Flowserve Stock And 2 US Industrial Picks For Rising Tariff Pressure

Century Aluminum Company CENX | 0.00 |

Tariff threats are back on the table, and this time the focus is on countries pushing digital services taxes on US tech giants. If those 100% tariffs on imports materialize, companies that manufacture and operate mainly within US borders could sit in a very different risk bucket from globally exposed exporters. This article looks at how that tension around digital taxes and Section 301 action might feed through to US domestic manufacturing and industrial stocks, and highlights 3 stocks from our screener that appear relatively better positioned if trade frictions pick up again.

Flowserve (FLS)

Overview: Flowserve is a long established US industrial company that designs and services pumps, valves, seals and related equipment that keep fluids moving safely through critical energy, water, chemical and industrial systems worldwide.

Operations: Flowserve generates most of its revenue from the Flowserve Pump Division at about US$3.2b, with the Flow Control Division contributing about US$1.5b and a small amount removed through eliminations and other items.

Market Cap: US$9.6b

Flowserve stands out in a tariff heavy world because it is a major US based manufacturer with a diversified backlog tied to energy transition, water infrastructure and AI driven power projects, while direct exposure to exports is reported as a modest share of sales. The company has been working on margin expansion, digital monitoring solutions and higher value services. Investors still need to weigh that story against issues like weaker backlog growth, a recent large non recurring loss and reliance on external borrowing. With activist pressure for faster execution and analysts split on how earnings guidance holds up to geopolitical shocks, Flowserve presents a mix of resilience and tension that may merit closer consideration.

Flowserve looks like a US industrial story that could be decoupling from pure export risk, yet activist pressure and that recent large non recurring loss still raise questions. See how the 5 key rewards and 1 important warning sign might reshape the picture for tariffs, margins, and that backlog narrative investors are only starting to piece together.

Century Aluminum (CENX)

Overview: Century Aluminum produces primary aluminum and alumina, supplying standard grade and higher value products from smelters in the United States and Iceland, as well as a carbon anode plant in the Netherlands and bauxite and alumina operations in Jamaica.

Operations: Century Aluminum generates about US$2.5b in revenue from primary aluminum, with roughly US$1.9b from the United States and US$660m from Iceland.

