Fed Cuts Rates, But Powell Issues a Major Warning. Is the December Cut Canceled?

ETF-S&P 500 SPY | 650.34 | +2.91% |

PowerShares QQQ Trust,Series 1 QQQ | 577.18 | +3.39% |

ETF-Dow Jones Industrial Average DIA | 463.19 | +2.46% |

Roundhill Daily 2X Long Magnificent Seven ETF MAGX | 42.73 | +9.45% |

PHLX Sox Semiconductor Sector Ishares SOXX | 328.66 | +6.09% |

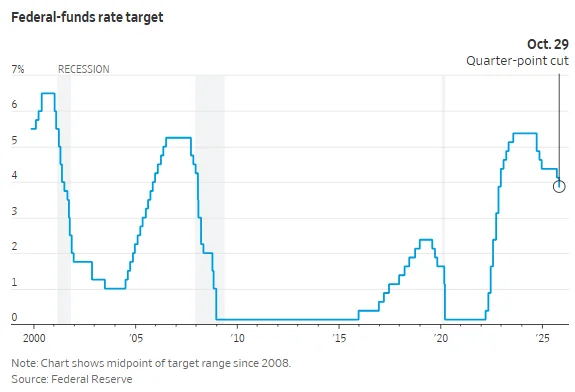

The Federal Reserve’s October policy meeting delivered the 25-basis-point rate cut the market expected, but it was Chairman Jerome Powell’s press conference that sent the real shockwave.

While the cut lowers the benchmark rate to a 3.75%-4.00% range, Powell adopted an "aggressively" hawkish tone, issuing an unusually direct challenge to investors betting on another cut in December.

His four most impactful words—"far from certain"—instantly reset market expectations and signaled that the "easiest phase" of rate reversals may be over.1

For investors, parsing the conflicting signals from this meeting is crucial. Here are the five key takeaways and what top Wall Street analysts are saying.

