First National Bank Alaska (FBAK) Earnings Growth Outpaces Five Year Trend And Tests Valuation Debate

FIRST NATIONAL BANK ALASKA FBAK | 297.00 | -0.99% |

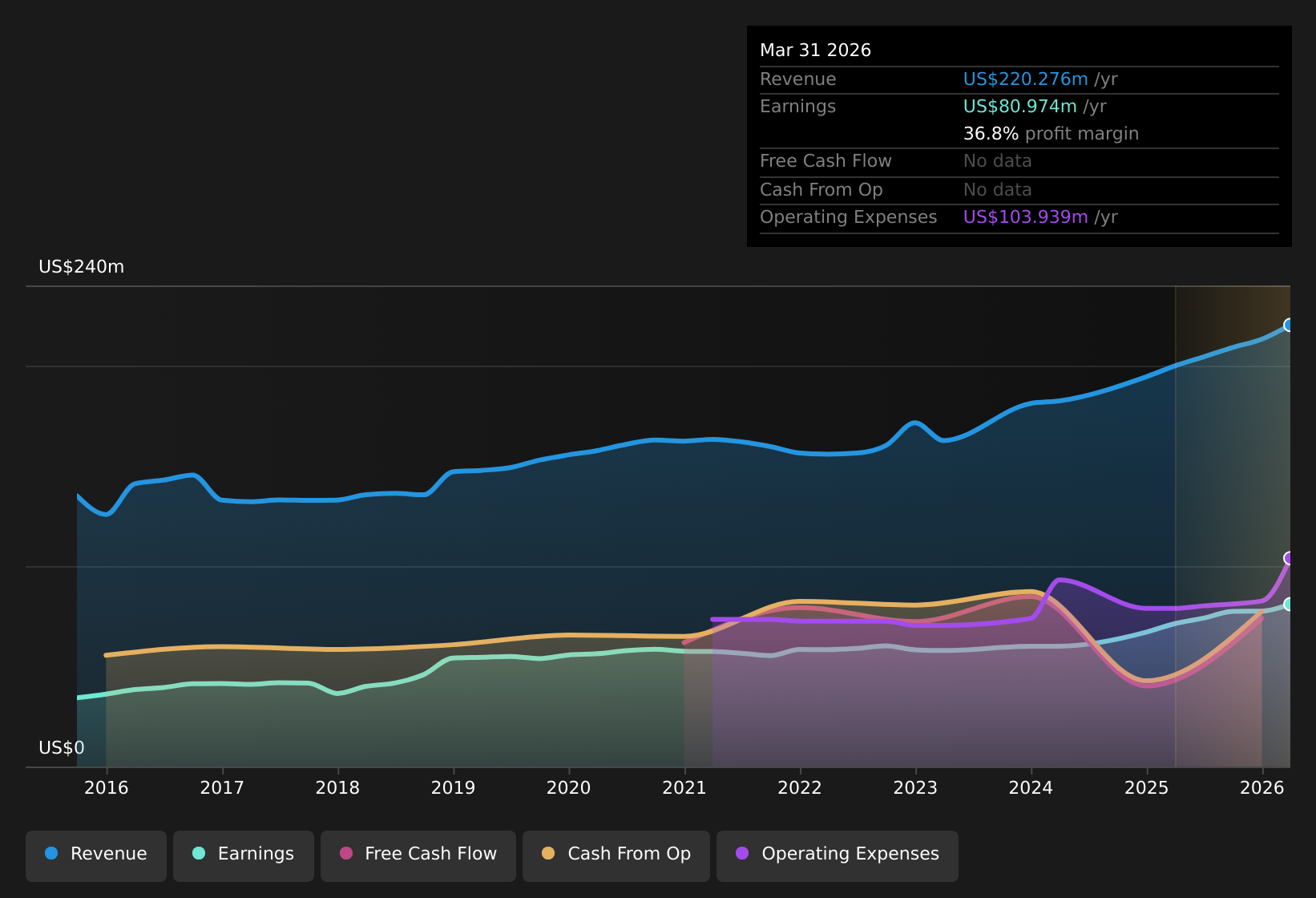

First National Bank Alaska (FBAK) has wrapped up FY 2025 with Q4 revenue of US$56.2 million, EPS of US$6.33 and net income of US$20.1 million, setting the tone for how investors read the full year. The bank has seen revenue move from US$52.2 million in Q4 2024 to US$56.2 million in Q4 2025, while trailing twelve month EPS sits at US$24.48 on net income of US$77.5 million, giving you a clear line of sight on how the top line is feeding into profitability. With a trailing net profit margin of 36.4% and year over year earnings growth of 15.6%, the latest release keeps the focus squarely on how effectively the bank is turning revenue into bottom line returns.

See our full analysis for First National Bank Alaska.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around growth, quality and risks that investors have been debating over the past year.

TTM earnings growth outpaces five year trend

- Over the trailing twelve months, net income is US$77.5 million on revenue of US$213.1 million, compared with US$67.0 million of net income and US$194.5 million of revenue in the prior twelve month period, while the five year earnings growth rate is 6.4% per year versus 15.6% in the last year.

- What stands out for a bullish view is that the recent 15.6% earnings growth sits above the 6.4% five year average, yet:

- TTM EPS of US$24.48 now reflects that step up, after sitting at US$21.17 a year earlier on a smaller profit base of US$67.0 million.

- Revenue over the same TTM window is US$213.1 million versus US$194.5 million previously, which lines up with the stronger earnings without suggesting any one off surge in the data you can see.

36.4% net profit margin underpins profitability story

- The bank reports a trailing twelve month net profit margin of 36.4% compared with 34.5% in the prior year, with Q4 2025 net income of US$20.1 million on revenue of US$56.2 million giving you a sense of how that margin shows up in a single quarter.

- Supporters of a bullish angle point to this margin profile as a sign the core franchise is holding its own, but the figures also show where the bar is set:

- Across FY 2025, quarterly net income moves between US$17.7 million and US$21.4 million while revenue ranges from US$49.3 million to US$56.2 million, so profitability is consistently sitting on a relatively high base.

- The Q1 2025 cost to income ratio of 49.7% and net interest margin of 3.63% are among the few detailed efficiency and spread datapoints disclosed, giving investors concrete inputs when they judge how sustainable a 36.4% net margin might be.

Valuation gap and richer P/E send mixed pricing signals

- The current share price of US$308.00 sits below the DCF fair value of US$382.11, implying roughly a 19.4% gap, while the P/E ratio of 12.6x is slightly above both peer and US Banks industry averages of around 12.0x and 11.9x.

- Critics looking at a more cautious or bearish angle highlight that this set of numbers gives a mixed message, and the data backs up why it is not a one way story:

- On one hand, the DCF fair value of US$382.11 suggests more value than the current US$308.00 price, which leans in favor of investors who rely on cash flow models.

- On the other hand, the modest P/E premium to peers and an unstable dividend record, flagged as a risk for income seekers, mean some investors may question how much weight to put on that DCF gap alone.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on First National Bank Alaska's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

While margins and earnings growth look solid, the richer 12.6x P/E and unstable dividend record leave income focused investors with unanswered questions about reliability.

If that dividend uncertainty gives you pause, use these 1777 dividend stocks with yields > 3% to quickly focus on companies targeting yields above 3% that may offer more consistent income profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.