Exploring 3 Undiscovered Gems In The US Market

Consolidated Water CWCO | 0.00 |

Over the last 7 days, the United States market has risen 2.5%, contributing to a remarkable 26% increase over the past year, with earnings forecasted to grow by 17% annually. In this thriving environment, identifying stocks that possess strong fundamentals and growth potential can be key to uncovering undiscovered gems in the US market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Security Federal | 18.41% | 5.46% | -0.53% | ★★★★★★ |

| Southern Michigan Bancorp | 108.80% | 7.38% | 0.84% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| Teekay | 2.14% | 10.67% | 57.58% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.26% | 11.00% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| NameSilo Technologies | 3.13% | 14.25% | 15.06% | ★★★★★☆ |

Let's uncover some gems from our specialized screener.

Alerus Financial (ALRS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Alerus Financial Corporation is a bank holding company for Alerus Financial, National Association, offering a range of financial services to businesses and consumers across the United States, with a market capitalization of approximately $704.86 million.

Operations: Alerus Financial generates revenue primarily from its Banking, Wealth Advisory Services, and Retirement and Benefit Services segments, totaling $239.54 million. The Banking segment is the largest contributor with $143.76 million in revenue.

Alerus Financial, with assets totaling US$5.3 billion and equity of US$574.7 million, is a financial services provider in the U.S. The company has total deposits of US$4.3 billion and loans amounting to US$4 billion, with a net interest margin of 3.5%. It maintains an appropriate level of bad loans at 1.3%, though its allowance for these is low at 94%. Recent strategic moves include a dividend increase to $0.22 per share and repurchasing 250,000 shares for $5.98 million this year, indicating active capital management efforts amidst growth prospects in technology investments and demographic shifts in retirement solutions.

Alto Ingredients (ALTO)

Simply Wall St Value Rating: ★★★★★☆

Overview: Alto Ingredients, Inc. is engaged in the production, distribution, and marketing of specialty alcohols, renewable fuel, and essential ingredients within the United States with a market capitalization of approximately $364.18 million.

Operations: The company's primary revenue streams include Pekin Campus Production at $591.55 million and Marketing and Distribution at $229.35 million, with Western Production contributing $100.64 million. Net profit margin trends could offer insights into the company's profitability dynamics over time, but specific figures are not provided here for analysis.

Alto Ingredients is making waves in the renewable fuels sector, with recent profitability marking a significant turnaround from prior losses. The company's net debt to equity ratio stands at a satisfactory 21.1%, reflecting prudent financial management over five years, reducing from 33.8% to 29.2%. Trading at 81.9% below its estimated fair value, Alto appears undervalued compared to industry peers. Despite challenges like volatile ethanol markets and policy shifts, earnings are projected to grow by 31% annually, while interest coverage remains low at 1.9x EBIT—highlighting potential risks amidst growth opportunities and strategic acquisitions like Carbonic enhancing margins.

