FirstCash (FCFS) Earnings Growth Surges 26.5%, Reinforcing Bullish Margin Narrative

FirstCash Holdings, Inc. FCFS | 201.63 | +1.37% |

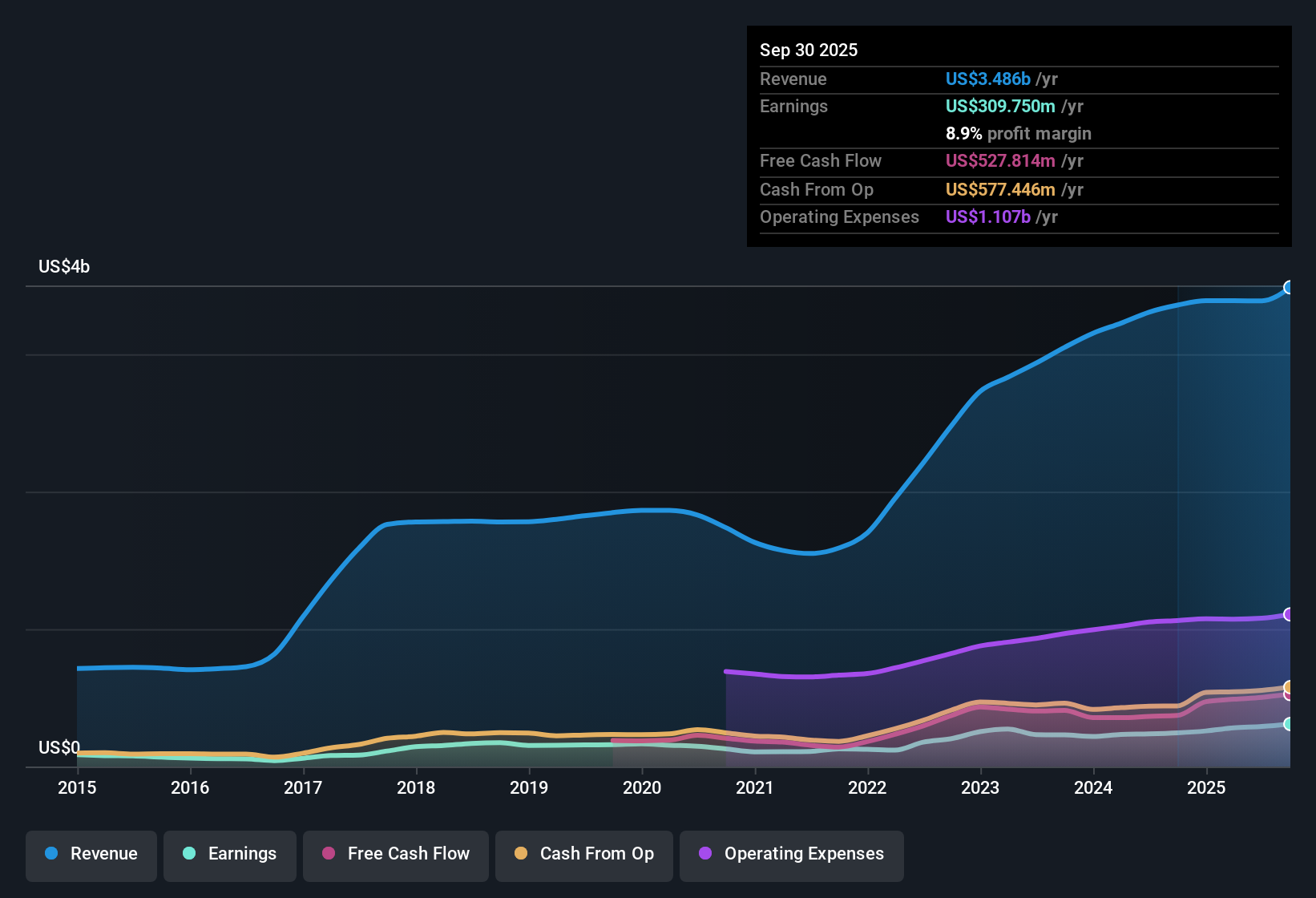

FirstCash Holdings (FCFS) reported earnings growth of 26.5% over the past year, outpacing its five-year average of 19.9% per year. Net profit margins improved to 8.9% from 7.3% last year, and the company is expected to see earnings increase at a 17.5% annual rate moving forward. While the share price sits at $158.64, well above the discounted cash flow fair value estimate of $71.35, the rising historic and projected profit and revenue offer a compelling growth narrative that investors will want to weigh against its high valuation multiple.

See our full analysis for FirstCash Holdings.Next, we will see how these headline numbers compare to the stories shaping consensus and debate in the market. Some narratives may get reinforced, while others will meet new evidence.

High Margins Signal Profit Quality

- Net profit margins reached 8.9% this year, up from 7.3% previously, pointing to an improvement in profitability that stands out compared to industry peers.

- Strong margins heavily support the case that FirstCash’s business model can defend profits in a range of economic conditions, especially amid macro uncertainty.

- Bulls argue that this margin resilience confirms FirstCash’s position as a defensive provider in the specialty finance sector, as margin expansion occurred alongside 26.5% earnings growth.

- What’s surprising is that even with rising profits, the company has maintained high profit quality, raising the ceiling for future performance if growth can stay on track.

Growth Forecasts Outrun Market

- Earnings are forecast to grow at a 17.5% annual rate, while revenue is set to rise by 9.5% per year, close to the broader US market’s 10.3% expectation but with a stronger profit trajectory.

- The company’s combination of high historical growth and sustained forecasts draws focus to its unique status in the sector.

- The prevailing view is that robust profit and revenue projections, surpassing industry trends, lend credibility to FirstCash as a growth story that could weather changes in macro conditions.

- Despite US market peer revenue forecasts edging slightly higher, FirstCash’s profit outlook gives it a differentiated edge that investors may seize on as justification for its premium.

Valuation Stands Out Versus Industry

- FirstCash trades at a price-to-earnings ratio of 22.7x, significantly higher than the US Consumer Finance industry average of 10x, yet markedly lower than the peer group’s 46.4x multiple. The share price of $158.64 far exceeds the DCF fair value estimate of $71.35.

- The tension between headline growth and valuation premium puts a spotlight on whether investors are willing to pay an above-industry multiple for the company’s durable earnings profile.

- What’s notable is that even as the stock commands a substantial premium to industry, the valuation is actually better than many immediate peers, offering a nuanced take for value-focused investors.

- However, the wide gap to DCF fair value may spark debate about how much future growth is already priced in, especially with only minor risks highlighted in the filings.

Curious how numbers become stories that shape markets? Explore Community Narratives Curious how numbers become stories that shape markets? Explore Community Narratives

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on FirstCash Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Despite FirstCash’s impressive growth and profitability, its current share price sits at a substantial premium to fair value. This raises concerns about overvaluation.

If you’re wary of paying too much, use these 834 undervalued stocks based on cash flows to focus on companies with strong fundamentals that may offer more attractive entry points right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.