Exploring 3 Undervalued Small Caps With Insider Activity Across Regions

Vertex, Inc. Class A VERX | 0.00 |

In the last week, the United States market has stayed flat, but over the past 12 months, it has risen by 16%, with earnings forecasted to grow by 15% annually. In this environment, identifying small-cap stocks that are perceived as undervalued and exhibit insider activity can offer intriguing opportunities for investors seeking potential growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| PCB Bancorp | 8.8x | 2.9x | 26.38% | ★★★★★☆ |

| Tennant | 28.1x | 1.0x | 48.51% | ★★★★★☆ |

| Financial Institutions | 8.6x | 2.7x | 43.94% | ★★★★★☆ |

| German American Bancorp | 14.1x | 4.6x | 46.08% | ★★★☆☆☆ |

| Franklin Financial Services | 10.6x | 2.6x | 2.09% | ★★★☆☆☆ |

| Union Bankshares | 10.2x | 2.1x | 21.25% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.4x | 1.9x | 47.94% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 46.36% | ★★★☆☆☆ |

| CEVA | NA | 4.9x | -16.14% | ★★★☆☆☆ |

| Douglas Emmett | 104.4x | 1.5x | 44.57% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

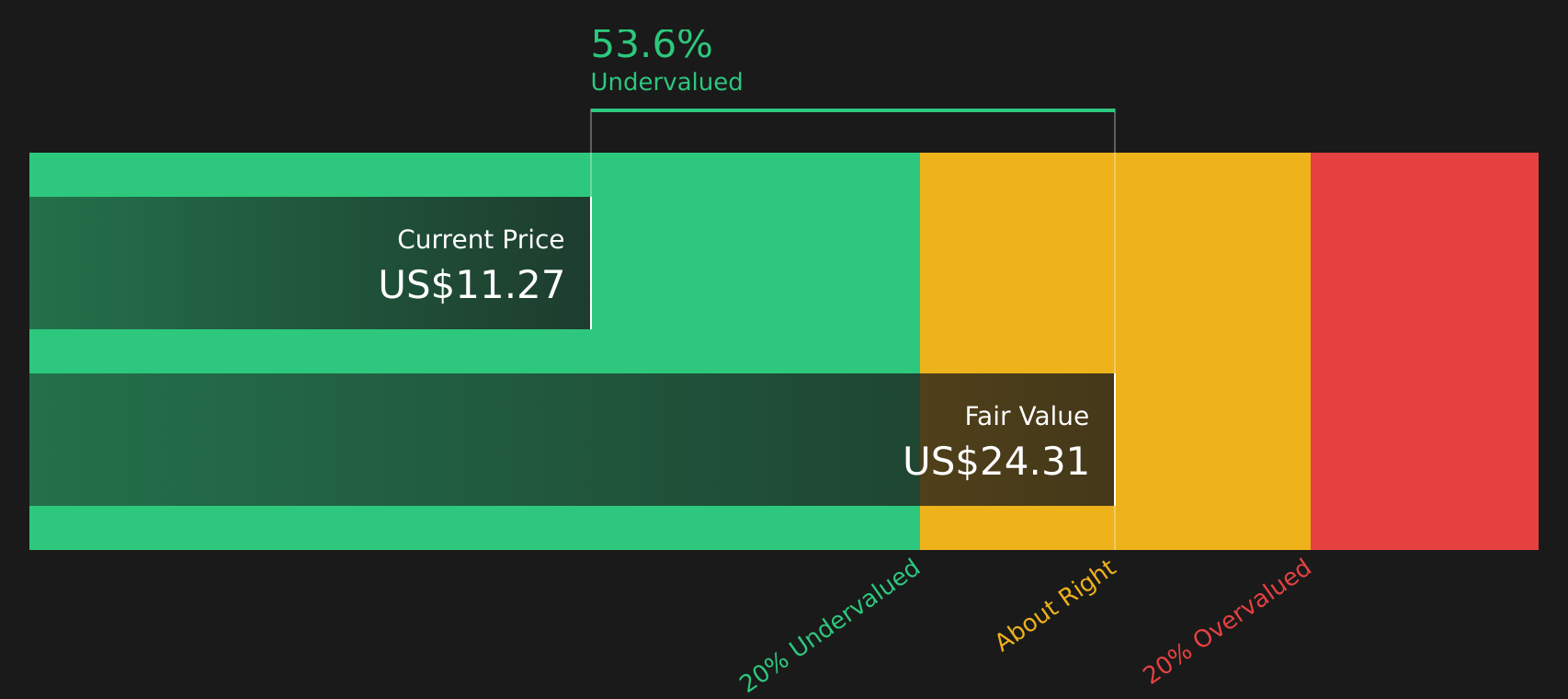

Vertex (VERX)

Simply Wall St Value Rating: ★★★★★☆

Overview: Vertex is a company specializing in software and programming solutions, with a market cap of approximately $2.45 billion.