Market Cap: US$4.5b

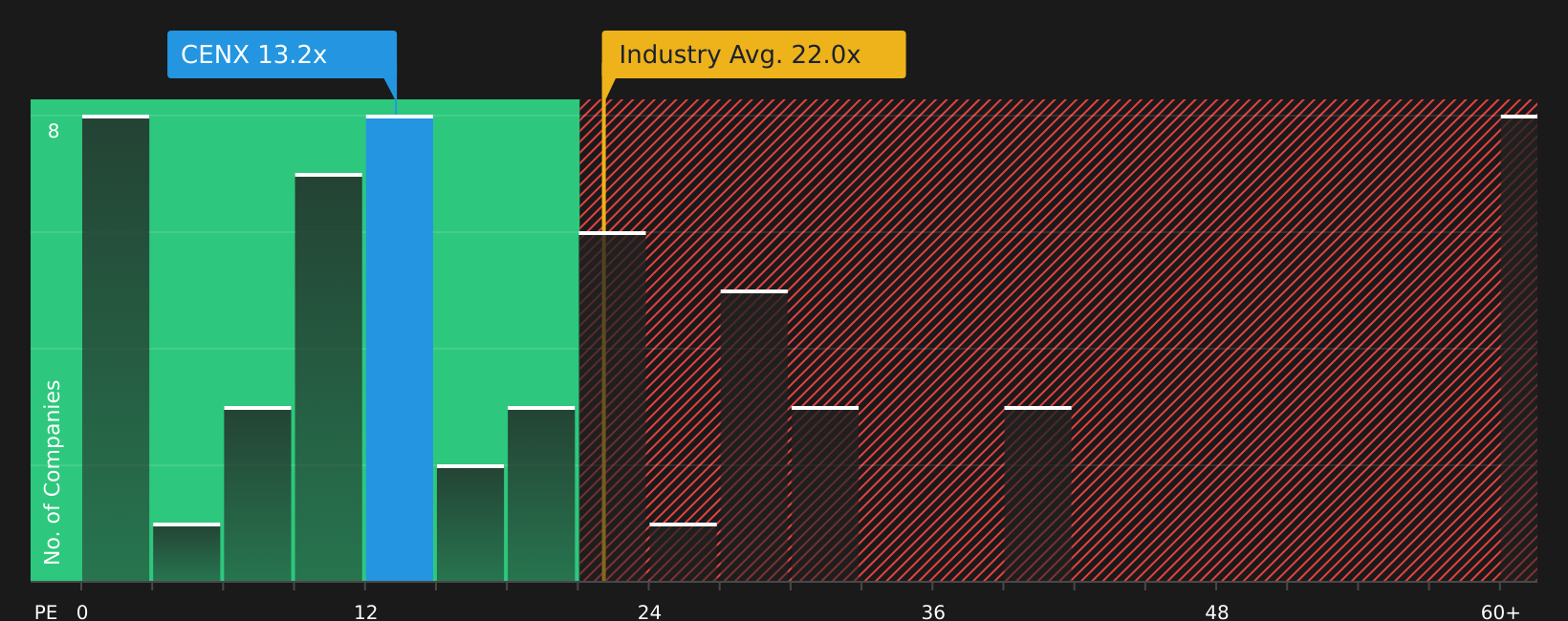

Century Aluminum sits at the center of the tariff conversation because it runs primary aluminum smelting inside the US, is working on a new domestic smelter project and has been vocal about support from Section 232 and Section 301 actions. Earnings growth, higher Midwest premiums and government tax credits have influenced the story. A P/E that is below the US Metals & Mining industry average, expanding domestic capacity and recent moves to secure a US based mine to metal supply chain are also key factors for the company. On the other hand, it has heavy reliance on favorable trade policy, energy and raw material costs and higher risk funding, which means the same tariff and power themes that support Century Aluminum can also quickly test its resilience if conditions change.

Century Aluminum’s efforts to expand US smelting capacity, secure tax credits, and establish a mine-to-metal supply chain appear to be an underappreciated story, and the analysis report for Century Aluminum highlights one crucial pressure point that investors often overlook.

VSE (VSEC)

Overview: VSE Corporation is an aviation services company that supplies aftermarket aircraft parts and provides maintenance, repair, and overhaul services for commercial airlines, cargo carriers, government fleets, and private aviation customers worldwide.

Operations: VSE generates about US$1.2b in revenue from its Aviation segment.

Market Cap: US$6.3b

VSE sits squarely in the crosshairs of onshoring and defense focused spending. Its aviation aftermarket model gives it exposure to both commercial travel and government fleets at a time when tariff threats are pushing supply chains closer to home. The company has been growing through acquisitions in higher margin aviation distribution and repair, with earnings momentum and rising profit margins pointing to improving efficiency. However, that growth is funded with higher risk external borrowing, shareholder dilution, and a relatively high P/E. For investors, the real question is whether VSE’s expanding repair capabilities and OEM partnerships offset the concentration in aviation, integration risk, and governance concerns that come with a fast rising stock in a more protectionist trade setting.

VSE’s accelerating aviation aftermarket story, funded with higher risk capital and a rich P/E, looks powerful but incomplete. The analyst forecasts for VSE hints at one growth hinge investors may be underestimating.

The three stocks covered here are just a starting point, and the full US Domestic Manufacturing and Industrial Stocks screener surfaces 27 more US based manufacturing and industrial companies with equally compelling tariff and reshoring narratives that might fit your watchlist. Use Simply Wall St to identify, analyze, and filter for the specific catalysts, risk profiles, and business stories that matter most so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If VSE or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly

Fresh ideas do not stay quiet for long. Before the next breakout gains momentum and these stories are caught by the crowd, scan under the radar for now and act early.

- Target durable income streams by scanning a focused group of reliable payers through the 8 dividend fortresses before yields start dropping as more investors pile in.

- Seek early momentum in companies supplying the picks and shovels for AI growth by reviewing the curated 51 AI infrastructure stocks, while it still flies under most radars.

- Identify under the radar operators positioned for long term electrification trends by filtering through the hand picked 8 top copper producer stocks before demand stories move fully into the spotlight.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.