First Solar (FSLR) Valuation Check After Record Q1 Results And Maintained Full Year Guidance

First Solar, Inc. FSLR | 0.00 |

First Solar (FSLR) just reported record first quarter 2026 results, with earnings per share beating expectations and net sales of US$1.04b. The company kept its full year guidance unchanged, which many investors watch closely.

The earnings beat helped shift sentiment after a weak start to the year, with the share price up 4.86% in the last session and a 7 day share price return of 9.26%. However, year to date the share price return is still down 22.83%, while the 1 year total shareholder return of 62.18% points to strong longer term momentum.

If record results in solar have your attention, this can be a useful moment to see which other power grid and energy infrastructure names are moving via our 34 power grid technology and infrastructure stocks

So with the shares still down year to date, yet trading at a discount to both some analyst targets and certain intrinsic value estimates, is First Solar quietly undervalued at this point, or are markets already pricing in the potential growth story?

Most Popular Narrative: 35.7% Overvalued

Compared with First Solar's last close at $211.71, the most followed narrative on the stock places fair value much lower at $155.98, which sets up a very different picture from recent trading.

Known for its high quality solar panels and government cooperation during the Biden administration, First Solar is a strong company when it comes to maintaining its operations and innovating on solar energy. Our team believes that First Solar is considerably below its fair value. The current semi bear market present in the US markets caused by President Trump’s tariffs and trade war threats has caused negative sentiments in the market which overall reflected on First Solar’s stock price causing it to drop below its fair price.

The narrative hinges on a detailed view of revenue growth, high margins and a future earnings multiple that together aim to justify that fair value. It blends assumptions about how fast profits compound with what kind of P/E investors might pay if those margins persist. If you want to see exactly how those moving parts shape the $155.98 figure and how they compare to current market expectations, the full narrative lays out every step.

Result: Fair Value of $155.98 (OVERVALUED)

However, this view could be challenged if trade policies change in ways that affect solar economics, or if margins and revenue growth differ from the assumptions behind that US$155.98 figure.

Another View: Multiples Paint a Different Picture

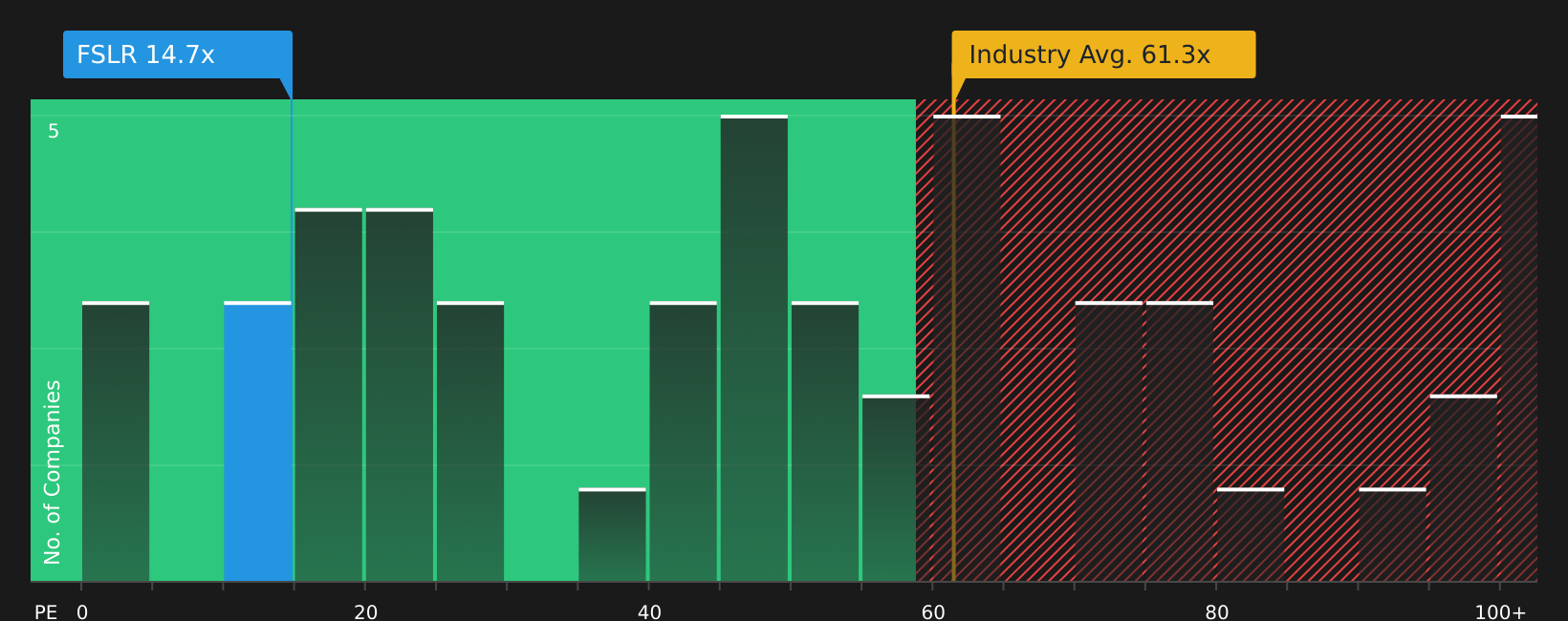

While the leading narrative sees First Solar as 35.7% overvalued at $211.71 versus a $155.98 fair value, the current P/E of 13.7x tells a different story. It sits well below the Semiconductor industry at 48.2x, peers at 84.1x, and even the 40.8x fair ratio the market could move toward. For you, that gap raises a simple question: is this a valuation risk or a valuation opportunity waiting to be tested by future results?

Next Steps

If the mixed signals on price and valuation leave you unsure, move quickly from headlines to hard data and weigh the trade off yourself with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If First Solar has you thinking more seriously about where you put your money next, do not stop at one name. Use focused lists to spot fresh opportunities.

- Target potential mispricings early by scanning our screener containing 25 high quality undiscovered gems before they appear on everyone else's radar.

- Prioritise resilience by checking companies in the 67 resilient stocks with low risk scores that may offer a steadier ride when volatility picks up.

- Focus on quality at a sensible entry point by reviewing companies in the 51 high quality undervalued stocks that combine fundamentals with pricing that could appeal to value focused investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.