FB Financial And 2 Other Stocks That May Be Trading Below Their Estimated Value

Everpure, Inc. Class A P | 0.00 |

Over the last 7 days, the United States market has risen by 1.6%, contributing to a 19% increase over the past year, with earnings expected to grow by 18% annually in the coming years. In such an environment, identifying stocks that may be trading below their estimated value can offer investors potential opportunities for growth and stability amidst these positive market trends.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Rayonier (RYN) | $21.49 | $42.86 | 49.9% |

| Q2 Holdings (QTWO) | $52.63 | $103.09 | 48.9% |

| Procore Technologies (PCOR) | $43.97 | $86.98 | 49.4% |

| Natera (NTRA) | $279.32 | $554.60 | 49.6% |

| Klaviyo (KVYO) | $16.90 | $33.62 | 49.7% |

| Janus Living (JAN) | $29.12 | $57.58 | 49.4% |

| Gold Royalty (GROY) | $2.86 | $5.69 | 49.7% |

| Esquire Financial Holdings (ESQ) | $120.34 | $238.84 | 49.6% |

| Beacon Financial (BBT) | $30.22 | $60.42 | 50% |

| Amaroq (AMRQ.F) | $1.112 | $2.21 | 49.8% |

We're going to check out a few of the best picks from our screener tool.

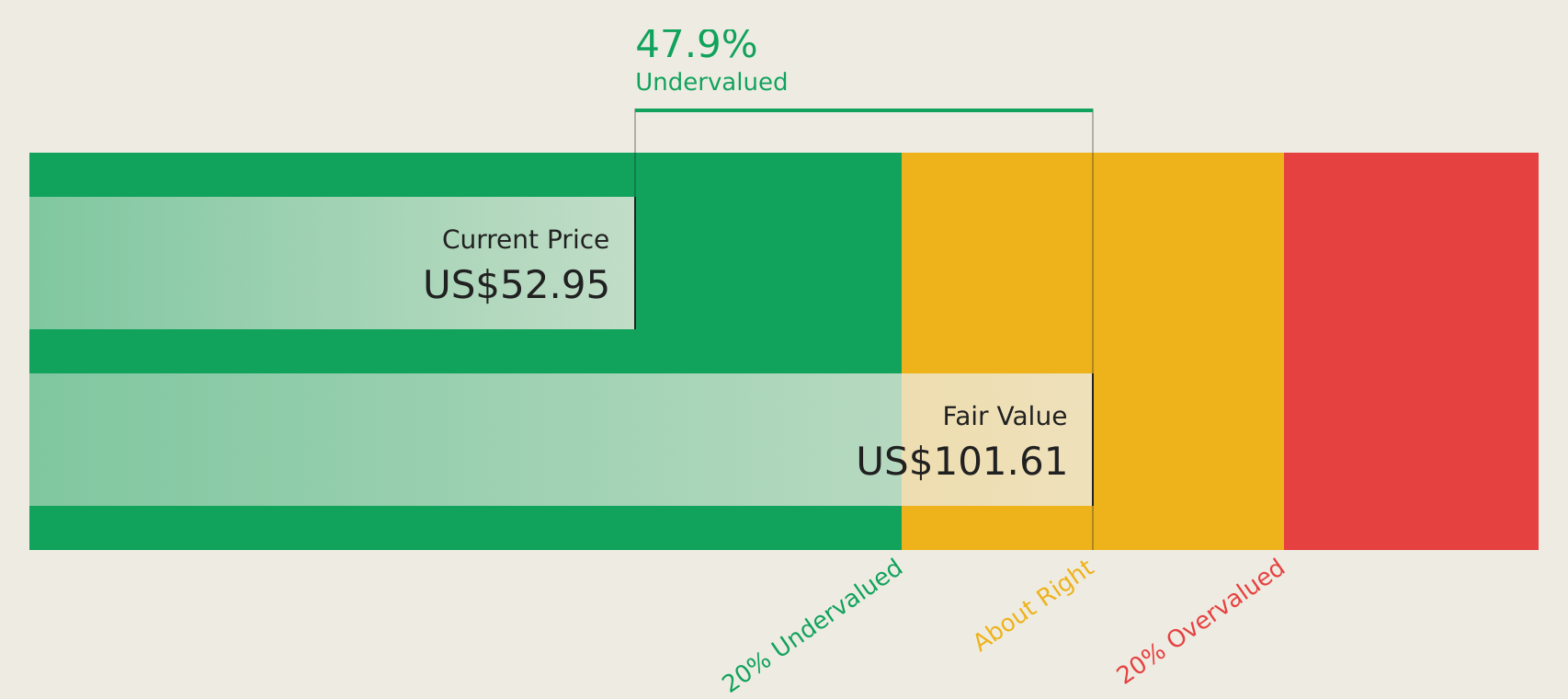

FB Financial (FBK)

Overview: FB Financial Corporation, with a market cap of $2.88 billion, operates as a bank holding company for FirstBank offering a range of commercial and consumer banking services.

Operations: The company generates revenue through its banking segment, which contributes $500.55 million, and its mortgage segment, which adds $57.12 million.

