Exploring Limak Dogu Anadolu Cimento Sanayi ve Ticaret Anonim Sirketi And 2 Other Undiscovered Gems In The Middle East

ALMUNAJEM 4162.SA | 0.00 |

The Middle East market has been experiencing a period of cautious sentiment, with most Gulf indices dipping amid geopolitical tensions and fluctuating energy prices. Despite these challenges, the region continues to offer unique opportunities for investors willing to explore lesser-known stocks that may benefit from strategic positioning and resilience in the face of uncertainty.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| C. Mer Industries | 70.13% | 13.00% | 68.68% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 14.04% | 16.38% | 23.83% | ★★★★★★ |

| MOBI Industry | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| Nofoth Food Products | NA | 15.50% | 18.29% | ★★★★★★ |

| Kirac Galvaniz Telekominikasyon Metal Makine Insaat Elektrik Sanayi ve Ticaret Anonim Sirketi | 21.92% | 19.33% | 42.01% | ★★★★★☆ |

| Smart Shooter | 69.58% | 83.01% | nan | ★★★★★☆ |

| Saudi Chemical Holding | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Etihad GO Telecom | 0.74% | 38.31% | 54.97% | ★★★★★☆ |

| Zahrat Al Waha For Trading | 56.06% | -0.88% | -37.72% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

