Bancorp | 11.9x | 3.1x | 42.77% | ★★★★☆☆ |

| German American Bancorp | 12.6x | 4.6x | 42.22% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 34.31% | ★★★☆☆☆ |

| NameSilo Technologies | 428.0x | 2.0x | 40.72% | ★★★☆☆☆ |

| National Vision Holdings | 29.2x | 0.7x | 38.08% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

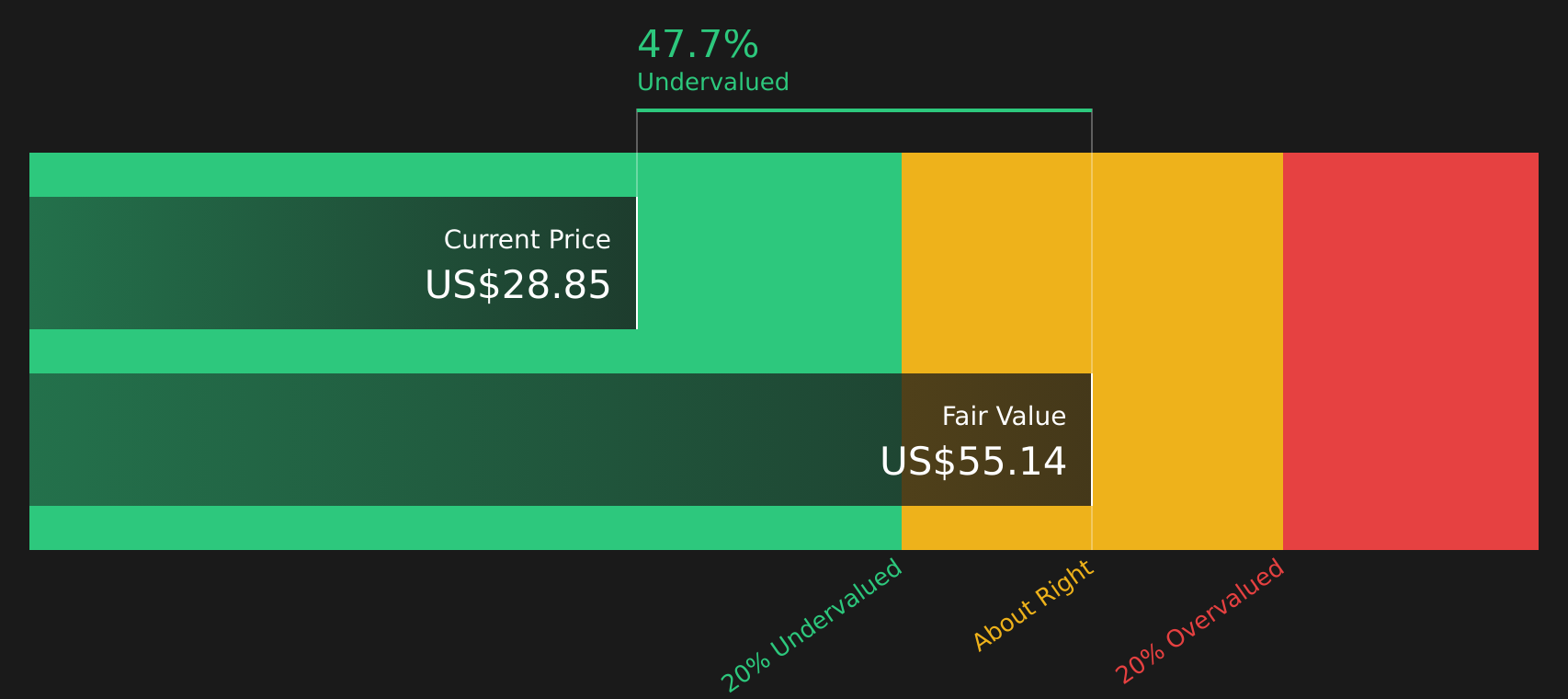

Commercial Bancgroup (CBK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Commercial Bancgroup operates primarily in the banking sector with a focus on providing financial services, and it has a market capitalization of $1.25 billion.

Operations: CBK generates revenue primarily from its banking segment, with recent figures showing $91.06 million. The company has consistently achieved a gross profit margin of 100%, indicating that it incurs no cost of goods sold (COGS). Operating expenses are a significant component, with general and administrative expenses being the largest at $35.06 million in the most recent period. Net income margin has shown an upward trend, reaching 41.77% in the last reported quarter.

PE: 11.2x

Commercial Bancgroup, a smaller player in the financial sector, recently reported a net income increase to US$9.53 million for Q1 2026 from US$8.69 million the previous year, despite slightly lower earnings per share. Insider confidence is evident as James Shoffner acquired 14,583 shares valued at approximately US$350,000. The company has initiated a share repurchase program worth up to US$10 million and continues to pay dividends of $0.10 per share. Earnings are projected to grow by 7.5% annually, suggesting potential value for investors seeking growth opportunities in this segment of the market.