Operations: Vertex generates revenue primarily from its software and programming segment, amounting to $748.44 million. The company's cost of goods sold (COGS) is $266.84 million, resulting in a gross profit margin of 64.35%. Operating expenses include significant allocations towards sales and marketing, research and development, and general administrative costs, impacting overall profitability.

PE: 267.3x

Vertex, a player in the tax technology sector, recently formed strategic alliances with xSuite Group to enhance their SAP offerings. The company's financial performance shows potential, with revenue rising to US$748 million in 2025 from US$667 million the previous year. A completed share repurchase of 503,890 shares for US$10.08 million indicates confidence in its value proposition. Despite external borrowing as a funding source, Vertex's earnings are projected to grow significantly by 59% annually.

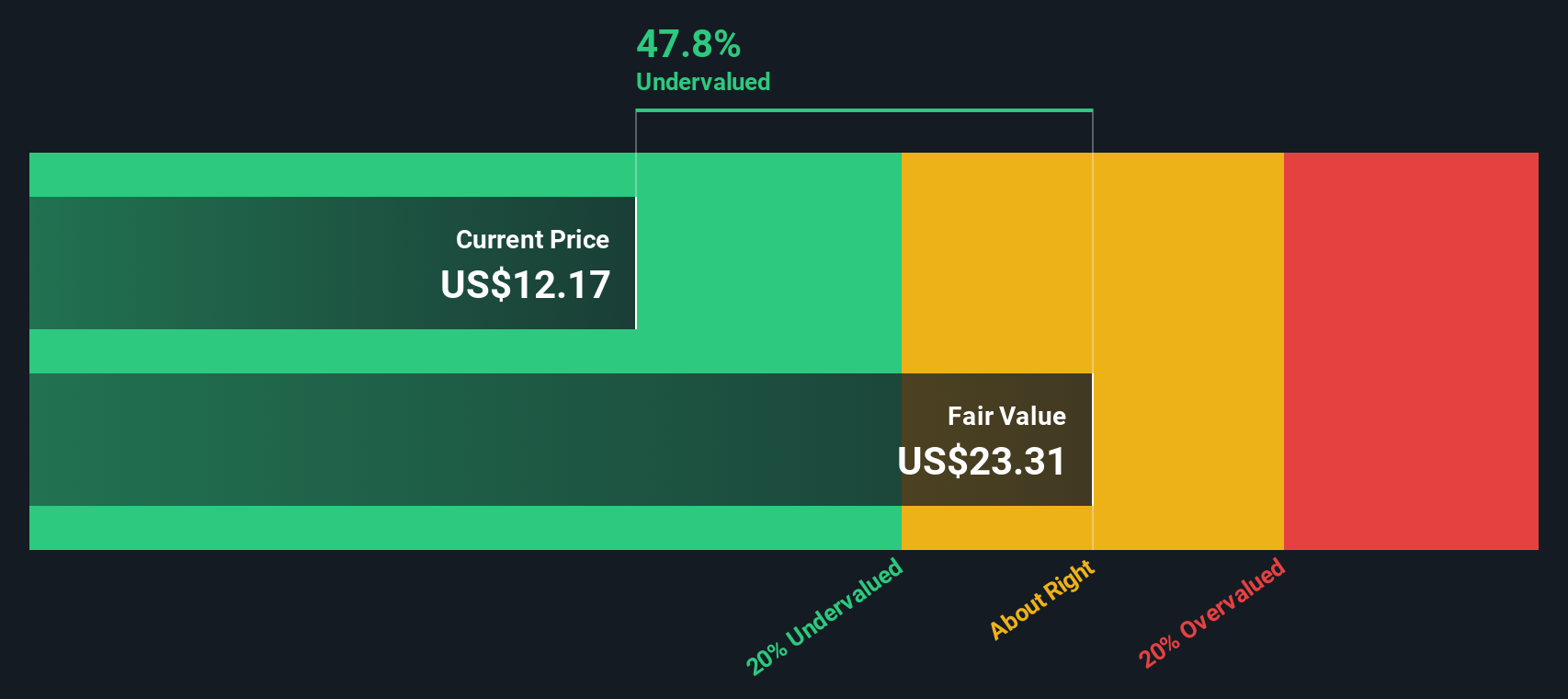

Northwest Bancshares (NWBI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Northwest Bancshares operates as a bank holding company providing a range of financial services through its community banking subsidiary, with a market cap of approximately $1.16 billion.

Operations: The company primarily generates revenue from its banking operations, with recent figures showing $599.09 million in revenue. Operating expenses are a significant cost component, totaling $376.82 million, including general and administrative expenses of $354.52 million and sales & marketing expenses of $8.66 million. The net income margin has shown fluctuations over time, with the latest figure at 21.02%.

PE: 15.0x

Northwest Bancshares, a smaller U.S. financial entity, showcases potential with its earnings growth forecast at 23.35% annually. Despite recent challenges from one-off items affecting results, the company reported net income of US$126 million for 2025, up from US$100 million in the previous year. Insider confidence is evident as executives have been purchasing shares throughout 2025 and early 2026. Future revenue guidance ranges between US$710 million to US$730 million for this year, signaling optimism amidst market uncertainties.

