FedEx (FDX) Valuation Check As ServiceNow Partnership Puts Dataworks Logistics Intelligence In Spotlight

FedEx Corporation FDX | 0.00 |

FedEx (FDX) is back in focus after expanding its work with ServiceNow to plug FedEx Dataworks logistics intelligence directly into ServiceNow’s procurement and supply chain platforms, creating data driven supplier and workflow tools.

Despite a 6.8% decline in the 7 day share price return and a small pullback today to US$375.93, FedEx still shows a 5.3% 30 day share price return and a 75.3% 1 year total shareholder return, which suggests that recent momentum remains intact even as investors weigh the ServiceNow partnership and prior gains.

If you like the logistics and automation angle of FedEx’s Dataworks partnership, you may want to broaden your search and check out 32 robotics and automation stocks

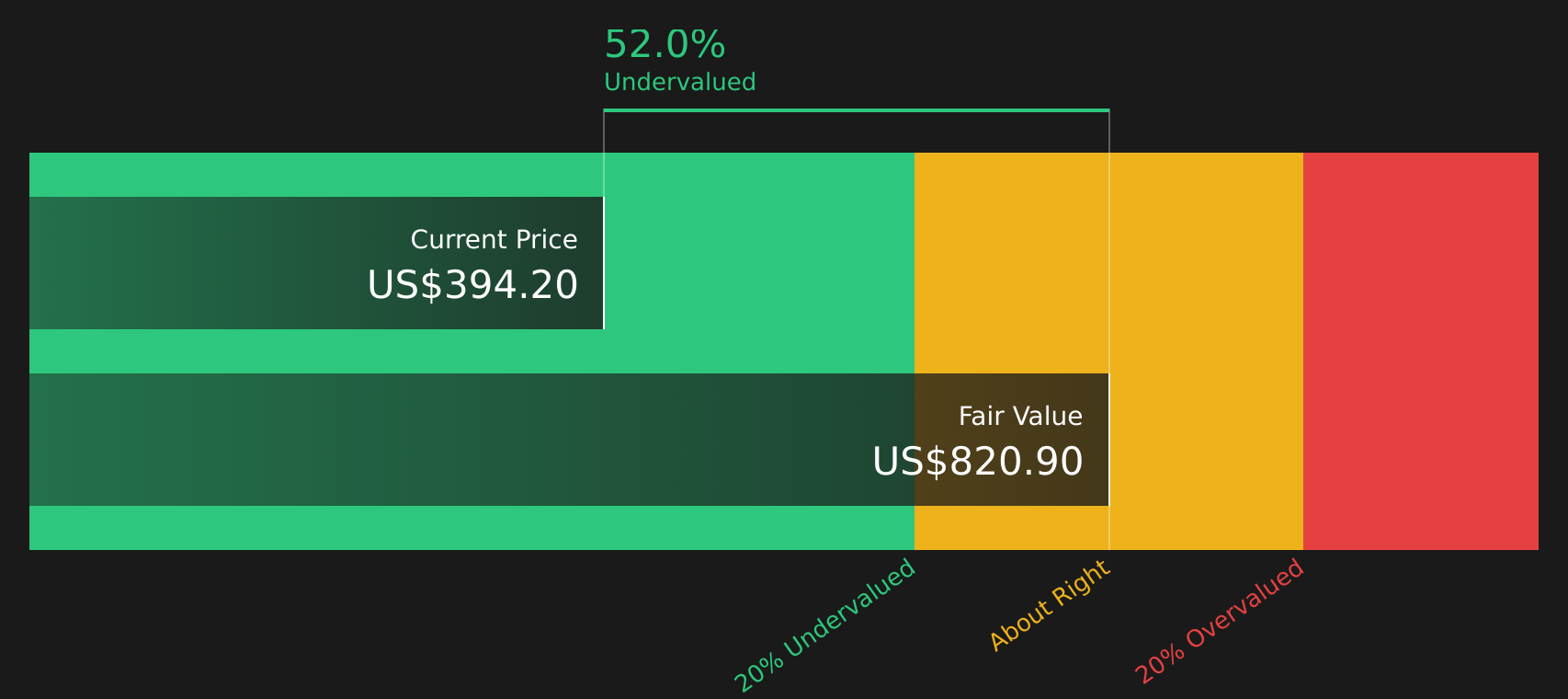

With FedEx trading at US$375.93, carrying a value score of 4 and a modeled intrinsic value gap of about 54%, the key question is simple: is this still a mispriced logistics giant, or is the market already baking in future growth?

Most Popular Narrative: 6.5% Undervalued

FedEx's most followed narrative pegs fair value at about $401.89, a touch above the last close at $375.93. This frames a modest undervaluation built on execution gains and network changes.

The Network 2.0 project aims to optimize 50 U.S. stations, streamlining operations to improve efficiency. By enabling about 12% of FedEx's daily global volume to flow through optimized facilities by the end of FY '25, this initiative should positively impact operating margins and earnings.

Curious what kind of revenue ramp, margin lift, and future earnings multiple need to line up to support that fair value? The narrative ties them together in a tight financial roadmap, with one core assumption doing most of the heavy lifting.

Result: Fair Value of $401.89 (UNDERVALUED)

However, the picture can change quickly if the USPS contract loss, weaker industrial demand, or freight separation costs hit volumes and margins harder than analysts expect.

Another Lens On Valuation

The analyst narrative relies on earnings forecasts and a P/E of about 21.8x in 2029. In contrast, the SWS DCF model points to a higher estimate, with an inferred future cash flow value of $815.83 per share compared with the current $375.93. This suggests FedEx may be trading below its estimated cash flow value. Which signal do you weigh more heavily: a richer long term cash flow view or a tighter near term multiple?

Next Steps

With sentiment split between the upside case and those contract and demand worries, it makes sense to move quickly and look through the numbers yourself so you can decide where you stand on the 4 key rewards and 2 important warning signs

Ready to hunt for your next idea?

If FedEx has you thinking more broadly about opportunities, use the screener to quickly surface stocks that match the mix of quality, value, and resilience you care about.

- Target potential mispricings across the market by scanning a curated set of 51 high quality undervalued stocks that combine solid fundamentals with room for market sentiment to catch up.

- Prioritise strength and staying power by zeroing in on companies filtered through the solid balance sheet and fundamentals stocks screener (44 results) so you focus on those with sturdier financial footing.

- Spot under the radar opportunities before the crowd by working through a screener containing 23 high quality undiscovered gems that highlights quality stocks many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.