Fannie Mae (OTCPK:FNMA) Q3 Net Income Rebound Challenges Persistent Loss Narrative

FEDERAL NATIONAL MORTGAGE ASSOC FNMA | 6.89 | -2.61% |

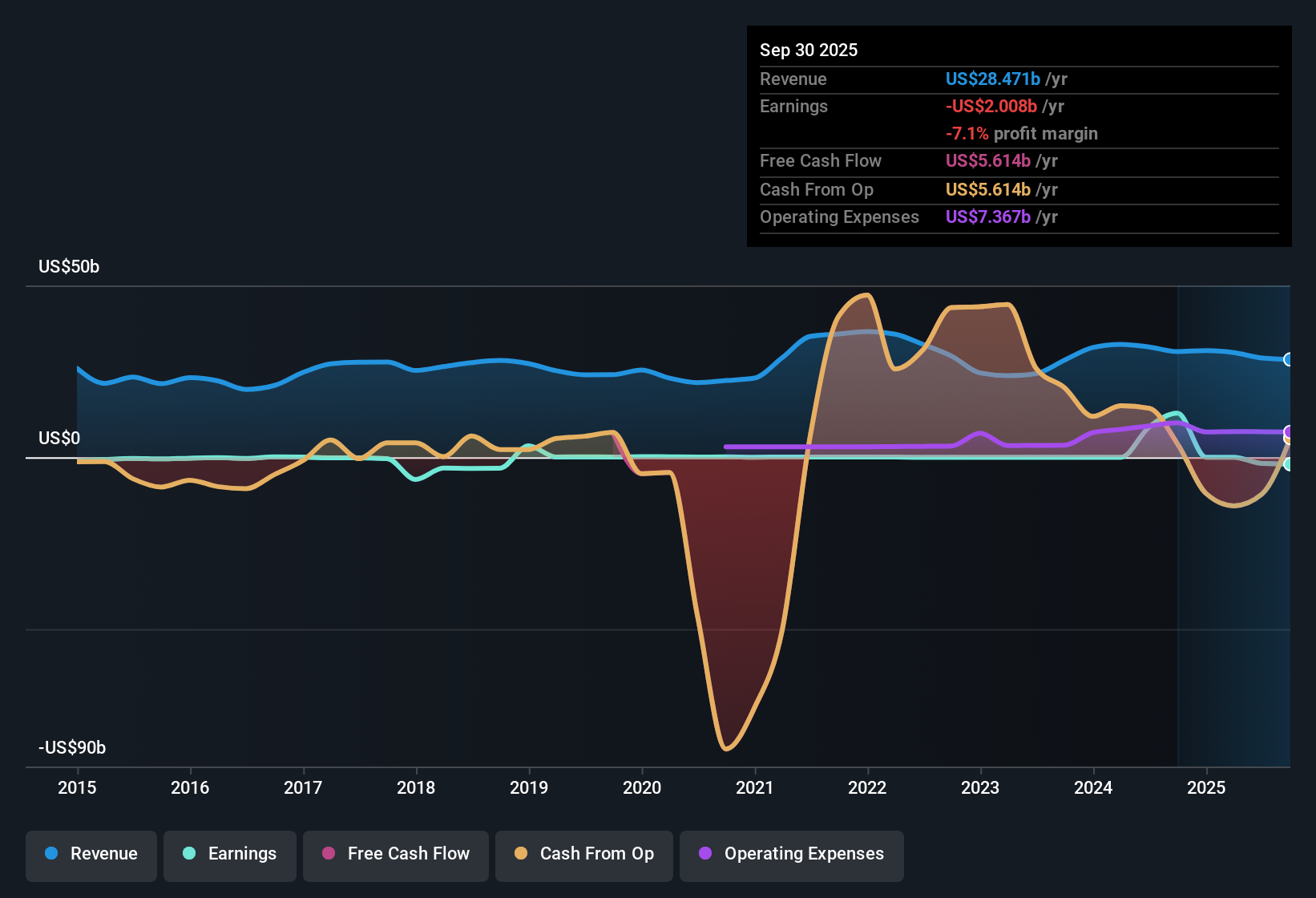

Federal National Mortgage Association (FNMA) has just posted its FY 2025 third quarter numbers, with revenue of US$7.0b and EPS of US$0.66 setting the tone for the latest update.

