First Solar (FSLR) Could Be 2% Above Fair Value On Tariff And AI Demand Optimism

First Solar, Inc. FSLR | 0.00 |

Recent analyst upgrades have put First Solar (FSLR) in focus after firms highlighted the company’s exposure to U.S. tariffs, strong utility-scale solar demand, solid margins, and an extensive contracted backlog tied to AI data center growth.

First Solar’s share price has cooled in the short term, with a 1-month share price return down 8% and a 7-day return down 3.6%. However, the 90-day share price return of 30.5% and 1-year total shareholder return of 59.6% still point to strong underlying momentum as investors weigh recent upgrades, tariff tailwinds, and AI related demand expectations.

If this AI fueled solar story has your attention, it could be a good moment to see what else is setting up in the sector with 49 AI infrastructure stocks

With First Solar trading close to analyst targets yet still carrying an intrinsic discount, and with brisk revenue and earnings growth, are investors looking at an undervalued AI infrastructure play, or has the market already priced in the next leg of growth?

Most Popular Narrative: 2% Overvalued

Based on the most followed narrative, First Solar’s fair value of $243.59 sits slightly below the latest close at $248.36, which frames a modest premium that analysts are trying to justify with policy and technology tailwinds.

Recent U.S. policy changes, specifically, strengthened incentives and tighter restrictions against foreign entities of concern (such as China) under the new reconciliation legislation, are boosting First Solar's competitive moat, supporting robust demand for domestically produced modules, and enabling the company to capture higher long-term contracted pricing, directly improving forward revenue visibility and gross margins.

Curious what assumptions sit behind that fair value for First Solar? The narrative leans heavily on projected margin strength, measured revenue growth and a lower future earnings multiple. The exact mix of those inputs is where the story gets interesting.

Result: Fair Value of $243.59 (OVERVALUED)

However, the First Solar narrative could still be knocked off course if trade policies shift against current tariff assumptions, or if aggressive low cost competitors pressure module pricing and margins.

Another View: First Solar Through the P/E Lens

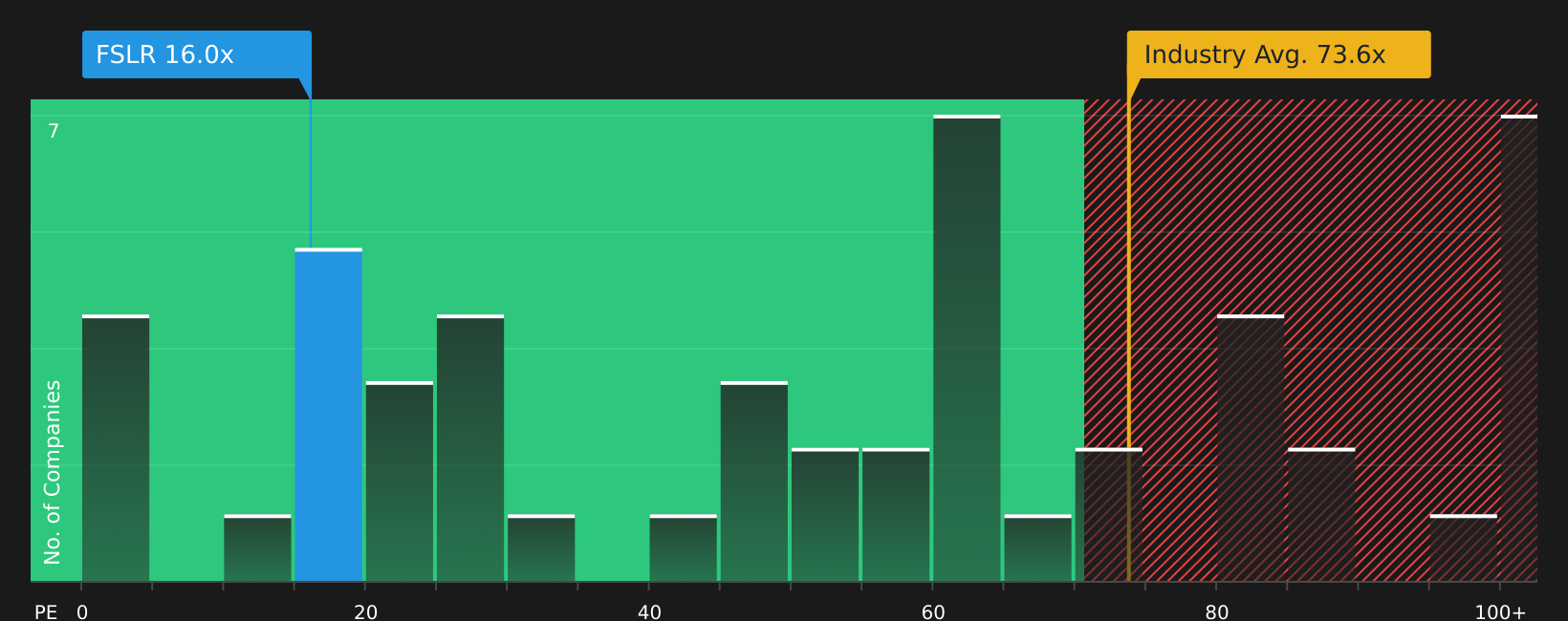

While the narrative driven fair value for First Solar suggests a small premium to $243.59, the market is currently pricing the stock at about 16x earnings, versus an estimated fair ratio of 41.9x and a US Semiconductor sector average of 70.5x. That wide gap suggests investors may be demanding a steep discount for policy and execution risk, so the key question is whether that caution is justified or overly harsh.

For a closer look at how this earnings multiple stacks up, and what it might mean if the market moves even part of the way toward the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment around First Solar clearly mixed, it helps to move quickly, test the assumptions for yourself, and weigh both risks and rewards before acting. To understand what the current optimism is based on, take a closer look at the 4 key rewards.

Looking for more investment ideas beyond First Solar?

If First Solar has sharpened your focus on where to put fresh capital, do not stop here. The best opportunities often sit just outside your current watchlist.

- Expand your hunt for mispriced opportunities by scanning 44 high quality undervalued stocks, where stronger fundamentals meet prices that may not fully reflect them yet.

- Strengthen your portfolio’s staying power by reviewing companies in the solid balance sheet and fundamentals stocks screener (48 results) that pair resilient finances with disciplined fundamentals.

- Get ahead of the crowd by tracking the screener containing 18 high quality undiscovered gems, so you are not the last to notice when quality stories gain wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.