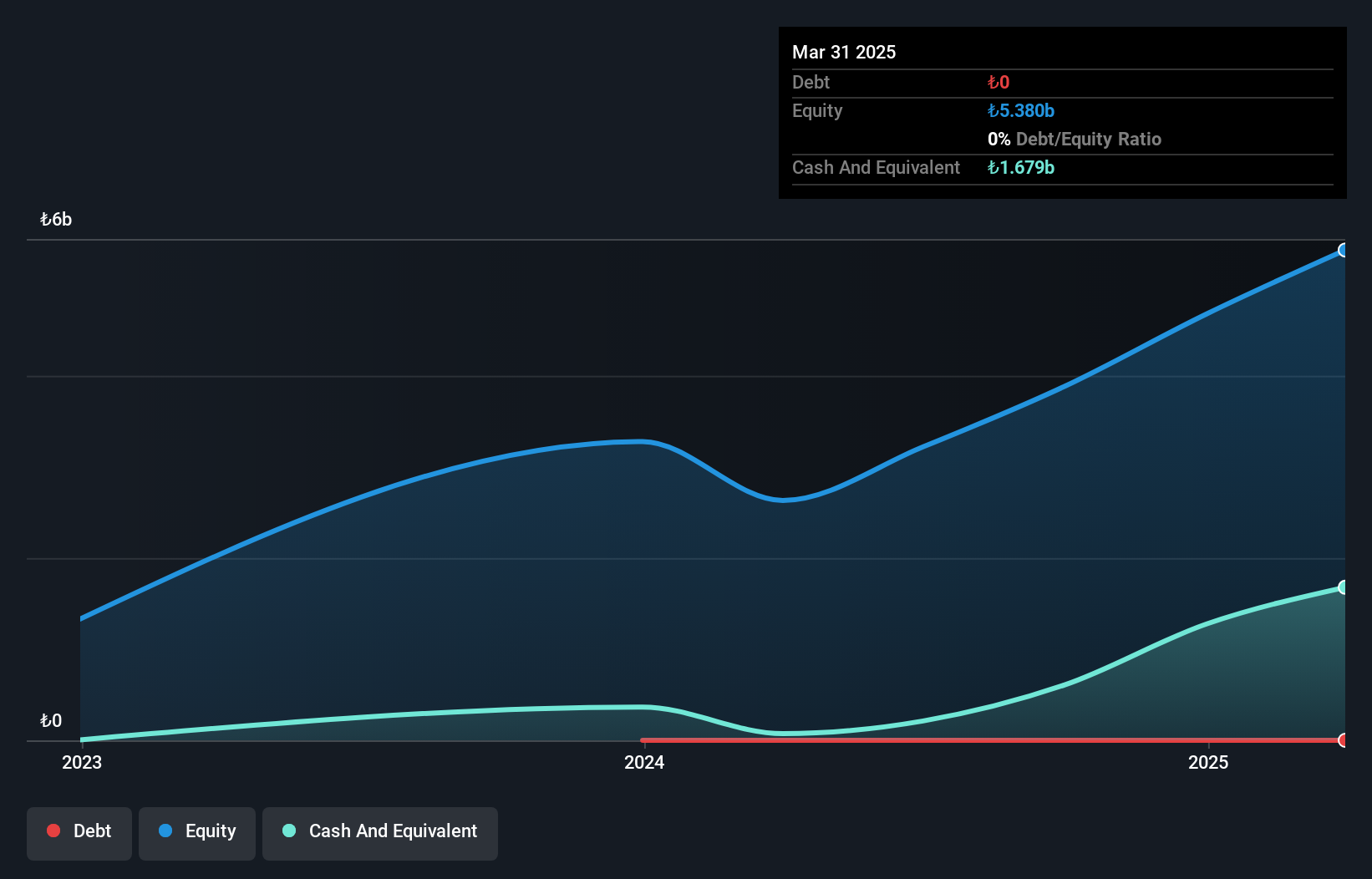

Limak Dogu Anadolu Cimento Sanayi ve Ticaret Anonim Sirketi (IBSE:LMKDC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Limak Dogu Anadolu Cimento Sanayi ve Ticaret Anonim Sirketi focuses on the production and sale of cement and clinker products in Turkey, with a market capitalization of TRY19.25 billion.

Operations: LMKDC generates revenue primarily from the sale of cement and clinker products in Turkey. The company's financial data indicates a market capitalization of TRY19.25 billion.

Limak Dogu Anadolu Cimento showcases a robust financial profile with earnings growth of 20.6% over the past year, outpacing the Basic Materials industry's -35.8%. The company's Price-To-Earnings ratio at 11.1x is notably lower than the TR market average of 22.1x, suggesting potential undervaluation. Despite having more cash than total debt and positive free cash flow, recent quarterly results reveal some challenges; sales dropped to TRY 1,388 million from TRY 1,684 million and net income fell sharply to TRY 9 million from TRY 297 million year-on-year for Q1 2026, hinting at possible operational or market pressures.

Almunajem Foods (SASE:4162)

Simply Wall St Value Rating: ★★★★★☆

Overview: Almunajem Foods Company, along with its subsidiary, operates in the wholesale and retail sectors for fruits, vegetables, cold and frozen poultry and meat, as well as bottled goods and other food items in Saudi Arabia, with a market cap of SAR3.63 billion.

Operations: The company generates revenue primarily from the wholesale and retail trade of various food products in Saudi Arabia. It focuses on fruits, vegetables, cold and frozen poultry, meat, and bottled goods. The net profit margin has shown variability over recent periods.

Almunajem Foods, a smaller player in the Middle East food industry, showcases solid financial health with high-quality earnings and positive free cash flow. Despite a rise in its debt to equity ratio from 15.7% to 27.3% over five years, the net debt to equity remains satisfactory at 22.8%. The company's interest payments are well covered by EBIT at 14.4 times coverage, indicating strong operational performance. Recent earnings showed a net income of SAR 97 million for Q1 2026, up from SAR 40 million the previous year, although sales dipped slightly to SAR 861 million from SAR 901 million.