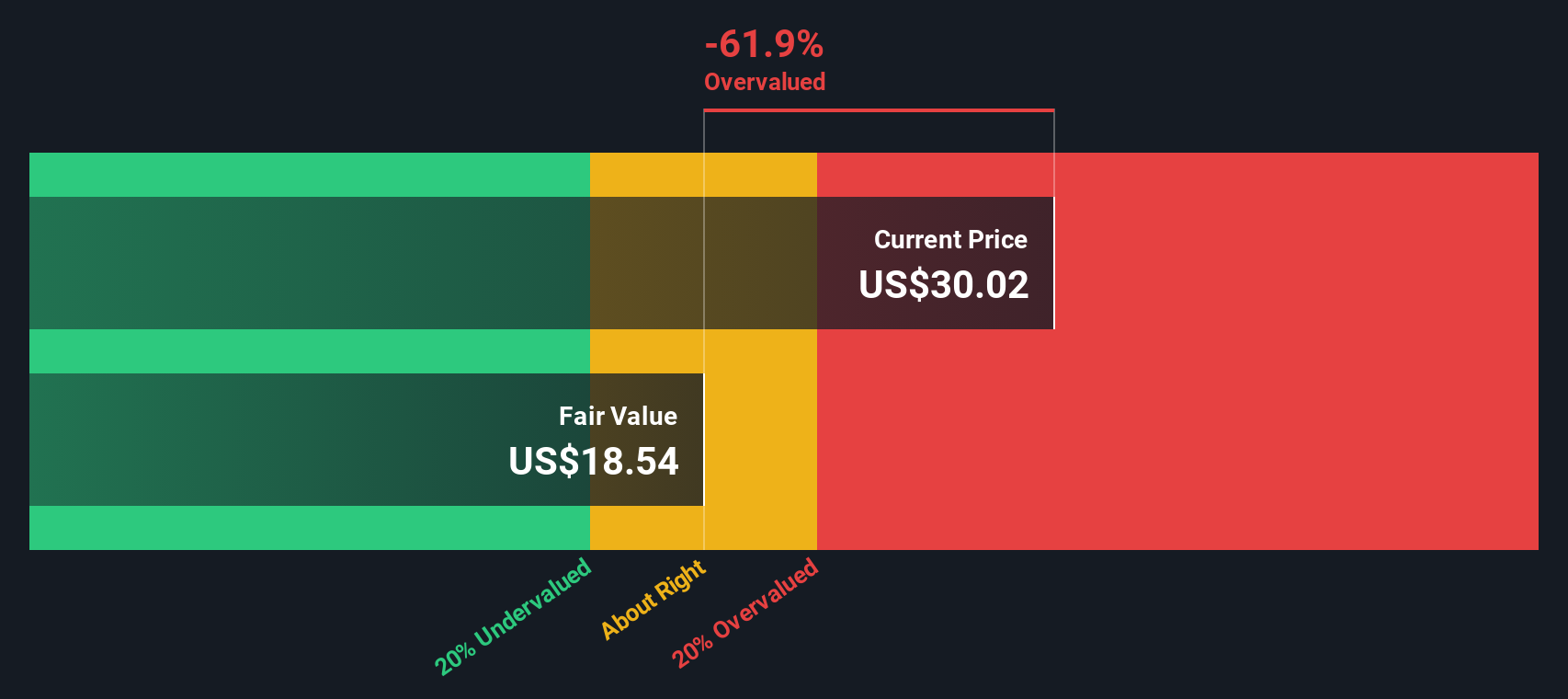

Appian (APPN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Appian is a software company specializing in low-code automation platforms that enable businesses to develop applications quickly, with a market capitalization of approximately $3.85 billion.

Operations: The company generates revenue primarily from its software and programming segment, reaching $762.69 million as of the latest quarter. Its gross profit margin has shown a notable trend, peaking at 75.28% before slightly decreasing to 72.47%. Operating expenses are significant, with sales and marketing being the largest component, followed by research and development costs. Despite consistent increases in revenue over time, net income margins have been negative but recently turned positive at 0.12%.

PE: 1737.8x

Appian, a tech company with a focus on AI and automation, recently expanded its alliance with Deloitte to modernize UK policing systems. This collaboration highlights Appian's strategic positioning in the market. The company has shown insider confidence through share repurchases amounting to US$21.81 million between February and March 2026. Despite reporting a net loss of US$1.53 million for Q1 2026, revenue grew significantly to US$202.18 million from the previous year, indicating potential growth prospects fueled by innovative partnerships and product enhancements like AI-assisted development tools.

Ingles Markets (IMKT.A)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ingles Markets operates a chain of supermarkets primarily in the southeastern United States, with a focus on retail and other segments, and has a market capitalization of approximately $1.86 billion.

Operations: Ingles Markets generates revenue primarily from its retail segment, accounting for approximately $5.18 billion. The company's cost of goods sold (COGS) and operating expenses are significant, impacting its net income margin which was 1.57% in the latest period. Gross profit margin has shown variation over time, most recently recorded at 24.41%.

PE: 16.3x

Ingles Markets, a smaller company in the U.S., recently reported second-quarter sales of US$1.31 billion, slightly down from last year, but net income rose to US$24.27 million from US$15.11 million previously. This indicates potential value as earnings per share increased significantly to US$1.28 from US$0.80. The company's board saw changes with Rory Held joining amid shareholder activism driven by Summer Road LLC, emphasizing operational transparency and strategic asset use concerns that could impact future growth strategies positively or negatively depending on resolution outcomes.

Turning Ideas Into Actions

- Unlock our comprehensive list of 61 Undervalued US Small Caps With Insider Buying by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.