Over recent quarters, revenue has moved from US$8.0b in FY 2024 Q2 to US$7.4b in Q3 and US$7.8b in Q4, then to US$7.2b in FY 2025 Q1, US$6.5b in Q2 and US$7.0b in Q3. EPS has ranged from US$1.50 in FY 2024 Q2 and US$0.69 in Q3 to close to zero in late 2024 and early 2025, before landing at US$1.19 in FY 2025 Q2 and US$0.66 in Q3. With that backdrop, investors are likely to focus on how consistently FNMA can convert this revenue base into sustainable margins across the cycle.

See our full analysis for Federal National Mortgage Association.With the headline numbers on the table, the next step is to see how this earnings print lines up with the dominant narratives around FNMA, highlighting where the data supports the story and where it pushes back against it.

US$3.9b profit this time, but still a trailing loss

- FNMA earned US$3.9b of net income in FY 2025 Q3 and US$7.0b of revenue, yet the latest trailing 12 month data still shows a total net loss of US$2.0b on US$28.5b of revenue.

- What stands out against a cautious, more bearish view is that recent quarters swing between very small profits in late 2024 and early 2025 and large profits like US$7.0b of net income in FY 2025 Q2. This means headline losses over the year sit alongside periods of strong profitability.

- Critics highlight that the company is currently unprofitable over the trailing year, yet the five year track record shows losses shrinking at about 34% a year, so the picture is more mixed than a simple loss label suggests.

- Bears also focus on risk, but the pattern of quarters ranging from US$3 million and US$6 million in net income up to US$8.8b and US$7.0b shows earnings power that does not fit a simple persistent loss story.

EPS swings from near zero to US$1.19

- Across the last six quarters, Basic EPS has ranged from close to zero in FY 2024 Q4 and FY 2025 Q1 to US$1.50 in FY 2024 Q2 and US$1.19 in FY 2025 Q2, with the latest quarter at about US$0.66.

- For a more cautious, bearish narrative that worries about earnings quality, these EPS swings show that results can move sharply from almost flat earnings to multi dollar per share quarters. Any simple story that earnings are either consistently strong or consistently weak is challenged by the sequence of US$0.00, US$0.00, US$0.00, US$0.69, US$1.19 and US$0.66 prints.

Value case meets balance sheet risk

- On valuation, FNMA trades at US$8.31 per share, which is below a DCF fair value estimate of about US$12.52 and on a P/S of 1.7x versus 2.4x for the broader US Diversified Financial industry and 3.8x for peers, while trailing 12 month net income is a loss of US$2.0b.

- What is interesting for a bullish angle is that the apparent value gap, roughly 33.6% below DCF fair value and a lower P/S than industry and peers, sits alongside concrete balance sheet concerns, since debt is reported as not well covered by operating cash flow. The reward story is therefore directly linked to a material funding risk rather than occurring in isolation.

- Supporters may point to the discount to the US$12.52 DCF fair value and the below peer P/S as evidence that the market is pricing in a lot of caution, yet the trailing loss and weak cash flow coverage of debt show why that discount exists.

- For you as an investor, that means the valuation and risk signals are pulling in different directions, and the key question is how comfortable you are with a company that looks cheap on sales and DCF while still carrying a recent loss and debt coverage pressure.

If you want to see how others connect these earnings swings, valuation signals, and risks into a single story, you can read a full narrative built around FNMA here: 📊 Read the full Federal National Mortgage Association Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Federal National Mortgage Association's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

FNMA's trailing 12 month loss, volatile EPS and pressure on debt coverage all point to meaningful balance sheet risk that some investors may find uncomfortable.

If that level of uncertainty feels a bit much, shift your focus toward companies with stronger financial footing and use our solid balance sheet and fundamentals stocks screener (45 results) to quickly spot ideas with sturdier balance sheets and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.