Exploring Middle Eastern Market with These 3 Undiscovered Gems

MAHARAH 1831.SA | 0.00 |

Amidst ongoing regional tensions and fluctuating investor sentiment, the Middle Eastern stock markets have experienced a retreat, with key indices such as Saudi Arabia's benchmark index declining due to geopolitical uncertainties. Despite these challenges, the region continues to offer unique opportunities for investors seeking potential growth in lesser-known stocks that may thrive by navigating these complex conditions effectively.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| Nofoth Food Products | NA | 20.62% | 23.75% | ★★★★★★ |

| Payton Industries | NA | 1.92% | 13.55% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 14.04% | 16.38% | 23.83% | ★★★★★★ |

| MOBI Industry | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| Baazeem Trading | 9.26% | -0.72% | -0.40% | ★★★★★☆ |

| Saudi Chemical Holding | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Etihad GO Telecom | 0.74% | 38.31% | 54.97% | ★★★★★☆ |

| Zahrat Al Waha For Trading | 56.06% | -0.88% | -37.72% | ★★★★☆☆ |

| Odas Elektrik Üretim Sanayi Ticaret | 4.18% | 22.26% | -13.16% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

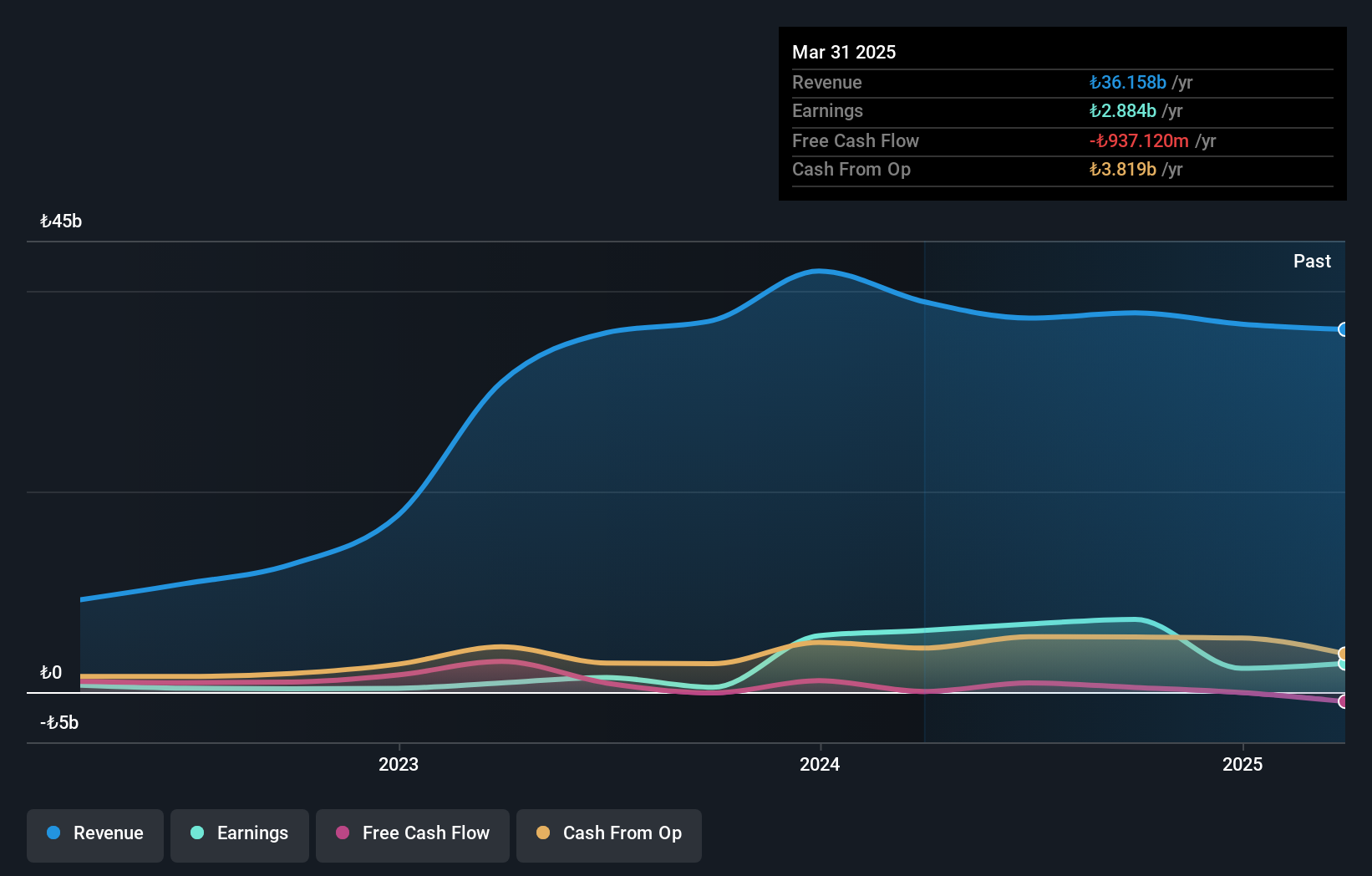

Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi (IBSE:BASGZ)

Simply Wall St Value Rating: ★★★★★☆

Overview: Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi A.S. is involved in the distribution of natural gas and operates with a market capitalization of TRY36.09 billion.

Operations: The company generates revenue primarily from the distribution of natural gas. It operates with a market capitalization of TRY36.09 billion.

Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi, a notable player in the gas utilities sector, showcases robust financial health with earnings growth of 9.2% over the past year, outpacing the industry average of 0.2%. The company's debt-to-equity ratio has impressively decreased from 41.5% to 7.9% in five years, indicating prudent financial management. With a price-to-earnings ratio of 10.6x compared to Turkey's market average of 21.3x, it appears undervalued relative to peers. Despite a slight dip in Q1 net income at TRY 2,068 million from TRY 2,520 million last year, its high-quality earnings and strong cash position suggest resilience and potential for continued stability in dividends with an upcoming payout of TRY 2 per share this July.

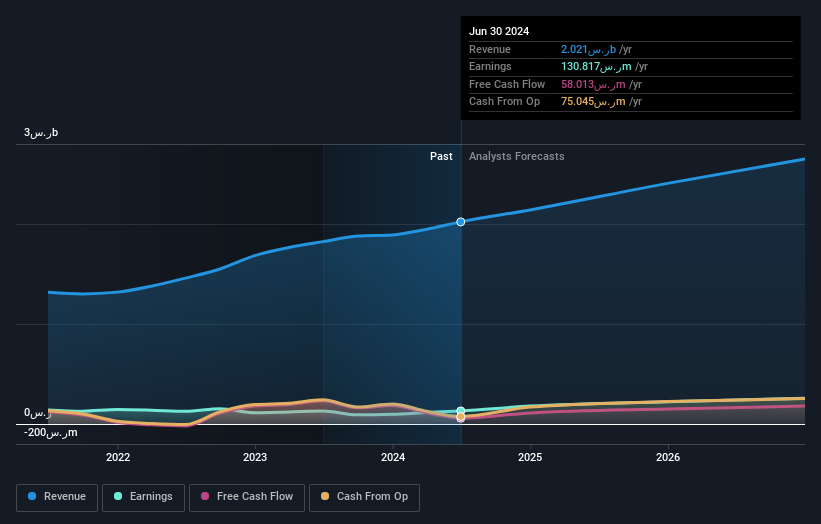

Maharah for Human Resources (SASE:1831)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Maharah for Human Resources Company provides manpower services to both public and private sectors in Saudi Arabia and the United Arab Emirates, with a market capitalization of SAR2.79 billion.

Operations: Maharah's primary revenue stream is from its Corporate segment, generating SAR2.68 billion, followed by the Individual segment at SAR492.80 million. The Facility Management segment contributes SAR94.14 million to the total revenue.

Maharah for Human Resources, a promising player in the Middle East, has shown impressive financial performance. Over the past year, earnings surged by 55.6%, outpacing the Professional Services industry growth of 11%. The company's net debt to equity ratio stands at a satisfactory 6.6%, indicating prudent financial management despite an increase from 0% to 35.2% over five years. Trading at a price-to-earnings ratio of 10.2x, Maharah is attractively valued compared to the Saudi Arabian market average of 17.8x. Recent announcements include a significant rise in sales to SAR 3.11 billion and net income reaching SAR 272 million for fiscal year-end December 2025, reflecting robust operational success and shareholder value enhancement through dividend distributions totaling SAR 58 million in April this year.

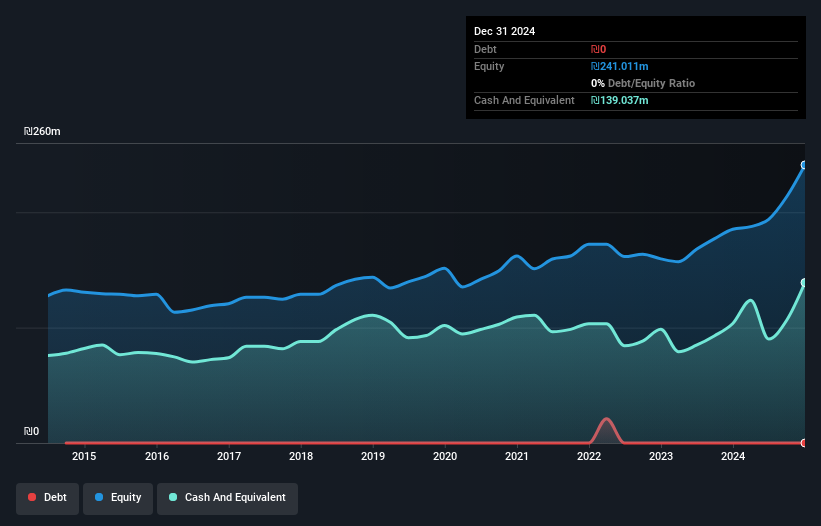

Analyst I.M.S. Investment Management Services (TASE:ANLT)

Simply Wall St Value Rating: ★★★★★★

Overview: Analyst I.M.S. Investment Management Services Ltd is a publicly owned investment manager with a market cap of ₪1.98 billion.

Operations: The company generates revenue primarily from investment management, totaling ₪512.90 million, with additional contributions from investments for its own account at ₪31.11 million. The net profit margin is a key indicator of financial performance, reflecting the company's ability to convert revenue into profit after all expenses are accounted for.

I.M.S. Investment Management Services, a nimble player in the Middle East market, has shown impressive growth with earnings surging 73.9% over the past year, outpacing industry peers by a notable margin. The company boasts zero debt, eliminating concerns over interest coverage and enhancing its financial stability. Recent results reveal net income of ILS 112.73 million for 2025, up from ILS 64.82 million the previous year, alongside an annual dividend increase to ILS 3 per share. With high-quality non-cash earnings and robust free cash flow of approximately US$2 billion in recent quarters, it seems poised for continued momentum in its sector.

Where To Now?

- Explore the 220 names from our Middle Eastern Undiscovered Gems With Strong Fundamentals screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.