Exploring 3 Undervalued Small Caps With Insider Buying Across Regions

FMC Corporation FMC | 17.75 | +3.50% |

Over the last 7 days, the United States market has dropped 2.3%, yet it remains up by 13% over the past year with earnings forecasted to grow by 16% annually. In this context of fluctuating performance, identifying small-cap stocks with potential insider buying can be an intriguing strategy for investors seeking opportunities that may not be immediately apparent in larger market trends.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 49.24% | ★★★★★★ |

| Financial Institutions | 8.4x | 2.6x | 45.13% | ★★★★★☆ |

| AVITA Medical | NA | 1.6x | 35.55% | ★★★★★☆ |

| Tennant | 27.5x | 1.0x | 49.71% | ★★★★☆☆ |

| Franklin Financial Services | 10.6x | 2.6x | 2.55% | ★★★★☆☆ |

| 1st Source | 10.6x | 4.0x | 49.71% | ★★★★☆☆ |

| German American Bancorp | 13.8x | 4.5x | 47.30% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.5x | 2.0x | 47.39% | ★★★☆☆☆ |

| Douglas Emmett | 105.8x | 1.6x | 43.49% | ★★★☆☆☆ |

| First Northern Community Bancorp | 10.5x | 3.0x | 41.01% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Grocery Outlet Holding (GO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Grocery Outlet Holding operates a chain of discount grocery stores across the United States, with a market cap of approximately $2.17 billion.

Operations: Grocery Outlet Holding generates revenue primarily through its retail grocery stores, with a recent figure of $4.69 billion. The company's gross profit margin has shown some variation, reaching 31.30% in the latest period. Operating expenses are significant, including general and administrative costs that impact overall profitability.

PE: -2.8x

Grocery Outlet Holding, a smaller player in the U.S. retail sector, faces challenges with high debt levels and reliance on external borrowing. Recent legal issues and missed financial targets have pressured its stock price, which dropped 27.9% to US$6.34 on March 5, 2026. Despite plans to open new stores in Virginia and elsewhere, the company is closing 36 underperforming locations as part of a restructuring effort. The company's strategic shift aims for sustainable growth amid insider confidence shown through share purchases earlier this year.