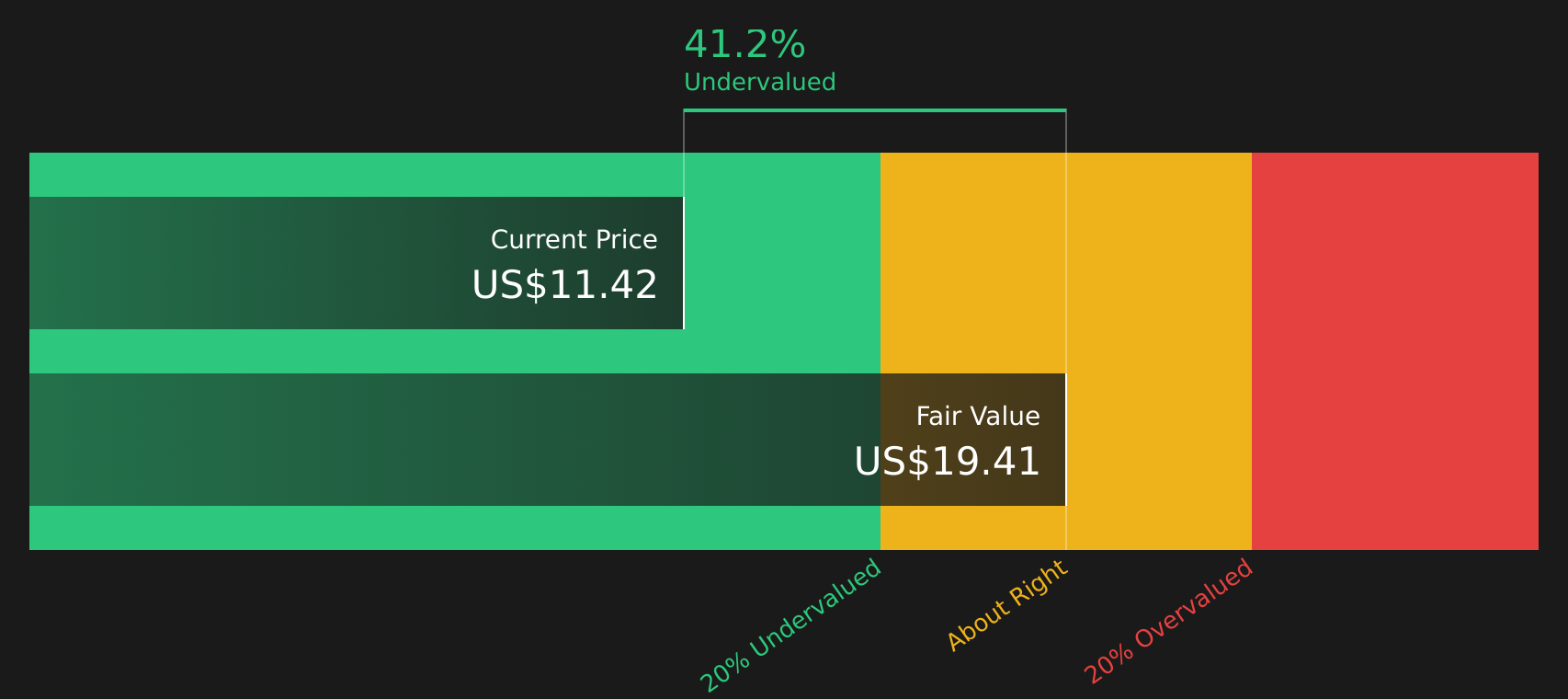

Bob's Discount Furniture (BOBS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bob's Discount Furniture operates in the retail home furnishing sector with a focus on providing affordable furniture options, and it has a market cap of $2.37 billion.

Operations: Bob's Discount Furniture generates revenue primarily from its retail home furnishing segment, with recent figures showing $2.37 billion. The company's gross profit margin was 46.76% in 2024 and adjusted to 45.66% by the end of 2025. Operating expenses include significant allocations to general and administrative costs, which were $781.26 million at the end of 2025, alongside sales and marketing expenditures totaling $137.40 million for the same period.

PE: 12.8x

Bob's Discount Furniture, a company with recent IPO activity amounting to US$330.65 million, has shown promising financial growth. For the full year ending December 28, 2025, sales reached US$2.37 billion from US$2.03 billion the previous year, while net income increased to US$121.72 million from US$87.93 million. Insider confidence is evident as Chief Growth Officer Stephen Moeller purchased 15,000 shares for approximately US$255,000 in March 2026. Despite high debt levels and reliance on external borrowing for funding, earnings are forecasted to grow by over 10% annually, suggesting potential for future expansion in the competitive furniture industry.

Taking Advantage

- Click this link to deep-dive into the 58 companies within our Undervalued US Small Caps With Insider Buying screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.