Exploring April 2026's Undiscovered Gems in the Middle East

ACC 3010.SA | 23.45 | -0.64% |

As the Middle East markets experience a boost, led by Dubai's gains amid hopes of de-escalation in regional tensions and supportive economic measures, investors are closely watching the small-cap segment for potential opportunities. In this dynamic environment, identifying stocks with strong fundamentals and resilience to geopolitical fluctuations can be crucial for those seeking to uncover hidden gems in the region.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| Baazeem Trading | 10.02% | -1.27% | -1.66% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | NA | 17.87% | 23.67% | ★★★★★★ |

| Nofoth Food Products | NA | 20.62% | 23.75% | ★★★★★★ |

| MOBI Industry | 22.69% | 5.89% | 17.98% | ★★★★★★ |

| Najran Cement | 14.49% | -4.20% | -30.16% | ★★★★★★ |

| Alf Meem Yaa for Medical Supplies and Equipment | 27.12% | 12.68% | 18.39% | ★★★★★☆ |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi | 2.52% | 43.31% | 23.27% | ★★★★★☆ |

| Saudi Chemical Holding | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Etihad GO Telecom | NA | 38.31% | 54.97% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

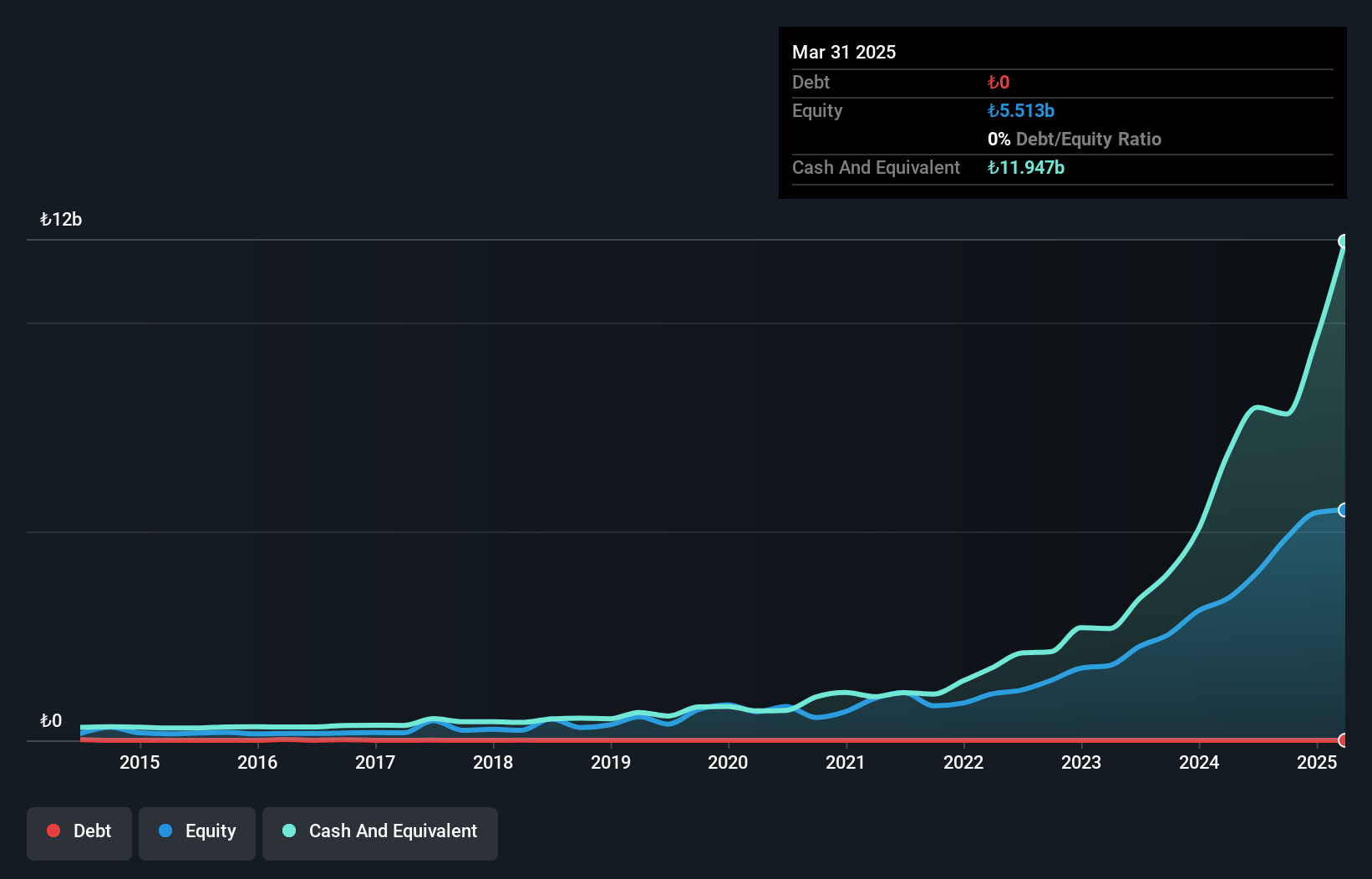

AgeSA Hayat ve Emeklilik Anonim Sirketi (IBSE:AGESA)

Simply Wall St Value Rating: ★★★★★☆

Overview: AgeSA Hayat ve Emeklilik Anonim Sirketi operates in Turkey offering life insurance products through its subsidiaries, with a market capitalization of TRY40.89 billion.

Operations: AgeSA generates revenue primarily from its life insurance products, with significant contributions from Life Insurance - Life Protection at TRY17.37 billion and Life Insurance - Pension at TRY9.10 billion. The company's market capitalization stands at TRY40.89 billion.