Decoding the Fed’s Message: The Five Key Takeaways

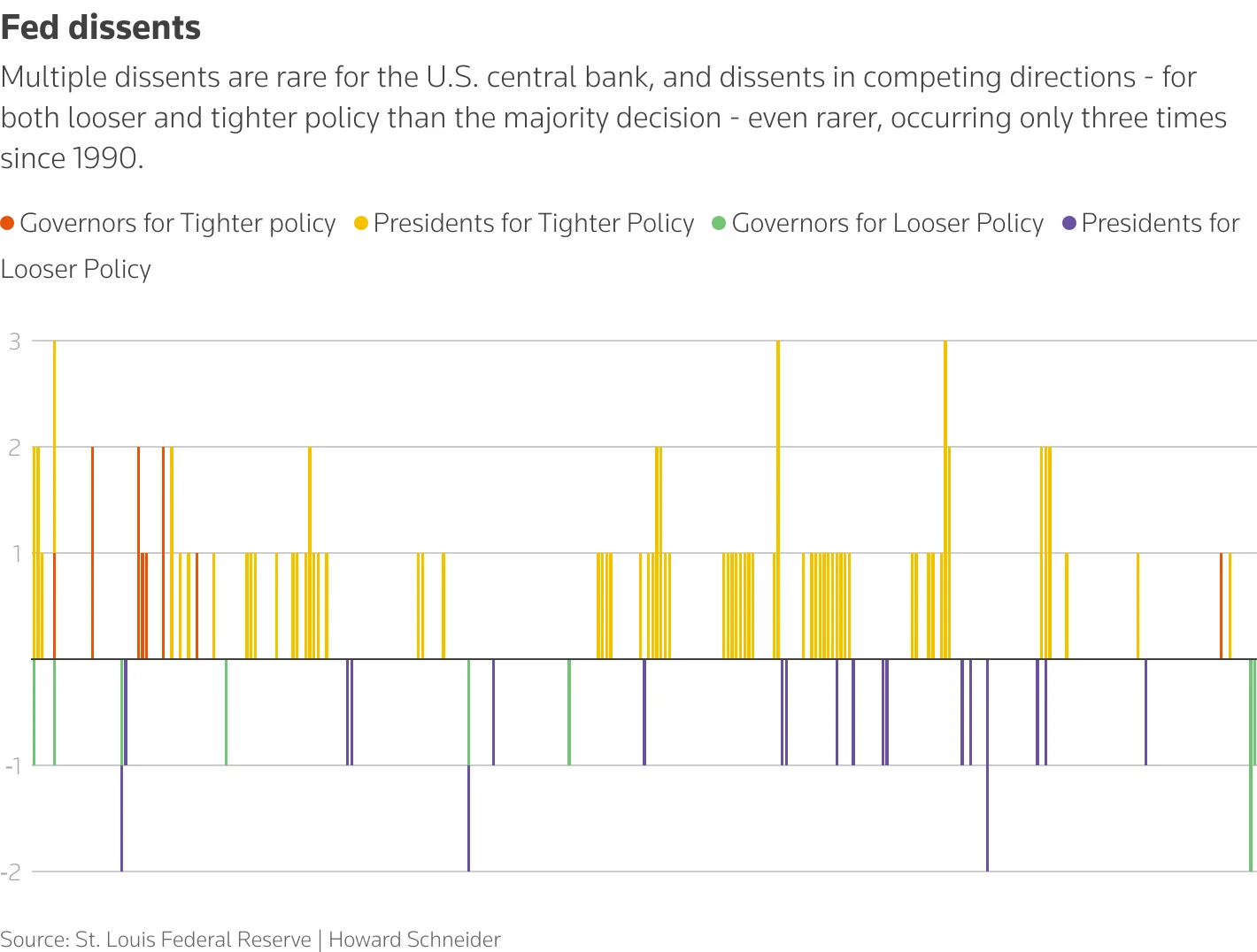

1. A Deeply Divided House

The 25-basis-point cut passed, but not without significant internal division. Two voting members dissented in opposite directions—a rare event signaling deep fractures within the FOMC.

- Dovish Dissent: Governor Milane (a Trump appointee) argued for a larger 50-basis-point cut.

- Hawkish Dissent: Kansas City Fed President Schmid argued for no cut at all, fearing easing could undermine the inflation fight.

This marks only the third time since 1990 that policymakers have dissented in opposing directions, highlighting major disagreement on the economic outlook.

2. Powell's Big Pushback on December

Before the meeting, markets had priced in a 90% probability of a December cut. Powell took direct aim at this assumption. "A further reduction in policy rates at the December meeting is far from a done deal," he stated, noting "widely differing views" among the 19 members. He stressed that the risk-management logic used for the September and October cuts would not necessarily apply going forward.

3. Quantitative Tightening (QT) Officially Ends

As speculated, the Fed is ending its balance sheet reduction, but it provided a firm date: December 1. This halts the three-and-a-half-year effort to shrink its $6.6 trillion balance sheet.5 The Fed will now reinvest principal payments from mortgage-backed securities into short-term Treasuries, a technical move Powell described as tilting the balance sheet toward a shorter duration.

4. The Inflation and Tariff Question

Powell hinted that inflation is returning toward the 2% target, but acknowledged it remains elevated (the core PCE index is at 2.8%). Regarding tariffs, he reiterated the Fed’s baseline assumption that their impact on inflation will be "temporary" and a "one-time" hit, rather than a lasting trend.

5. The "Data Vacuum" (Government Shutdown)

Powell acknowledged the government shutdown has created uncertainty and delayed key data. However, he suggested that existing public and private data indicate the economic outlook hasn't significantly changed: the economy is expanding moderately, the labor market is cooling, and inflation remains slightly elevated.