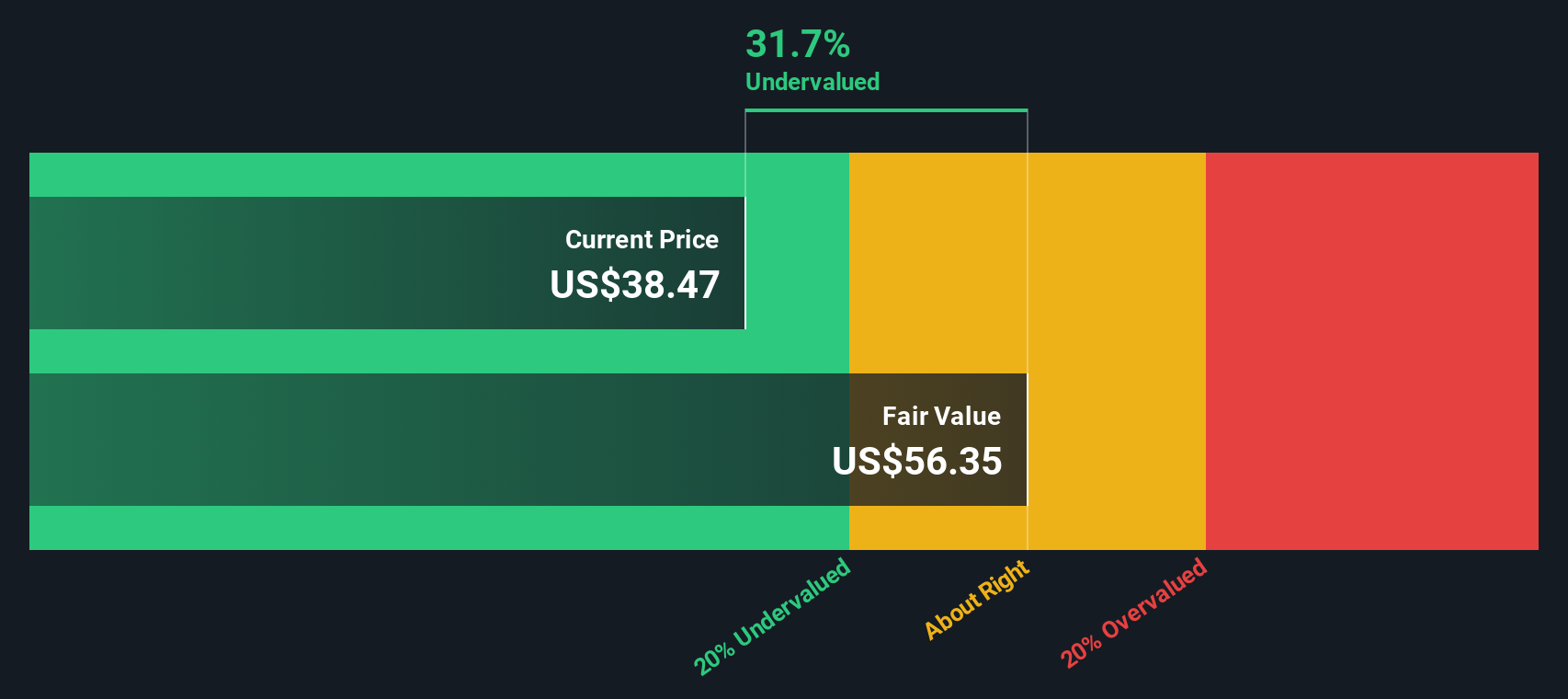

FMC (FMC)

Simply Wall St Value Rating: ★★★★★☆

Overview: FMC is a global agricultural sciences company that provides innovative solutions for crop protection, with a market capitalization of $13.45 billion.

Operations: The company generates revenue primarily from its Innovative Solutions segment, with recent quarterly revenue at $3.47 billion. The cost of goods sold (COGS) was reported at $2.30 billion, resulting in a gross profit of $1.17 billion and a gross profit margin of 33.81%. Operating expenses amounted to $932.1 million, while non-operating expenses were notably high at $2.44 billion, impacting the net income significantly to -$2.20 billion and resulting in a net income margin of -63.55%.

PE: -0.8x

FMC, a player in the specialty chemicals industry, is currently navigating challenging financial waters with a reported net loss of US$2.24 billion for 2025. Despite this, insider confidence is evident as Michael Barry purchased shares worth approximately US$250,000 in February 2026. The company is innovating with rimisoxafen, a dual-mode herbicide poised to address global agricultural challenges. Upcoming bylaw changes aim to enhance shareholder rights and strategic flexibility as FMC explores options to strengthen its portfolio and competitiveness.

Harley-Davidson (HOG)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Harley-Davidson is a renowned manufacturer of heavyweight motorcycles, complemented by its financial services segment, with a market capitalization of approximately $5.74 billion.

Operations: The company's revenue streams are primarily derived from HDMC, contributing $3.58 billion, and HDFS at $869.20 million, with Livewire generating $25.67 million. Over recent periods, the gross profit margin has shown variability, reaching 31.75% in late 2025 before adjusting to 29.84% by early 2026. Operating expenses have been a significant cost factor impacting net income margins across various periods observed.

PE: 6.1x

Harley-Davidson, a prominent player in the motorcycle industry, has caught attention due to its current market valuation. Despite facing financial challenges with a net loss of US$279 million in Q4 2025 and declining revenues of US$4.47 billion for the year, insider confidence is evident as CEO Arthur Starrs acquired 15,000 shares worth US$286,500 in March 2026. The company also repurchased over 16 million shares by December 2025. While earnings are expected to decline by an average of 7.3% annually over the next three years and liabilities are entirely funded through higher-risk external borrowing, Harley's strategic product launches and dividend increases may indicate potential for long-term value creation despite short-term hurdles.

Make It Happen

- Discover the full array of 65 Undervalued US Small Caps With Insider Buying right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.