AgeSA Hayat ve Emeklilik showcases a robust financial profile with earnings surging 93.5% last year, outperforming the insurance sector's 46% growth. The company operates debt-free, eliminating concerns over interest coverage and enhancing its appeal in the market with a favorable price-to-earnings ratio of 7.4x against the TR market's 17.2x. Reporting high-quality earnings, AgeSA is also free cash flow positive, underscoring its financial health and operational efficiency. Recently announced dividends of TRY 6.94 per share further highlight shareholder value focus amidst reporting net income of TRY 5,555 million for the full year ending December 2025.

Arabian Cement (SASE:3010)

Simply Wall St Value Rating: ★★★★★★

Overview: Arabian Cement Company is involved in the production, trading, and selling of cement across Saudi Arabia and Jordan with a market capitalization of SAR2.42 billion.

Operations: Arabian Cement generates revenue primarily through the production and sale of cement in Saudi Arabia and Jordan. The company's financial performance is influenced by its cost structure, which includes raw material costs, energy expenses, and operational efficiencies. Its net profit margin reflects these dynamics within the cement industry.

Arabian Cement, a notable player in the Middle East's cement industry, has shown resilience with its earnings growth of 3.9%, outpacing the Basic Materials industry's -10.1%. The company's debt to equity ratio impressively reduced from 11.3% to 0.7% over five years, indicating strong financial management and more cash than total debt suggests robust liquidity. With a price-to-earnings ratio of 15.3x, it remains an attractive option compared to the SA market average of 17.3x. Recent earnings reveal sales climbing to SAR 1,062 million from SAR 857 million last year, while net income reached SAR 165 million up from SAR 160 million previously reported.