Estimated Discount To Fair Value: 44.9%

FB Financial appears undervalued, trading at 44.9% below its fair value estimate and more than 20% below future cash flow value. The company reported strong Q1 results with net interest income of US$145.97 million and net income of US$57.53 million, reflecting significant growth from the previous year. Despite a recent share repurchase program worth up to US$175 million, FB Financial's earnings are forecast to grow significantly at 30.2% annually, outpacing the broader U.S. market growth rate.

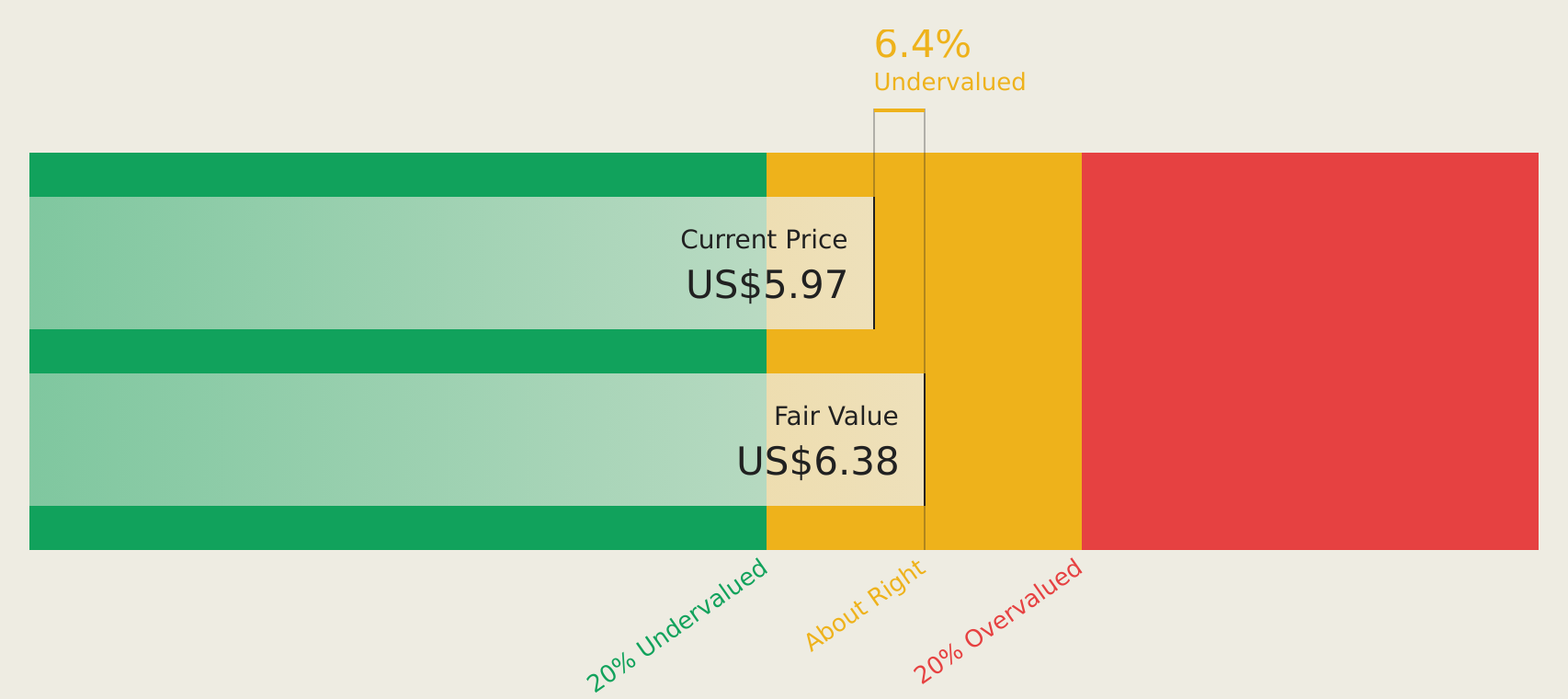

Jumia Technologies (JMIA)

Overview: Jumia Technologies AG operates an e-commerce platform across various regions including Africa, Europe, and the United Arab Emirates, with a market cap of approximately $873.16 million.

Operations: The company's revenue is primarily derived from its e-commerce platform, which generated $203.23 million.

Estimated Discount To Fair Value: 42%

Jumia Technologies is trading at US$7.05, significantly below its estimated future cash flow value of US$12.16, suggesting it may be undervalued based on cash flows. Despite a net loss of US$17.73 million in Q1 2026, the company reported sales growth to US$50.56 million from the previous year and is expected to become profitable within three years with earnings projected to grow 96.92% annually, outpacing market averages.

Everpure (P)

Overview: Everpure, Inc. offers data storage and management technologies, products, and services both in the United States and internationally with a market cap of $24.17 billion.

Operations: The company generates revenue from its Computer Storage Devices segment, amounting to $3.94 billion.

Estimated Discount To Fair Value: 46.2%

Everpure is trading at US$72.71, well below its estimated future cash flow value of US$135.13, highlighting potential undervaluation based on cash flows. Despite being dropped from several Russell indices recently, the company has shown strong financial performance with a Q1 2026 net income of US$24.08 million compared to a loss last year and forecasts earnings growth of 28.4% annually, outpacing market averages while maintaining robust strategic alliances and product innovations in AI and data resilience sectors.

Make It Happen

- Embark on your investment journey to our 149 Undervalued US Stocks Based On Cash Flows selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.