Flowserve (FLS) Is Up 6.2% After Reaffirming 2026 AI Power Guidance Amid Starboard Pressure - Has The Bull Case Changed?

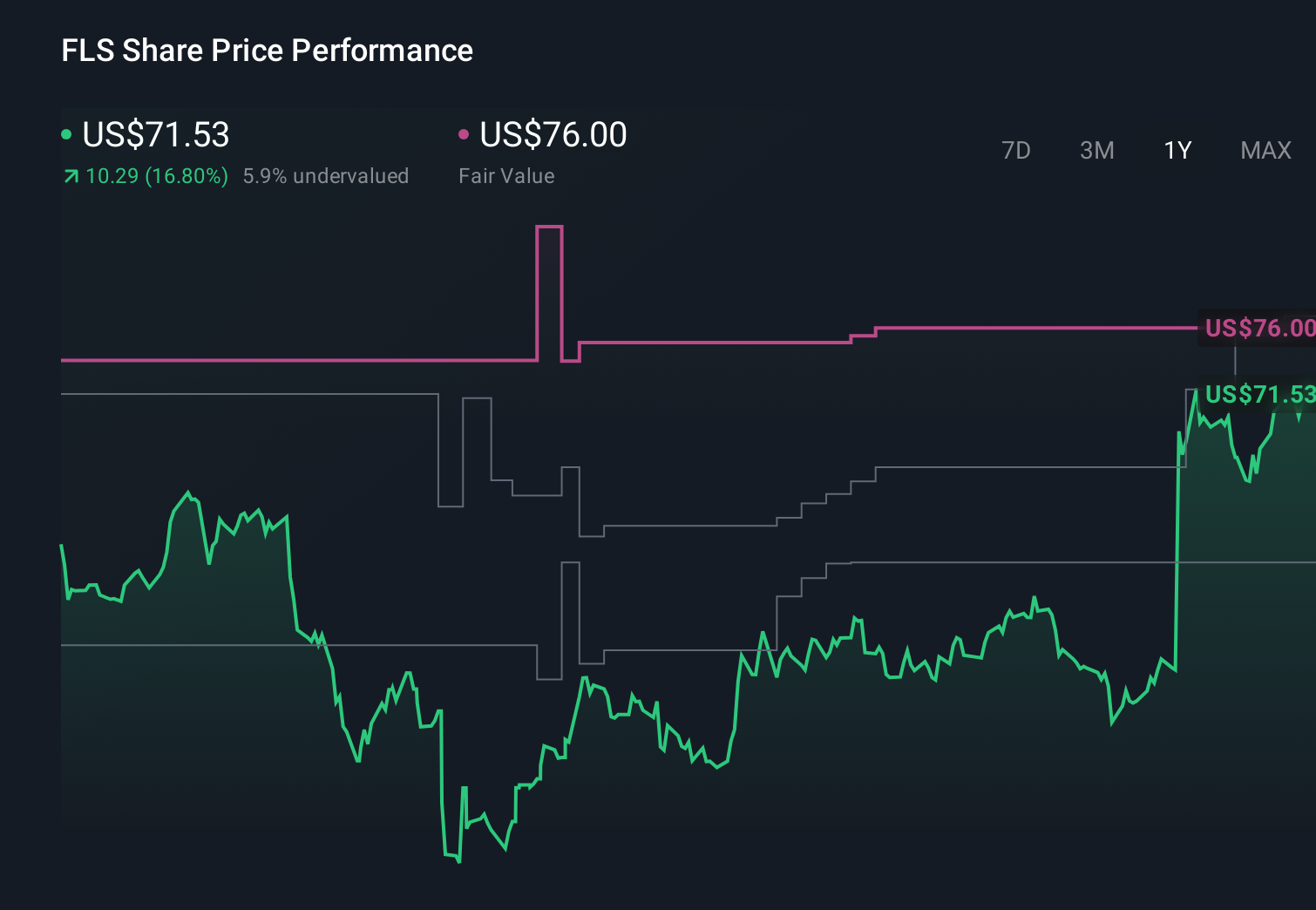

Flowserve Corporation FLS | 0.00 |

- In recent weeks, Flowserve has highlighted its exposure to AI-driven infrastructure, reaffirmed 2026 guidance, and emphasized earnings support from power generation, nuclear and aftermarket demand, while responding to activist investor Starboard Value’s calls for operational and capital allocation improvements.

- An important angle is how management’s confidence in AI-linked power projects and margin expansion targets, despite a weak backlog patch and only modest revenue growth expectations, is reshaping investor perceptions of the company’s long-term earnings potential.

- Next, we’ll examine how management’s reaffirmed guidance amid Starboard’s activism could reshape Flowserve’s investment narrative around AI-related infrastructure exposure.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Flowserve Investment Narrative Recap

To own Flowserve, you need to believe its exposure to AI-linked power, nuclear and aftermarket work can translate into durable earnings, even with only modest revenue growth and a mixed backlog. The near term catalyst is whether AI-related power projects convert into firm orders and margin progress, while the biggest risk is that weak bookings and tougher project pricing limit that margin expansion. Recent news around AI infrastructure and activism reinforces the story but does not fundamentally change these near term drivers.

The most relevant recent announcement is Flowserve’s May 29 response to activist investor Starboard Value, where the company reaffirmed 2026 guidance, highlighted adjusted margin gains since 2022, and emphasized AI related power and nuclear demand as key supports for its 2030 targets. This directly ties into the catalyst around margin execution and AI-linked infrastructure, while keeping attention on the risk that project delays, tariffs and competitive bidding could still constrain the benefit to earnings.

Yet beneath Flowserve’s AI and margin story, investors should be aware that tariff exposure and project delays could still materially affect earnings and cash flow...

Flowserve’s narrative projects $5.5 billion revenue and $718.3 million earnings by 2029. This requires 5.9% yearly revenue growth and roughly a $364.3 million earnings increase from $354.0 million today.

Uncover how Flowserve's forecasts yield a $90.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$5.5 billion and earnings near US$691 million by 2029, and their tariff and macro concerns could look very different once Flowserve’s new AI related power optimism and activist pressure are fully reflected in updated forecasts.

Explore 5 other fair value estimates on Flowserve - why the stock might be worth just $82.33!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Flowserve research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.