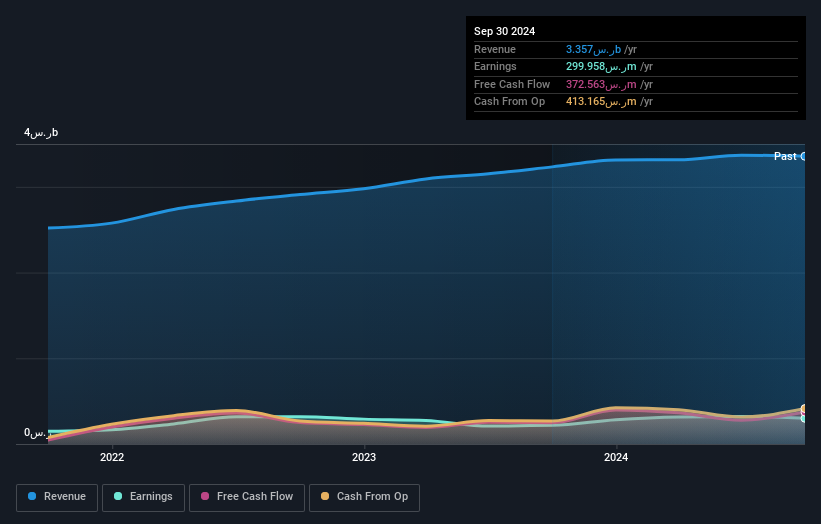

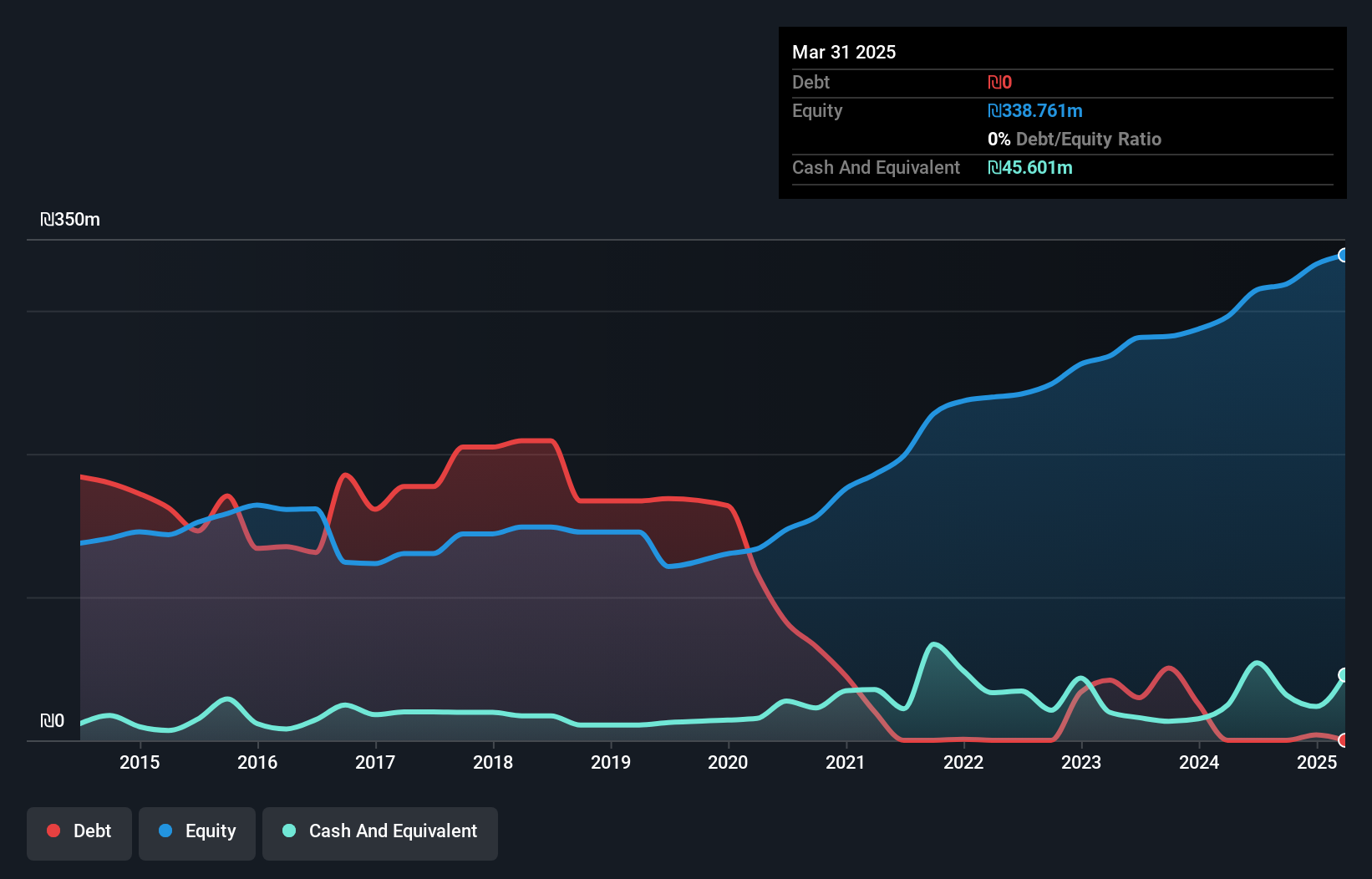

Tiv Taam Holdings 1 (TASE:TTAM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Tiv Taam Holdings 1 Ltd. engages in the production, marketing, and importation of food products in Israel with a market capitalization of approximately ₪1.51 billion.

Operations: The company generates revenue primarily from its retail segment, contributing ₪1.59 billion, and trade segment, adding ₪570.50 million.

Tiv Taam Holdings 1, a nimble player in the Middle East market, has shown impressive earnings growth of 26.3% over the past year, outpacing the Consumer Retailing industry average of 8.2%. The company trades at a significant discount, 69.4% below its estimated fair value, suggesting potential upside for investors. Financially sound with an interest coverage ratio of 4.9x and a reduced debt to equity ratio from 25.6% to 15.6% over five years, Tiv Taam appears well-positioned despite historical earnings declines of 4.5% annually over five years; recent net income rose to ILS73 million from ILS58 million last year.

Taking Advantage

- Dive into all 223 of the Middle Eastern Undiscovered Gems With Strong Fundamentals we have identified here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.