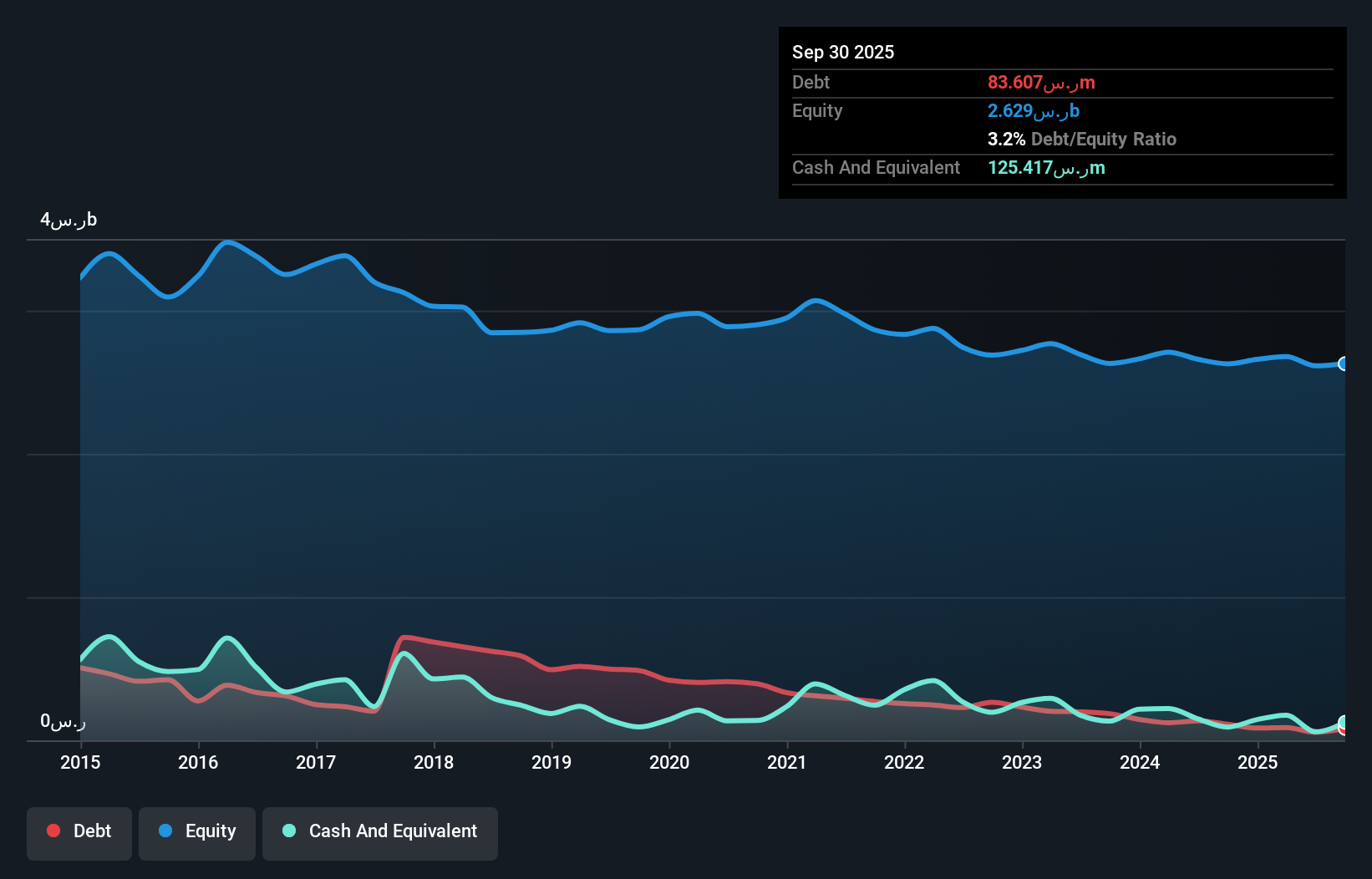

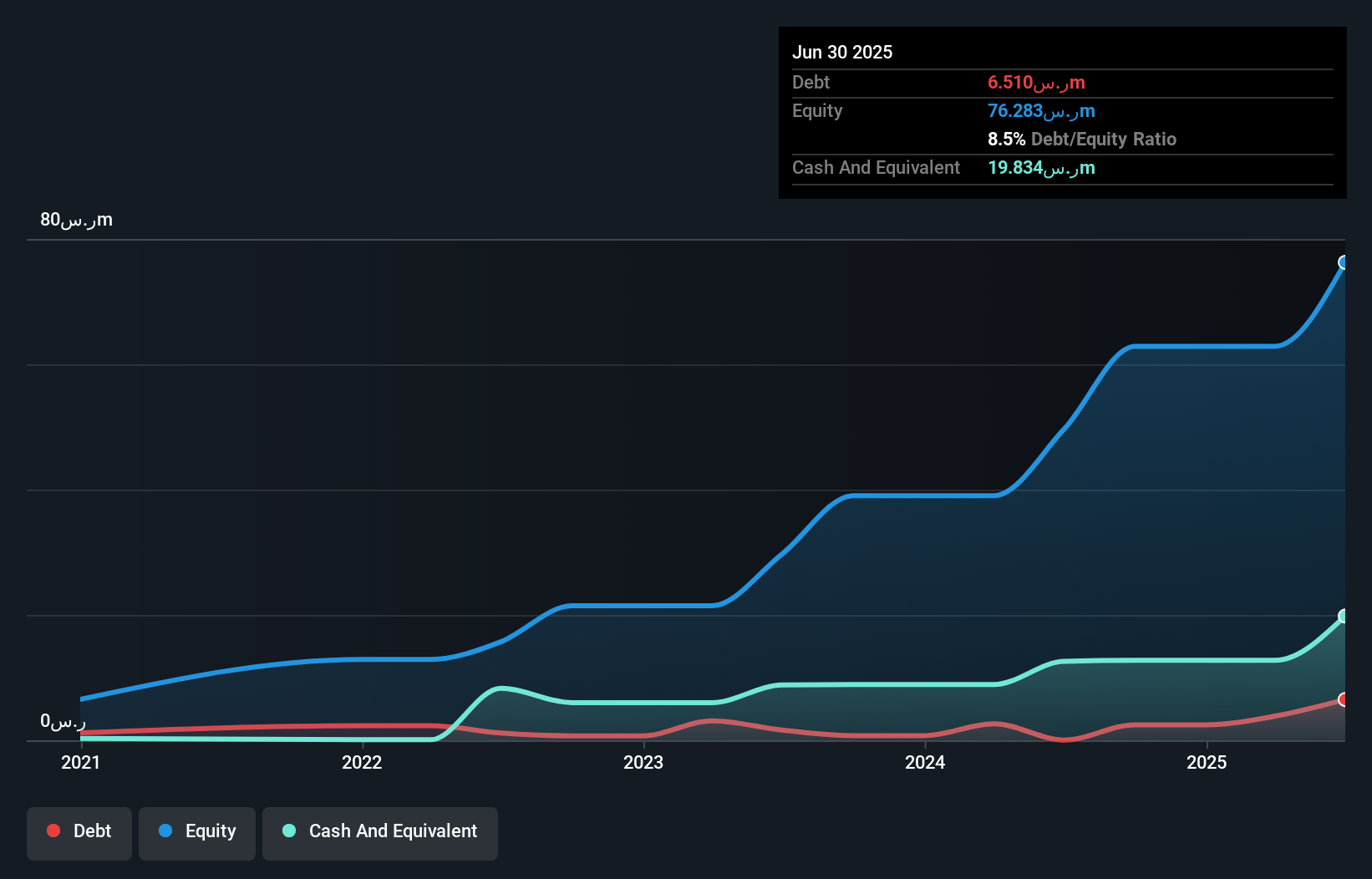

Edarat Communication and Information Technology (SASE:9557)

Simply Wall St Value Rating: ★★★★★★

Overview: Edarat Communication and Information Technology Co. operates in the technology sector, focusing on communication and IT services, with a market capitalization of SAR1.79 billion.

Operations: Edarat Communication and Information Technology Co. generates revenue primarily from communication and IT services. The company's gross profit margin is 28.5%, reflecting its cost management efficiency within the sector.

Edarat Communication and Information Technology, a nimble player in the Middle East's tech sector, has seen its earnings grow by 47.4% over the past year, outpacing the IT industry's 11.4%. With a debt-to-equity ratio dropping from 18.3% to 8.5% in five years and trading at 30.3% below estimated fair value, it presents an intriguing proposition for investors seeking value. Recent client announcements include a significant contract with Banque Saudi Fransi for data center colocation services, potentially boosting future revenue streams beyond its SAR192 million reported sales last year and net income of SAR36 million.

Key Takeaways

- Get an in-depth perspective on all 212 Middle Eastern Undiscovered Gems With Strong Fundamentals by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.