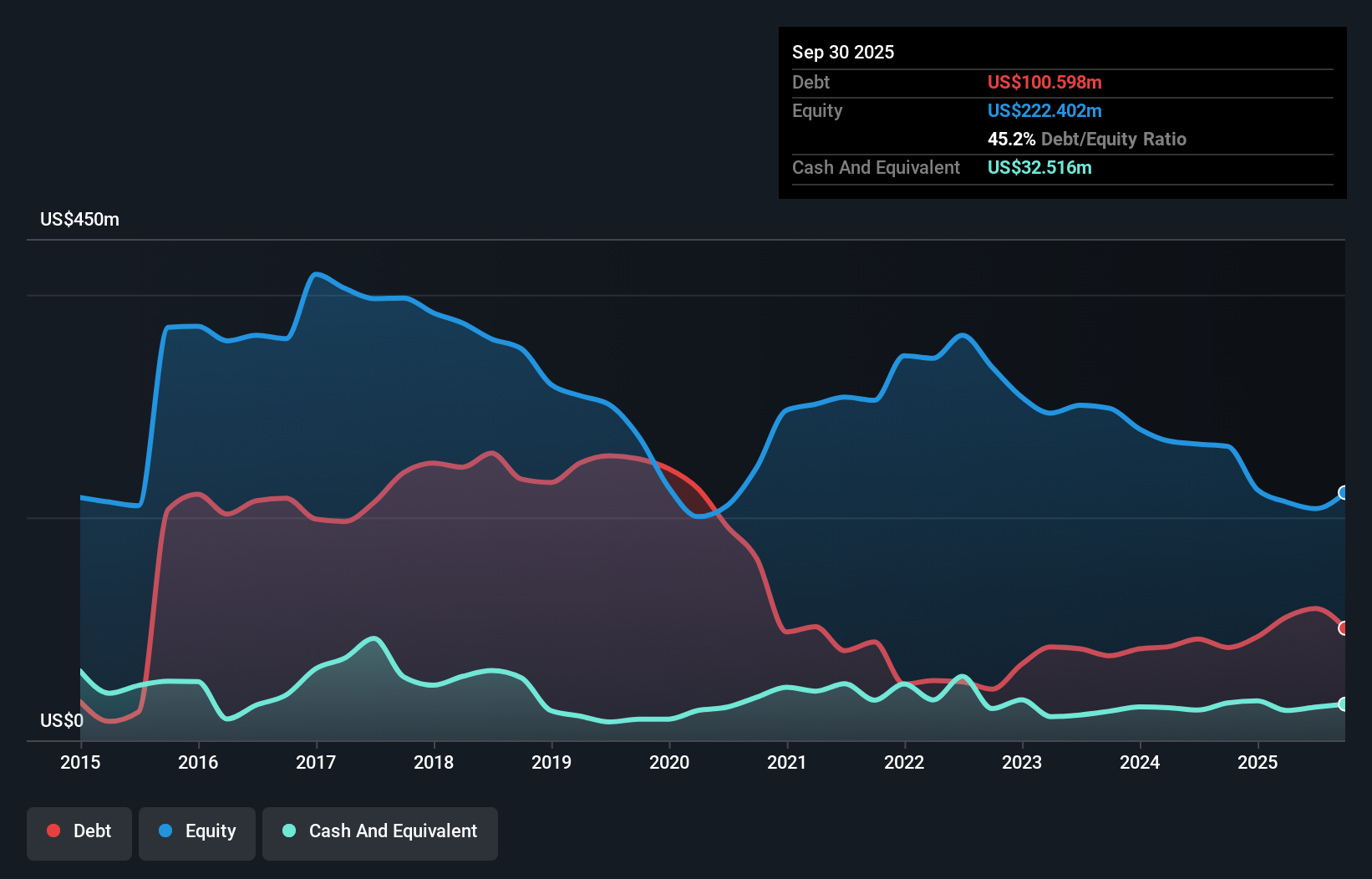

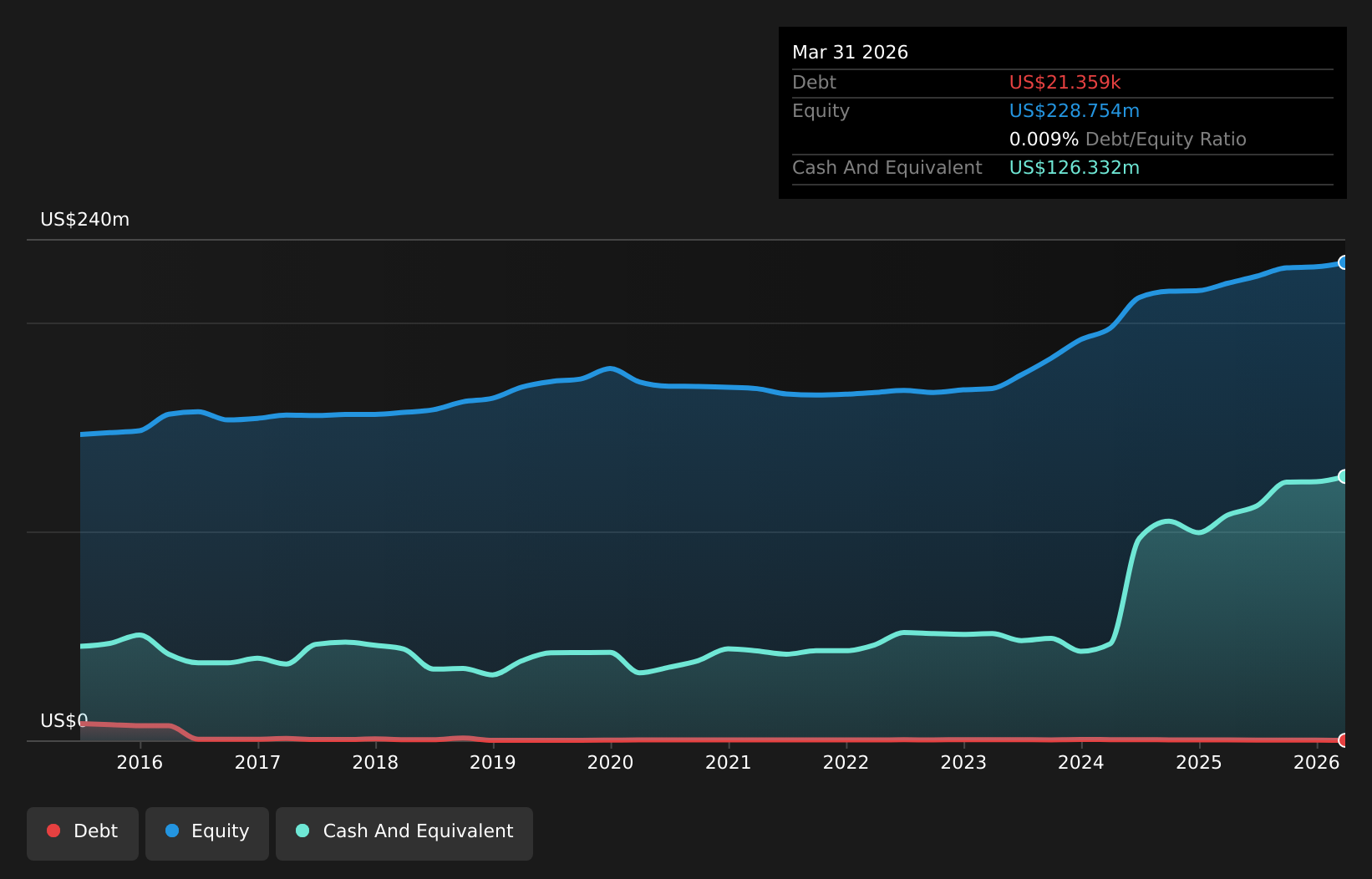

Consolidated Water (CWCO)

Simply Wall St Value Rating: ★★★★★★

Overview: Consolidated Water Co. Ltd., along with its subsidiaries, operates in the Cayman Islands, the Bahamas, the United States, and the British Virgin Islands by supplying potable water, treating wastewater and water for reuse, and offering water-related products and services; it has a market cap of $470.57 million.

Operations: The company's revenue streams are diversified across four segments: Bulk ($33.81 million), Retail ($32.75 million), Manufacturing ($14.28 million), and Services Excluding Manufacturing ($47.49 million).

Consolidated Water, a notable player in the water utilities sector, is leveraging its robust balance sheet to pursue strategic acquisitions and expand its desalination projects. The company's recent earnings call highlighted a decrease in quarterly sales to US$29.97 million from US$33.72 million last year, with net income dropping to US$3.78 million from US$4.79 million. Despite these figures, the company maintains a debt-to-equity ratio of 0.01%, significantly reduced over five years, while trading at 17% below fair value estimates suggests potential upside for investors considering future growth strategies and market expansion opportunities in regions like Hawaii and Florida.

Make It Happen

- Unlock more gems! Our US Undiscovered Gems With Strong Fundamentals screener has unearthed 336 more companies for you to explore.Click here to unveil our expertly curated list of 339 US Undiscovered Gems With Strong Fundamentals.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.