Fastenal (FAST) Extends Key Credit Facilities, Is The Stock Already Fully Valued?

Fastenal Company FAST | 0.00 |

Why Fastenal’s Latest Financing Moves Matter For Investors

Fastenal (FAST) has just overhauled its main revolving credit facility and Master Note Agreement, extending access to capital, revising covenants, and adjusting borrowing limits in ways that reshape its financial toolkit.

These financing changes sit alongside the recent addition of FedEx executive Vishal Talwar to Fastenal’s board, giving investors fresh information about both the company’s balance sheet flexibility and its governance bench at the same time.

Fastenal’s recent credit agreements and board appointment come as the stock trades at US$46.26, with a 1-month share price return of 5.28% and a 1-year total shareholder return of 14.86%, indicating momentum that has built steadily over recent years.

If this kind of steady progress has your attention, it may be a suitable moment to widen your watchlist and see what else fits your criteria through the 20 top founder-led companies

Fastenal’s decades of industrial supply experience, recent 1 year total return of 14.86%, and only slight discount of about 1% to the average analyst price target raise a key question for investors: is there still a genuine buying opportunity here, or is the market already pricing in much of the future growth?

Most Popular Narrative: 1% Undervalued

The most followed narrative currently pegs Fastenal’s fair value at $46.49, which sits only slightly above the last close at $46.26, indicating a tightly balanced valuation.

The analysts have a consensus price target of $46.49 for Fastenal based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0, and the most bearish reporting a price target of just $39.9.

Want to see what is backing that finely tuned fair value for Fastenal? The narrative leans on specific revenue growth, margin expansion and a premium future earnings multiple. Curious which assumptions really carry the weight here? The full story brings those threads together into a single valuation blueprint.

Result: Fair Value of $46.49 (UNDERVALUED)

However, Fastenal’s story still carries some tension, with higher inventory levels tying up cash and ongoing tariff and freight pressures threatening to squeeze margins if conditions change.

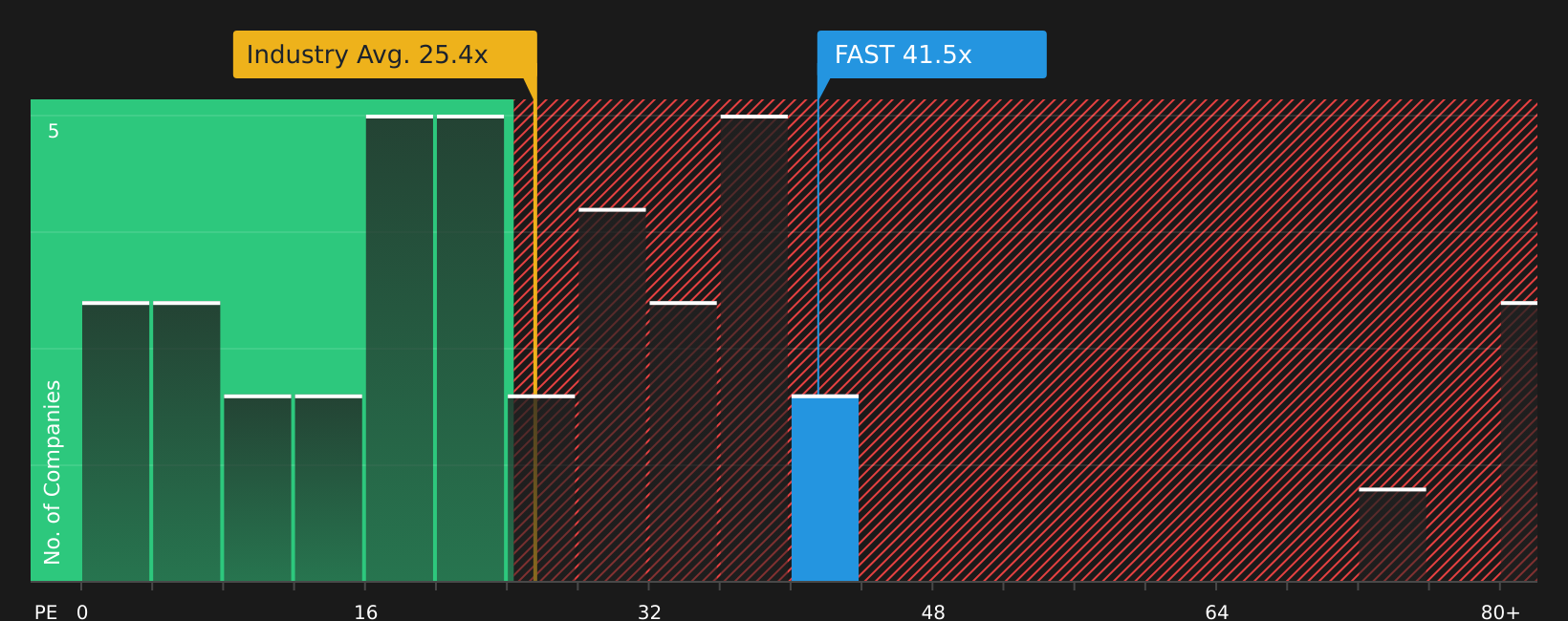

Another View: Fastenal Looks Expensive On Earnings Multiples

The earlier narrative framed Fastenal as roughly 1% undervalued against a fair value of about $46.49, but the earnings multiple tells a different story. At a P/E of 40.9x, Fastenal trades well above the US Trade Distributors industry at 24.7x and its own fair ratio of 28.4x. This suggests less room for error if growth or margins do not match expectations.

For investors, the gap between the current P/E and that fair ratio implies that even small disappointments in earnings or cash generation could hit the share price harder than for lower rated peers. The key question is whether Fastenal’s execution quality and balance sheet justify paying that kind of premium.

Next Steps

Given the mixed signals around Fastenal’s valuation and growth expectations, it makes sense to look at the underlying data yourself and decide quickly which side you lean toward by weighing the 2 key rewards and 1 important warning sign.

Looking For More Investment Ideas Beyond Fastenal?

If Fastenal has sharpened your focus, do not stop here. Broaden your watchlist now so you do not miss other compelling opportunities shaping up.

- Spot potential value setups early by checking companies featured in the screener containing 18 high quality undiscovered gems.

- Strengthen your downside protection by reviewing the 69 resilient stocks with low risk scores that score well on resilience.

- Target financial robustness by scanning stocks in the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.