Wall Street is Split: The Great December Debate

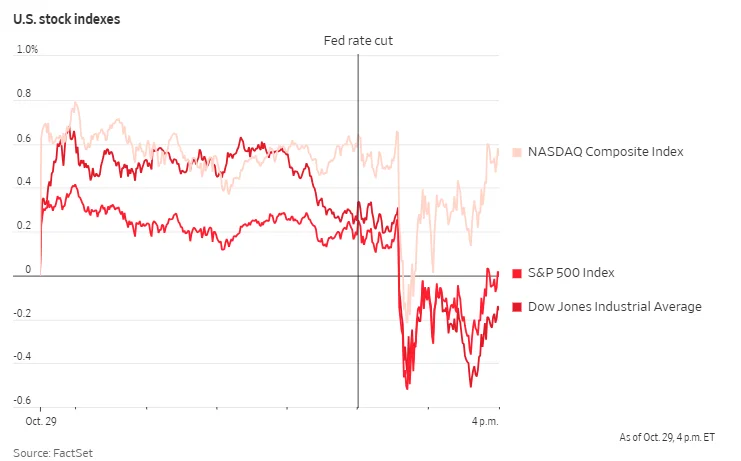

Financial markets reacted instantly to Powell’s hawkish pivot.

- Stocks: The S&P 500 index(SPX.US) briefly fell sharply before staging a rebound to close flat.

- Bonds: U.S. Treasury yields rose, with the 10-year yield hitting its highest level since October 10, closing at 4.07%.

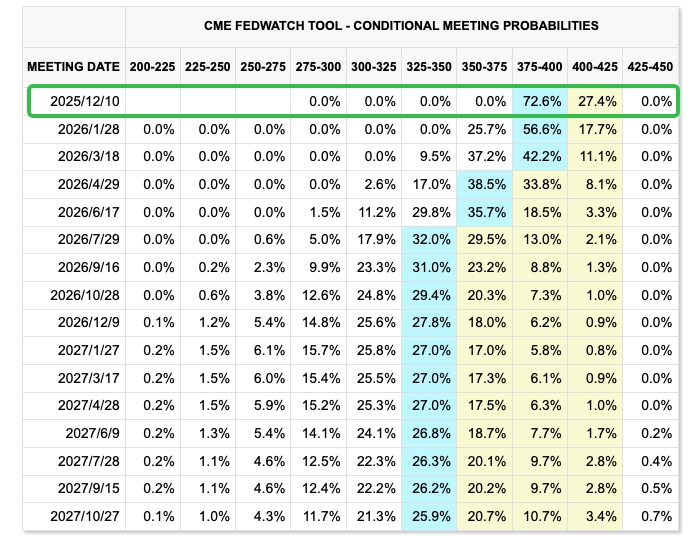

- Fed Futures: According to the CME FedWatch Tool, traders slashed the probability of a December rate cut from nearly 90% down to roughly 73%. Traders heard Powell, but still lean slightly toward a cut.

Here is how top analysts and investors are interpreting the new landscape:

The "Don't Count on It" Camp

- Dan North (Allianz): "He (Powell) has dealt a blow to the market’s expectations of a December rate cut like a WWE wrestler. While the door isn’t completely shut... Powell strongly signaled otherwise: ‘Don’t count on it.’"

- Michael Rosen (Angeles Investments): "Powell’s comments have tempered market expectations... reflecting tensions within the Fed over additional easing amid persistently high inflation that remains above its own target."9

- Adam Button (InvestingLive): "Schmidt’s dissent was hawkish, reflecting the sentiment of some Fed officials, so Powell may face some pressure to temper market pricing for a December rate cut."

The "Strictly Data-Dependent" Camp

- Jason Pride (Glenmede): "The weakness in the labor market and the risk of inflation triggered by tariffs leave no clear playbook for the future. Future policy decisions are far from preordained and are highly data-dependent."

- Oliver Pursche (Wealthspire Advisors): "Chairman Powell indicated that another rate cut in December is not a done deal.10 But no rate cut is ever a done deal. To me, this is not an inappropriate statement. The Fed always bases its decisions on data."

- Jeffrey Gundlach (DoubleLine Capital): The "New Bond King" noted that U.S. inflation is likely to remain above 3% and that the odds of a December rate cut are "fifty-fifty."11

The "Cut is Still Coming" Camp

- Jeffrey Roach (LPL Financial): Some analysts remain focused on the economy, not just Powell's words. Roach believes that "downside risks in the job market will likely lead the Fed to continue cutting rates in December and into next year."

For investors, the key takeaway is that the Fed is no longer on autopilot. The 25-basis-point cut is history; the real story is the profound uncertainty Powell has injected into the market, making every piece of economic data between now and December critical.