First Busey (BUSE) After Its New Strategy Chief Appointment Looks Fairly Valued

First Busey Corporation BUSE | 0.00 |

New strategy chief puts recent leadership moves at First Busey in focus

First Busey (BUSE) has appointed Mike Daley as chief strategy officer after he led Finance & Business Line Strategy during the bank's integration with CrossFirst Bank last year, putting its leadership approach in the spotlight for investors.

Beyond this leadership change, First Busey’s recent 7.5% 1 month share price return and 24.1% year to date share price return, alongside a 63.97% 3 year total shareholder return, point to momentum that has been building over time.

If you are weighing what to watch next in financials and beyond, it could be a good moment to broaden your search through 20 top founder-led companies

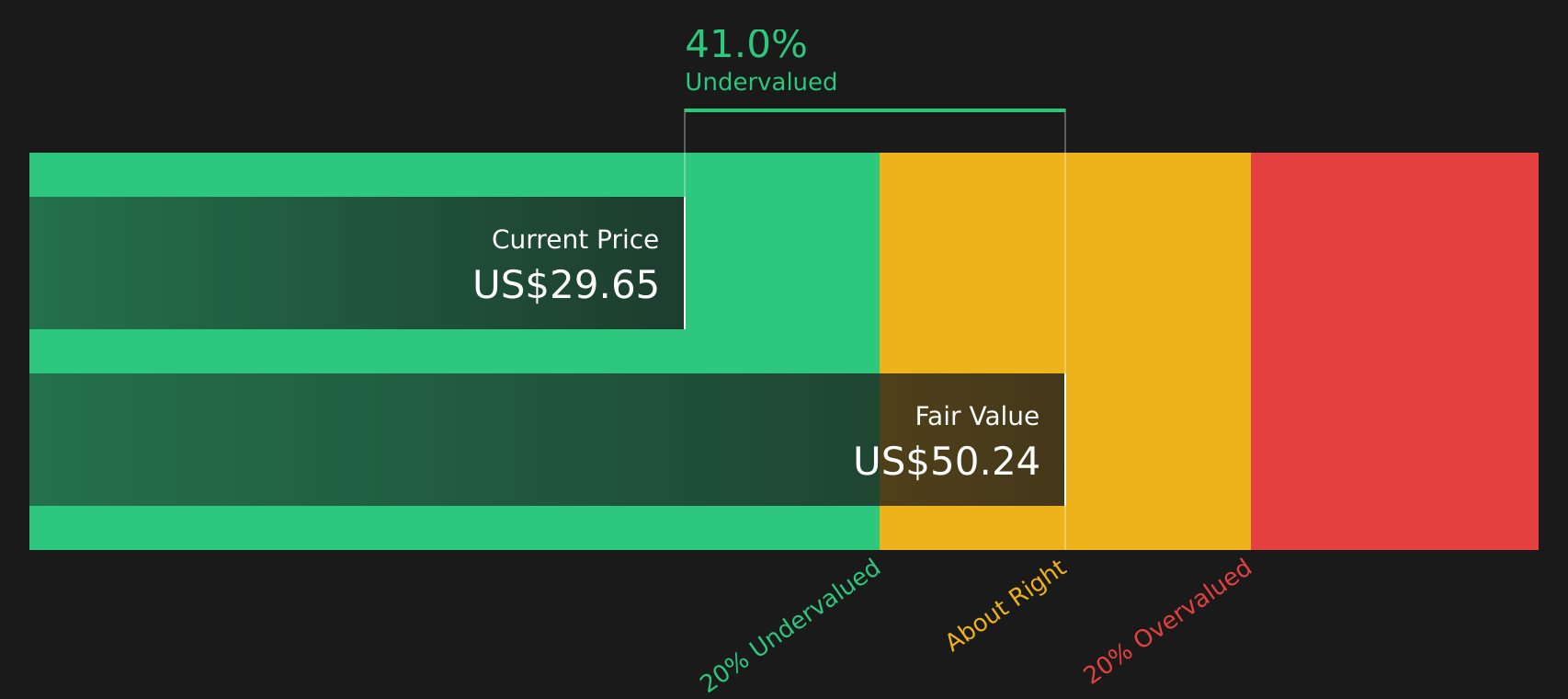

With First Busey trading at US$29.65, only about 1.7% below the consensus price target but at an indicated intrinsic discount of roughly 41%, investors are left asking: is there real upside here, or is the market already pricing in future growth?

Price-to-Earnings of 12.5x: Is it justified for First Busey?

On a P/E basis, First Busey trades on 12.5x earnings, which sits slightly above the US Banks industry average of 12.2x and close to the estimated fair P/E of 12.2x, so investors are looking at a valuation that leans mildly rich rather than clearly cheap.

The P/E ratio compares the company’s share price to its earnings per share and is a common way to see how much investors are paying for each dollar of profit. For a bank like First Busey, where earnings, return on equity and balance sheet strength matter a lot, this multiple is one quick way to see how expectations line up with current profitability.

Here, the signals are mixed. On one side, First Busey is flagged as expensive versus both the US Banks industry average P/E of 12.2x and the estimated fair P/E of 12.2x, which suggests the market is asking a small premium relative to both peers and a regression based fair ratio that the market could move towards over time. On the other side, First Busey is described as good value when compared with a broader peer group average P/E of 14.4x, pointing to some relative appeal if you widen the comparison set beyond the immediate industry.

That tension is important. If the market eventually leans toward the lower industry or fair P/E levels, there could be pressure on the multiple. In contrast, alignment with the higher peer group average would argue that the current 12.5x is not stretched in that wider context. Understanding which reference point matters most for your own portfolio construction is key before leaning too heavily on a single P/E snapshot.

Result: Price-to-Earnings of 12.5x (ABOUT RIGHT)

However, investors in First Busey still need to watch for integration setbacks around the CrossFirst tie up, as well as any slowdown in revenue or net income growth at current levels.

Another view on First Busey’s value

While the P/E discussion paints First Busey as roughly in line with where the market might expect a bank stock to trade, the Simply Wall St DCF model points in a different direction. On that measure, First Busey at $29.65 is assessed as trading about 41% below an estimated fair value of $50.24.

That kind of gap suggests the P/E multiple may be missing something about the company’s cash flow profile, or that the DCF assumptions are more optimistic than current sentiment implies. Which lens do you trust more for your own process?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First Busey for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of leadership change and valuation tension around First Busey leaves you curious rather than convinced, consider acting while the data is fresh and testing the story against your own risk tolerance, starting with the 4 key rewards

Looking for more investment ideas beyond First Busey?

If you are serious about putting fresh capital to work, do not stop with First Busey. Use these focused stock lists to quickly surface new candidates.

- Target dependable income by scanning for companies in 7 dividend fortresses that may align with your yield goals and risk comfort.

- Spot potential mispricings by reviewing screener containing 18 high quality undiscovered gems before the wider market starts paying attention.

- Prioritise resilience by checking which businesses feature in the 74 resilient stocks with low risk scores and might fit a more defensive allocation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.