Fastenal (FAST) Valuation Check As Supply Chain Push And Q1 2026 Margins Support Investor Optimism

Fastenal Company FAST | 0.00 |

Fastenal (FAST) is back in focus after Q1 2026 results highlighted operating leverage and margin expansion, putting fresh attention on its push into embedded supply-chain services and digital inventory tools for large customers.

The Q1 2026 update comes after a steady year, with the share price up 13.75% year to date and a 1 year total shareholder return of 11.47%. The 3 year total shareholder return of 79.33% points to stronger longer term momentum.

If Fastenal's shift toward embedded supply chains has you thinking about where else infrastructure heavy investing could lead, it might be worth scanning 35 power grid technology and infrastructure stocks

With Fastenal trading close to recent analyst targets and showing solid recent returns, the real question now is simple: are you looking at a relatively fully priced compounder, or is the market underestimating its embedded supply chain push?

Most Popular Narrative: 1.1% Undervalued

Fastenal's most followed narrative pegs fair value at $46.49, almost on top of the $46 last close. This puts the focus squarely on execution rather than a valuation gap.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains.

Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Interested in how a high margin distributor might perform when it leans further into embedded inventory technology and a larger digital mix, and what that could mean for earnings power and valuation multiples over time? The full narrative outlines the growth rates, margin assumptions, and P/E levels used to support that fair value estimate.

Result: Fair Value of $46.49 (ABOUT RIGHT)

However, there is still clear risk here, especially if trade tensions raise sourcing costs or if digital competitors pull smaller customers away more quickly than Fastenal can adapt.

Another View: High Multiple, Different Message

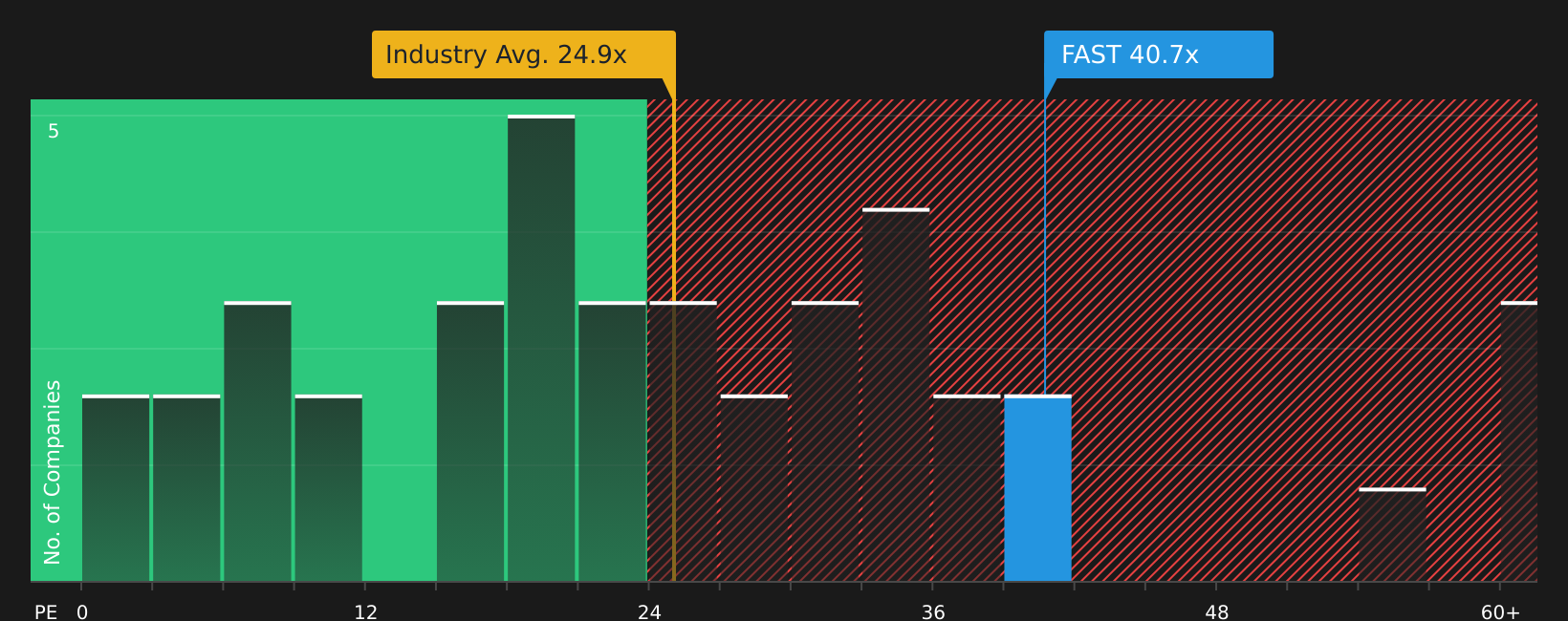

While the fair value narrative comes out close to Fastenal's $46.00 share price, the P/E tells a tougher story. At 40.6x, it sits well above the US Trade Distributors industry at 24.8x, peers at 25.5x, and a fair ratio of 28.5x. That gap points to real valuation risk if expectations slip. How comfortable are you paying this premium?

Next Steps

If the mixed messages on valuation and growth are leaving you undecided, it helps to review the numbers yourself and stress test the key assumptions. To weigh both the upside and the risks before you act, start with the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Fastenal has sharpened your thinking, do not stop there. Use the tools available to widen your opportunity set before the market moves ahead of you.

- Target potential mispricings by scanning a focused list of companies on the 47 high quality undervalued stocks that match strong fundamentals with appealing valuations.

- Prioritize resilience and stay on the front foot by reviewing companies highlighted in the 62 resilient stocks with low risk scores that score well on financial and risk checks.

- Get ahead of the crowd by searching for underfollowed opportunities through the screener containing 21 high quality undiscovered gems before they appear on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.